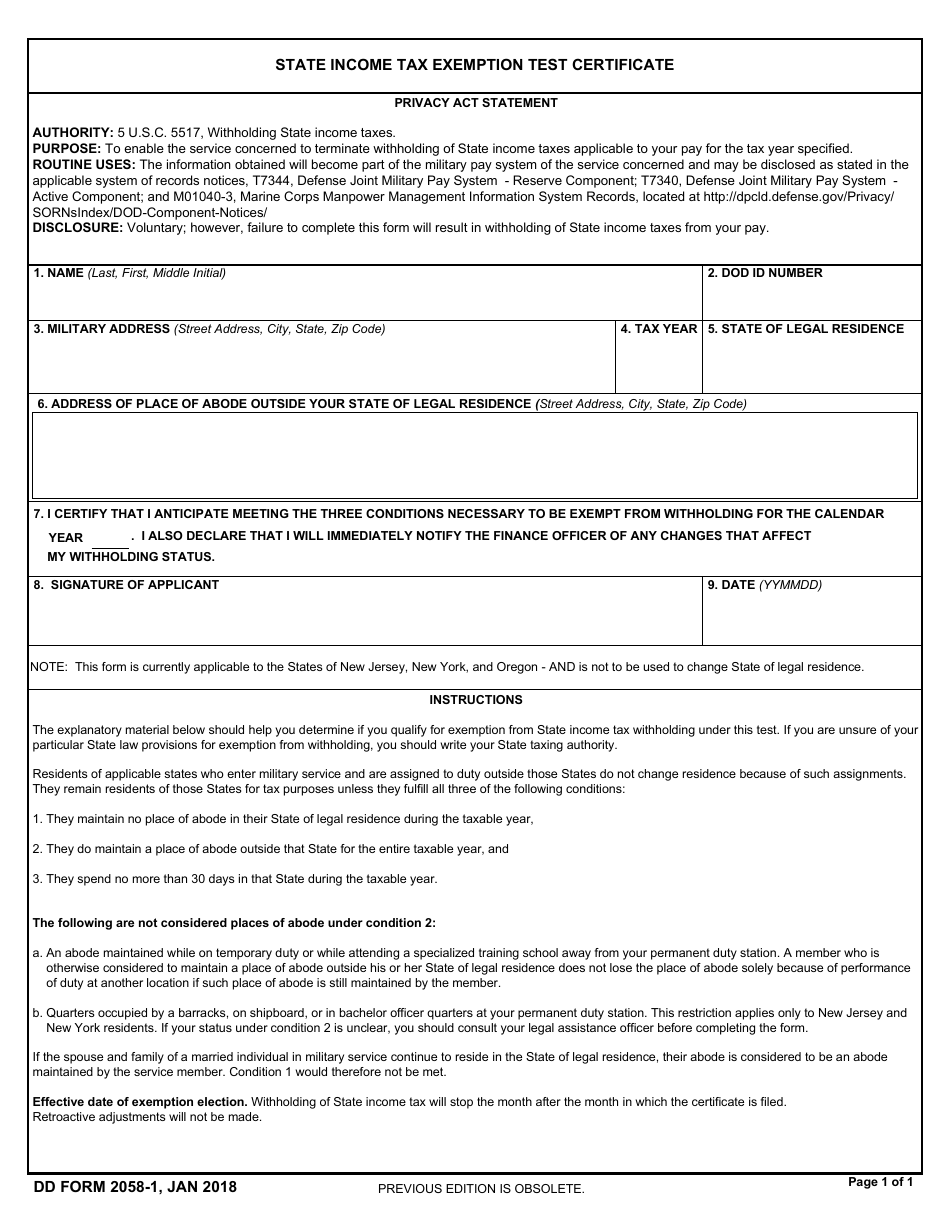

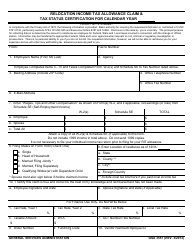

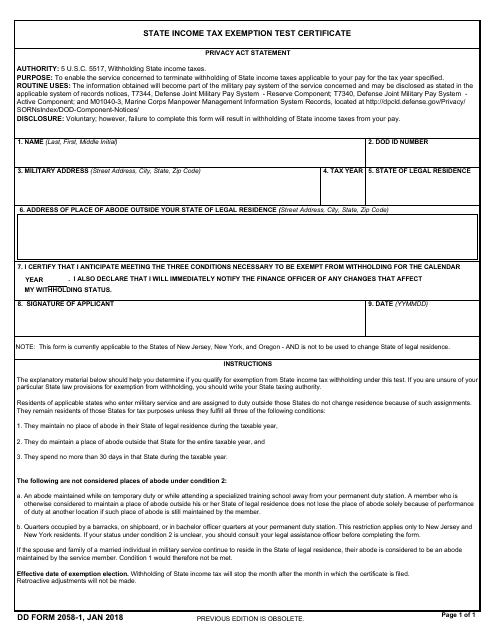

DD Form 2058-1 State Income Tax Exemption Test Certificate

Fill PDF Online

Fill out online for free

without registration or credit card

What Is DD Form 2058-1?

This is a form that was released by the U.S. Department of Defense (DoD) on January 1, 2018. The form, often mistakenly referred to as the DA Form 2058-1, is a military form used by and within the U.S. Army. As of today, no separate instructions for the form are provided by the DoD.

Form Details:

- A 1-page document available for download in PDF;

- The latest version available from the Executive Services Directorate;

- Additional instructions and information can be found on page 1 of the document;

- Editable, printable, and free to use;

- Fill out the form in our online filing application.

Download an up-to-date fillable DD Form 2058-1 down below in PDF format or browse hundreds of other DoD Forms compiled in our online library.

DD Form 2058-1 Instructions

Failing to file the DD 2058-1 correctly and on time will result in the state income tax being withheld from your pay.

- Active duty service members file their tax returns according to the laws applicable to their State of Legal Residence. The rules for civilians are as follows: you remain a resident of your state unless you spent 30 days or less in your state of residence or voluntarily abandoned your residency to establish a new legal domicile in another state. If your SLR (State of Legal Residence) differs from your permanent place of abode then you are considered a resident of that place for income tax purposes.

- Active duty does not affect your SLR. A service member is still considered a resident of their State of Legal Residence regardless of being stationed in another state.

- Each state has specific laws that regulate whether a service member is exempt from paying income tax while on duty. Contact your state tax authority for up-to-date information. If you change your SLR while serving in the military, your income tax payments will depend on the laws of that state.

- Fill in the DD 2058-1. Write down your name, Army ID, military address, and the taxable year. Define your State of Legal Residence or place of abode outside of your legal residence (if any). Note that all cases of change of residency must be immediately reported to your military personnel office. Sign and date the form and turn it in at S-1. Withholding of income tax will stop the month after the one in which the certificate is filed.

DD 2058-1 Related Forms:

- DD Form 2058, State of Legal Residence Certificate, is used by servicemen and women to document a change in legal residence;

- DD Form 2058-2, Native American State Income Tax Withholding Exemption Certificate, is used for claiming exemption from income tax withholding by Native American members of the Army.