![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1096, 1097, 1098, 1099, 3921, 3922, 5498, W-2G

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1096, 1097, 1098, 1099, 3921, 3922, 5498, W-2G

for the current year.

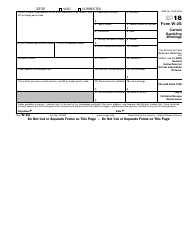

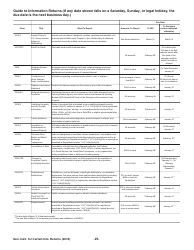

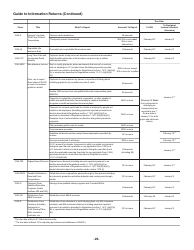

Instructions for IRS Form 1096, 1097, 1098, 1099, 3921, 3922, 5498, W-2G Certain Information Returns

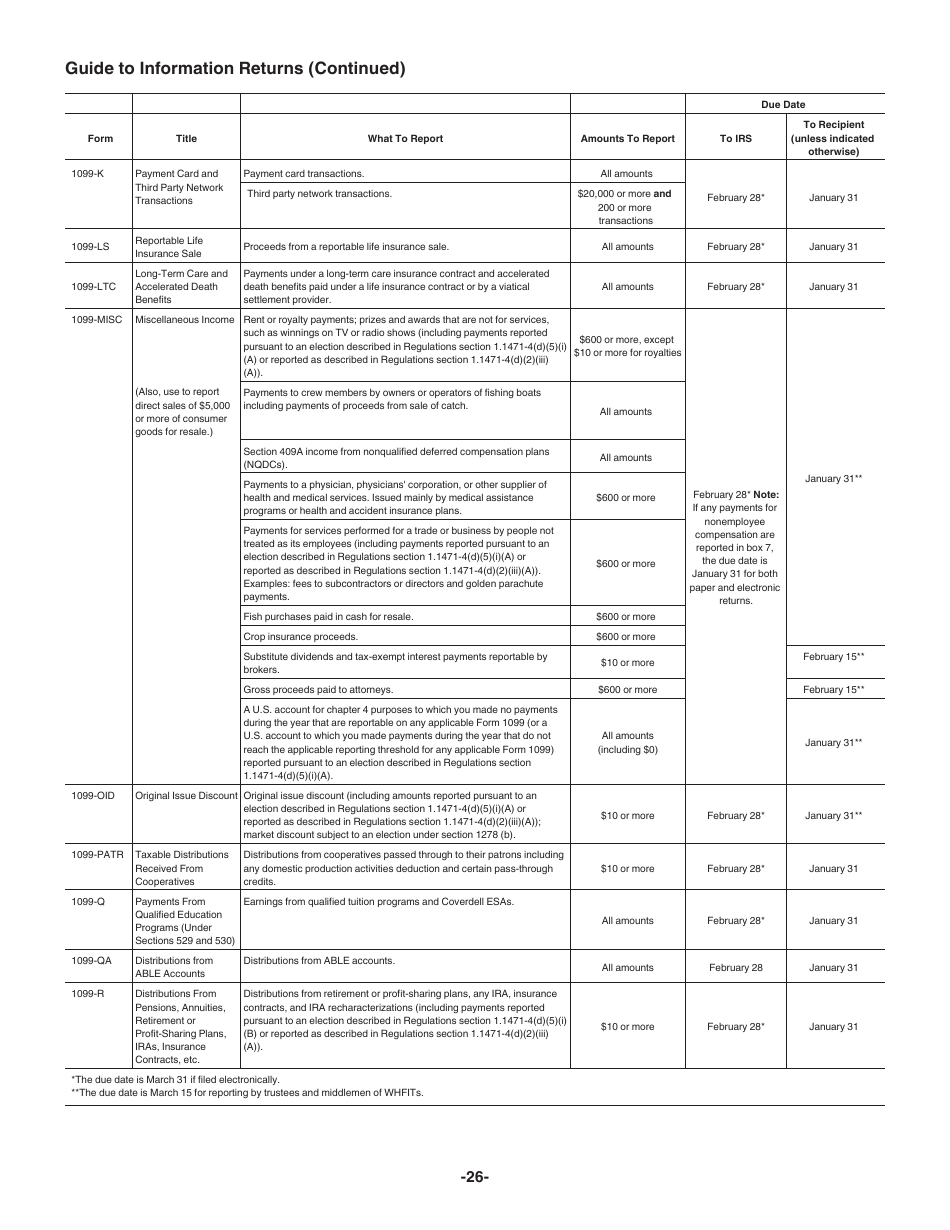

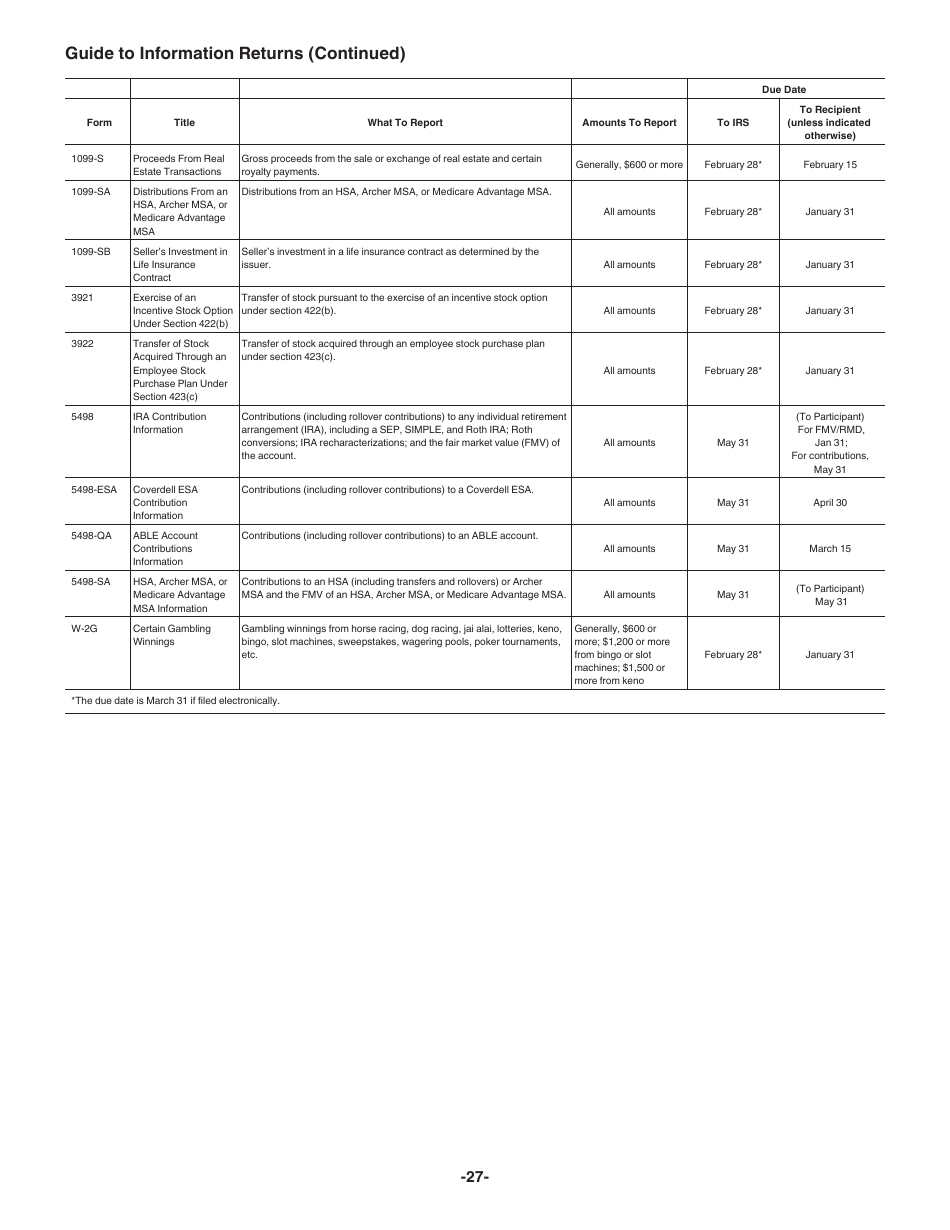

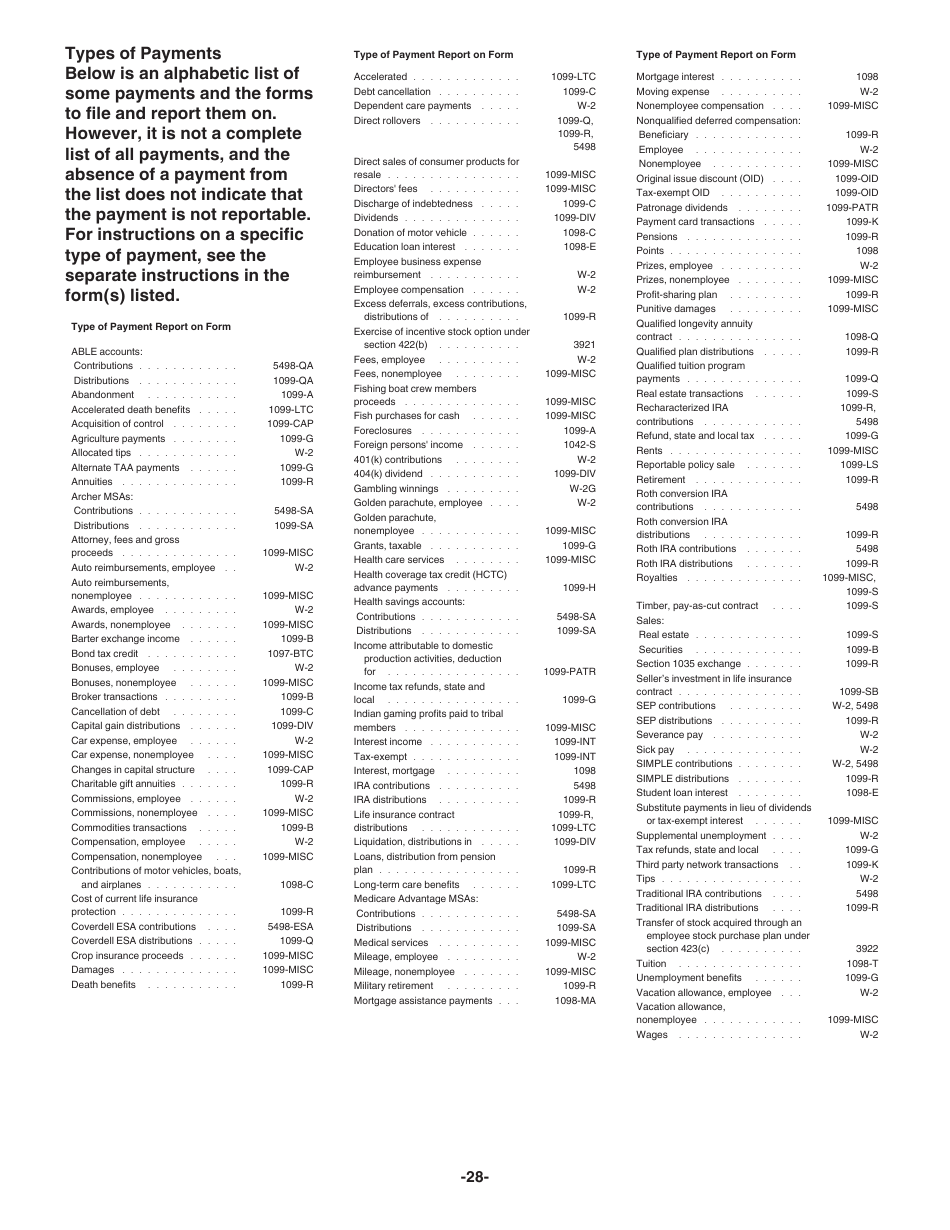

This document contains official instructions for IRS Form 1096 , IRS Form 1097 , IRS Form 1098 , IRS Form 1099 , IRS Form 3921 , IRS Form 3922 , IRS Form 5498 , and