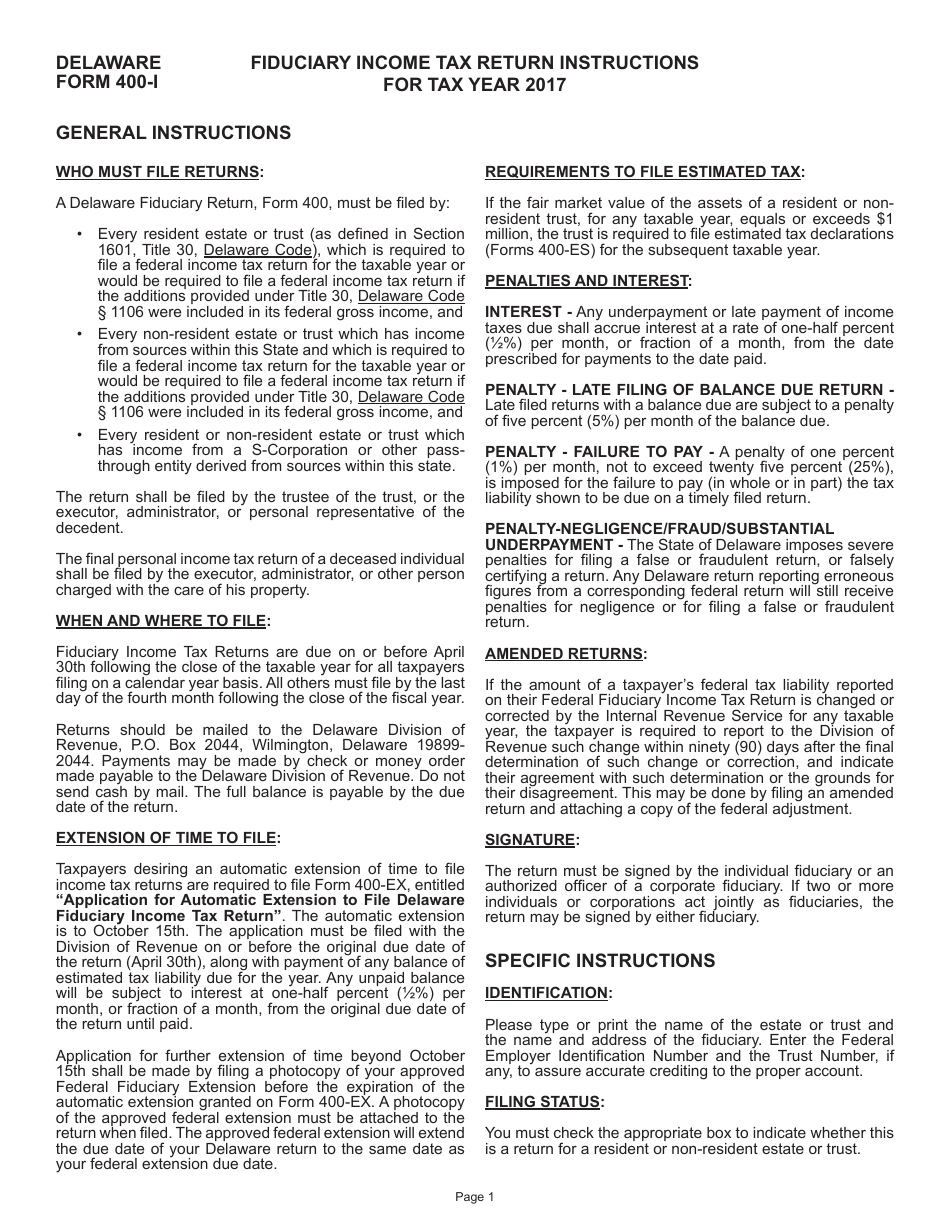

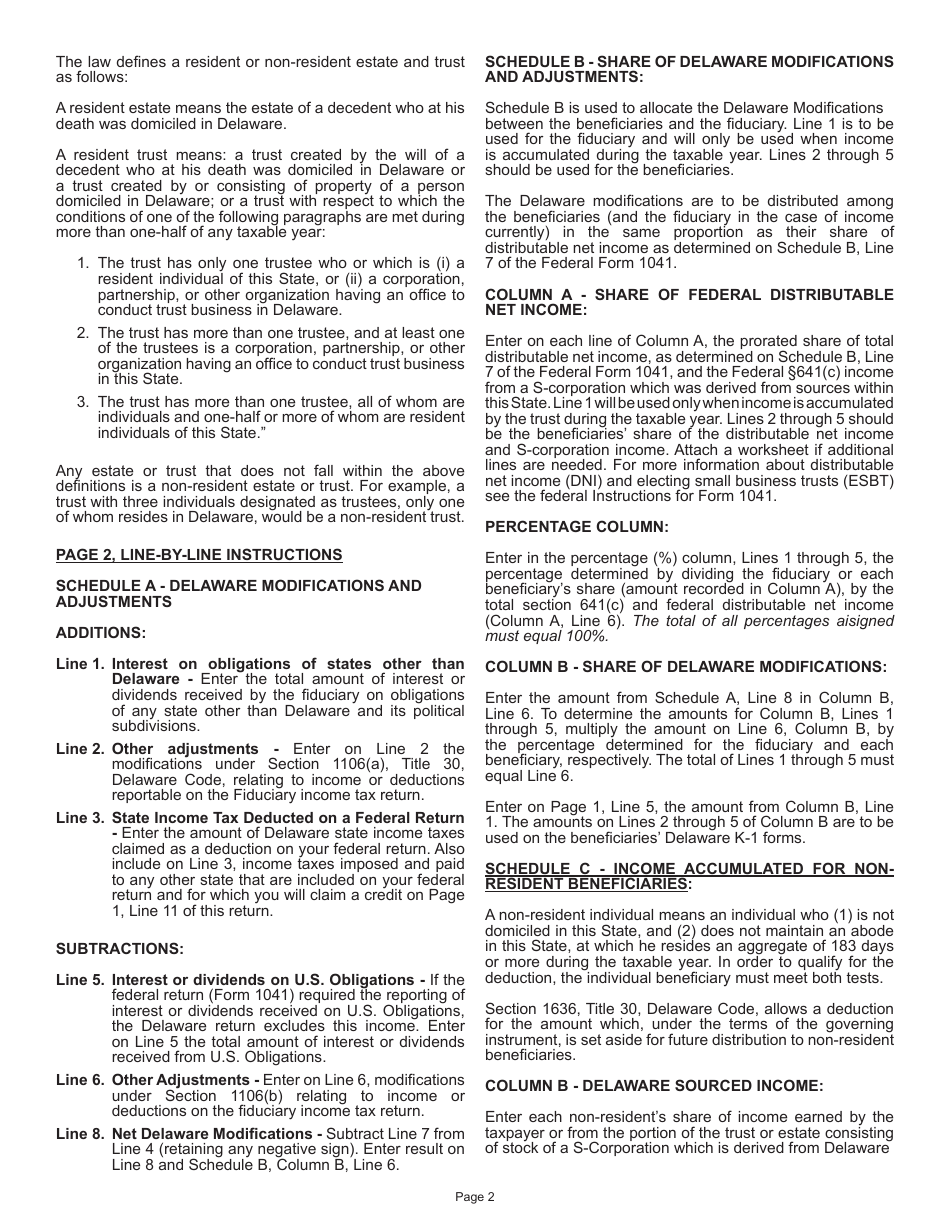

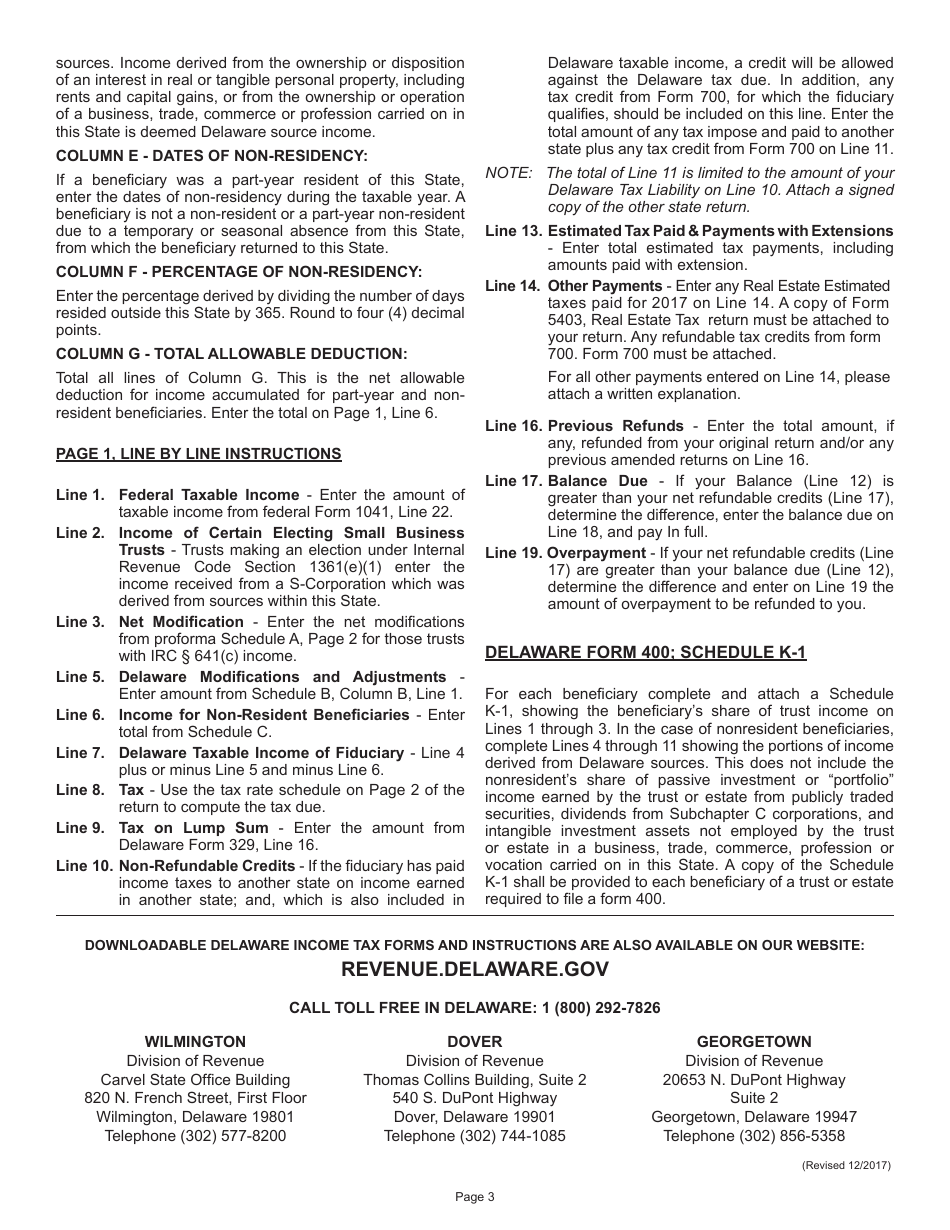

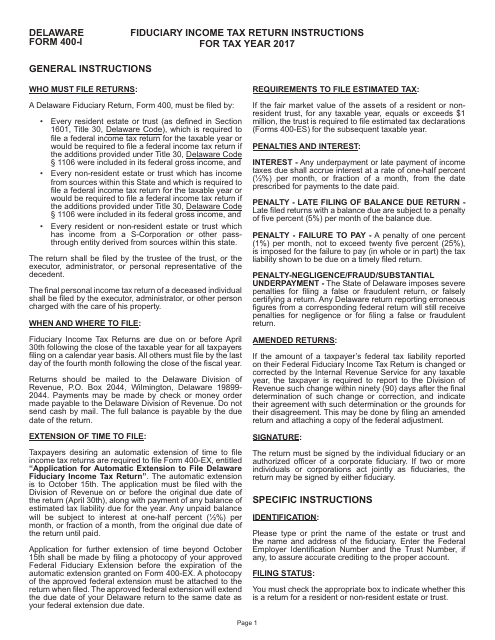

Instructions for Form 400 Fiduciary Income Tax Return - Delaware

This document contains official instructions for Form 400 , Fiduciary Income Tax Return - a form released and collected by the Delaware Department of Finance.

FAQ

Q: What is Form 400?

A: Form 400 is the Fiduciary Income Tax Return for Delaware.

Q: Who needs to file Form 400?

A: Fiduciaries, such as trustees or executors, who are responsible for filing taxes on behalf of an estate or trust in Delaware.

Q: What is the purpose of Form 400?

A: Form 400 is used to report the income, deductions, and credits of an estate or trust in Delaware.

Q: When is Form 400 due?

A: Form 400 is due on or before April 30th following the end of the taxable year.

Instruction Details:

- This 3-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Delaware Department of Finance.

1

2

3