Free SBA Disaster Loan Forms and Templates

What Is an SBA Disaster Loan?

An SBA Disaster Loan is a form of financial assistance by the Small Business Administration (SBA) to businesses and private non-profit organizations, homeowners, and renters located in regions affected by the declared disaster. This assistance comes as low-interest, long-term credit, providing support for faster recovery in an emergency. If insurance or funding from FEMA (Federal Emergency Management Agency) does not fully cover losses, you may qualify for this financing option. This federal assistance becomes available in regions stated in an official declaration.

SBA Disaster Loan Application Forms

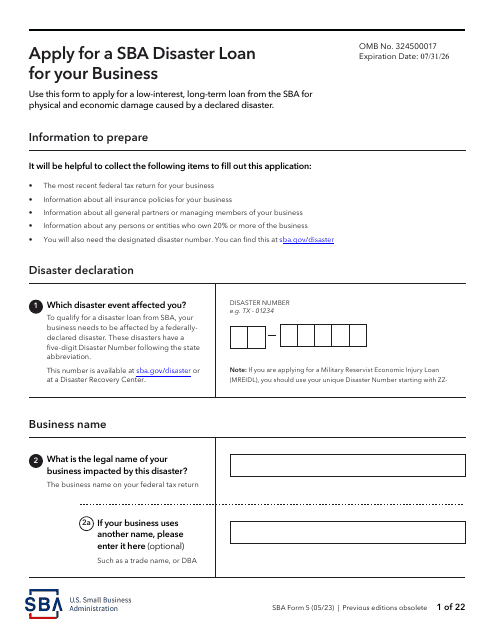

- SBA Form 5 is to be completed by all small business applicants;

- SBA Form 5C is an application for renters and homeowners;

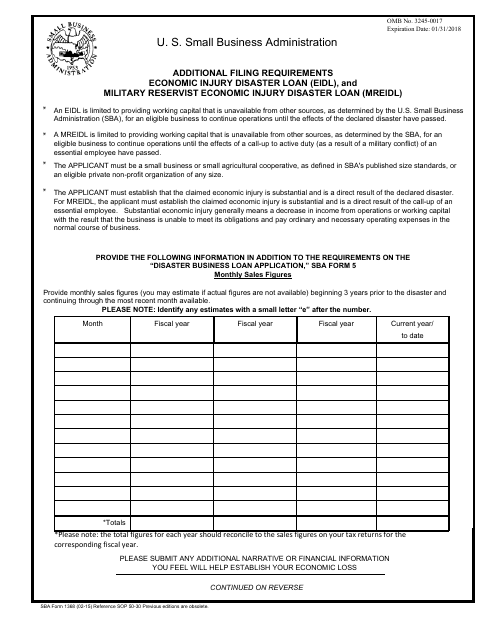

- SBA Form 1368 is an additional document for military reservists (MREIDL);

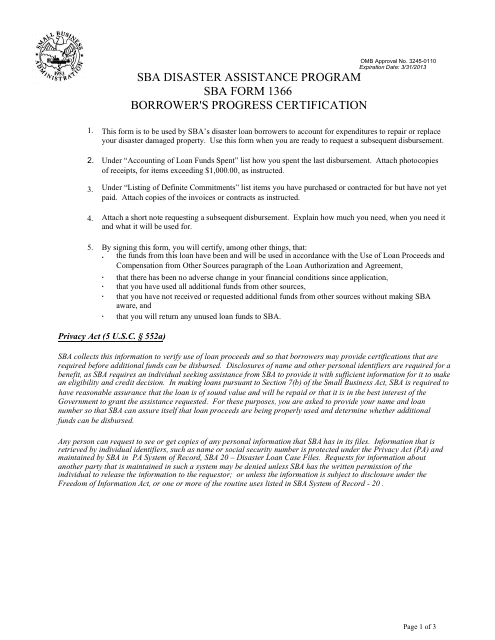

- SBA Form 1366 is a form for keeping records of borrower's expenditures;

Additional related forms include SBA Form 3305 (a volunteer award for outstanding contributions), SBA Form 3304 (a public official award), and SBA Form 3303 (an award for small business disaster recovery

General disaster loan terms are as follows:

- Amounts up to $2M to companies and up to $200K to individuals;

- 30-year repayment plan;

- Interest rates from 2.75% to 8%, calculated individually;

- First month’s payment deferral for a year;

There are different forms of lending options, depending on the nature of a cataclysm: Home and Property, Economic Injury, Military Reservist Economic Injury, Farm Emergency. In such tragic events, substantial damage and serious, often uninsured losses are suffered by the population. When local and state governments are overwhelmed by the outcome and are unable to provide adequate relief, the governor requests help from FEMA, SBA, etc.

An SBA Disaster Loan disbursement is made through a non-profit - a CDC - which then distributes funds to approved applicants. EIDL ( Economic Injury Disaster Loan ) is the most commonly provided loan type.

How Long Does It Take to Get an SBA Disaster Loan?

The SBA typically provides assistance within four weeks. Lending decisions are always based on the applicant’s credit score. After applying, a credit review will be the first step made by the SBA, followed by the inspection to verify incurred losses and summing up all eligible insurance recoveries. EIDL can be issued before insurance payments are received by the applicant. It takes approximately 5 days to receive an initial payment after your signed Loan Closing Documents are received by the loan officer.

What Can an SBA Disaster Loan Be Used For?

A disaster loan - also called the "SBA Disaster Relief" - intends to finance recovery from the crisis. You can use the lent money to pay for repair or replacement of damaged property, mortgage or lease payments, equipment, inventory, as well as paying for other obligations and operating costs.

How Hard Is It to Get an SBA Disaster Loan?

SBA Disaster Loan requirements are fairly strict. To qualify, you need to have a minimum credit score of 620-680, depending on the application type and what regional lender you will be working with. Acceptable credit score ensures a safer loan repayment rate, although these terms are often tough for people and organizations. Advances under $200,000 can be approved without a personal guarantee or collateral.

Homeowners and tenants need to submit an IRS Form 4506-T with their SBA Form 5C. This allows the SBA to access the applicant's tax return information. If you own a small business, file both SBA Form 5 and IRS Form 4506-T, complete a personal financial statement, attach a list of liabilities and provide a copy of the previous year’s Federal income tax return. Additional information may be requested depending on individual circumstances.

Documents:

7

Use this form to enter information on the business's monthly revenue for three years prior to the disaster. You can also use this form to provide your financial forecast of income and expenses until the time when you estimate your business will operate normally.

This form is used for borrowers to certify their progress in the SBA Disaster Assistance Program. It helps track and verify the borrower's use of funds and the progress made towards recovery.