IRS Form W-2G . All forms are released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1096 is available for download through this link. The latest available IRS Form 1098 can be downloaded through this link. IRS Form 5498 can be found here. IRS Form W-2g can be downloaded here.

FAQ

Q: What is IRS Form 1096?A: IRS Form 1096 is used to summarize and transmit forms 1099 to the IRS.

Q: What is IRS Form 1097?A: IRS Form 1097 is used to report certain payments made by the federal government.

Q: What is IRS Form 1098?A: IRS Form 1098 is used to report mortgage interest, student loan interest, or tuition payments.

Q: What is IRS Form 1099?A: IRS Form 1099 is used to report various types of income, including freelance earnings, interest, and dividends.

Q: What is IRS Form 3921?A: IRS Form 3921 is used to report the exercise of incentive stock options.

Q: What is IRS Form 3922?A: IRS Form 3922 is used to report the transfer of stock acquired through an employee stock purchase plan.

Q: What is IRS Form 5498?A: IRS Form 5498 is used to report IRA contributions, rollovers, and conversions.

Q: What is IRS Form W-2G?A: IRS Form W-2G is used to report certain gambling winnings.

Instruction Details:

- This 29-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below{class="scroll_to"} or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 1096, 1097, 1098, 1099, 3921, 3922, 5498, W-2G Certain Information Returns

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29