![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 760C

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 760C

for the current year.

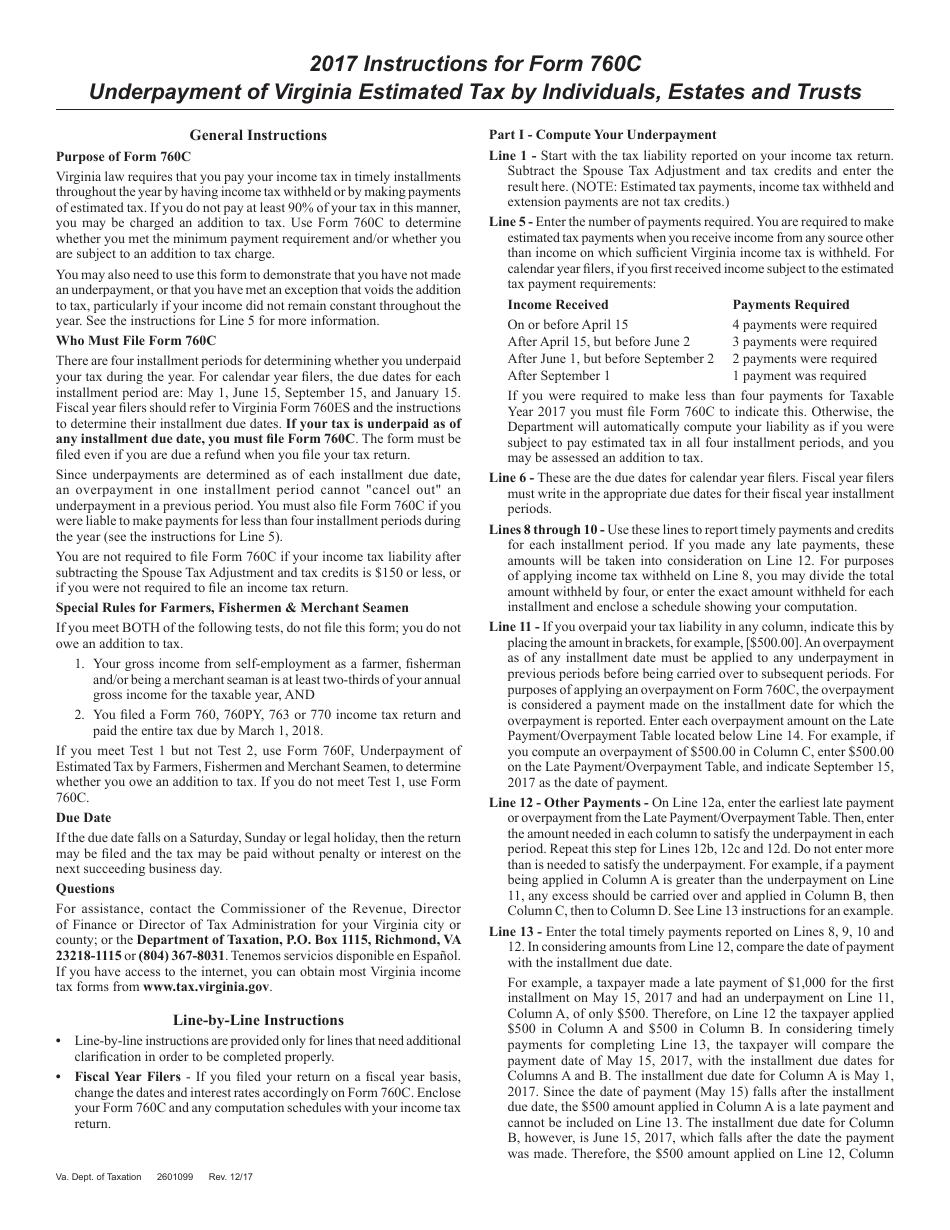

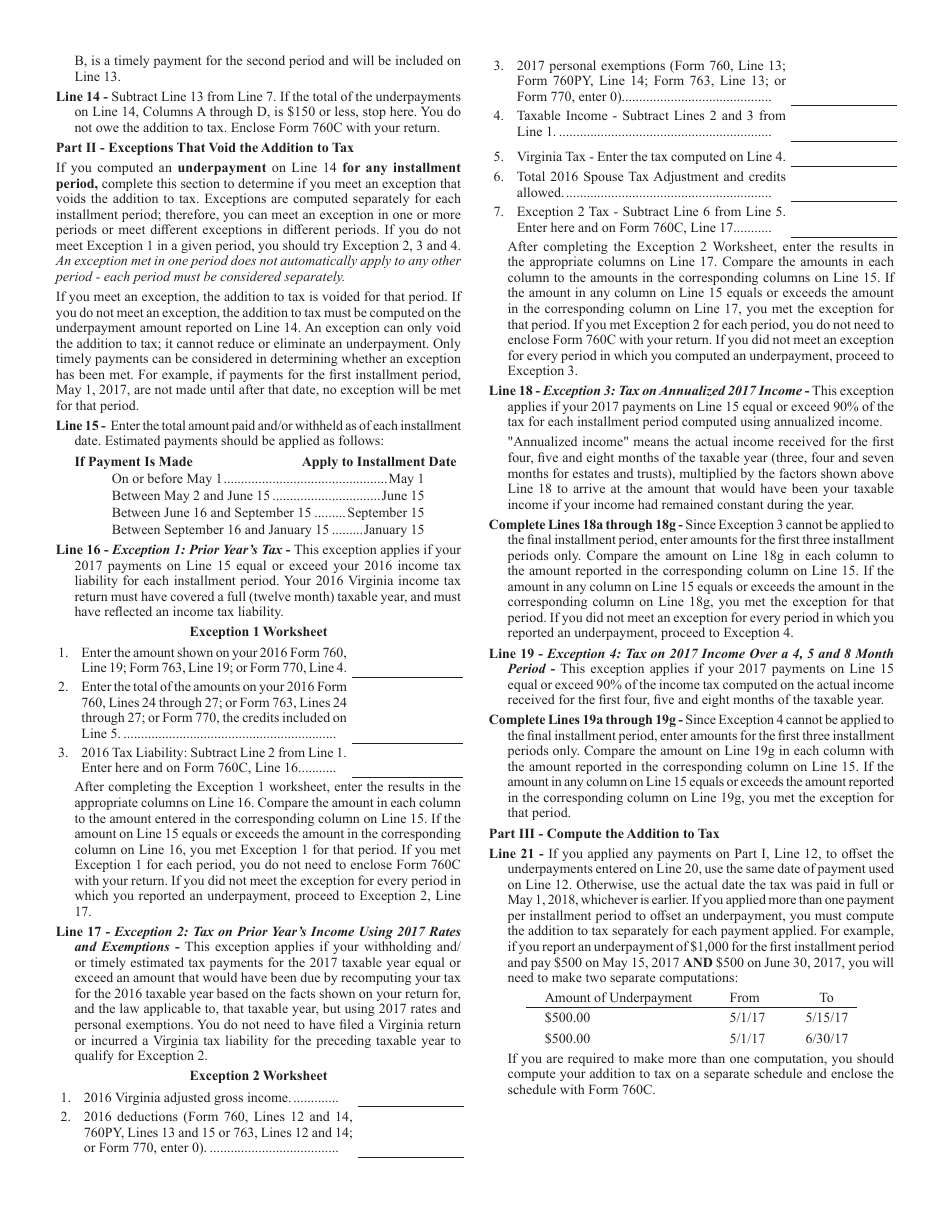

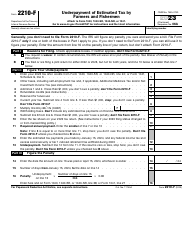

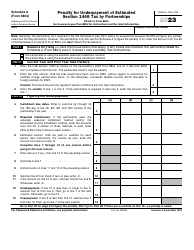

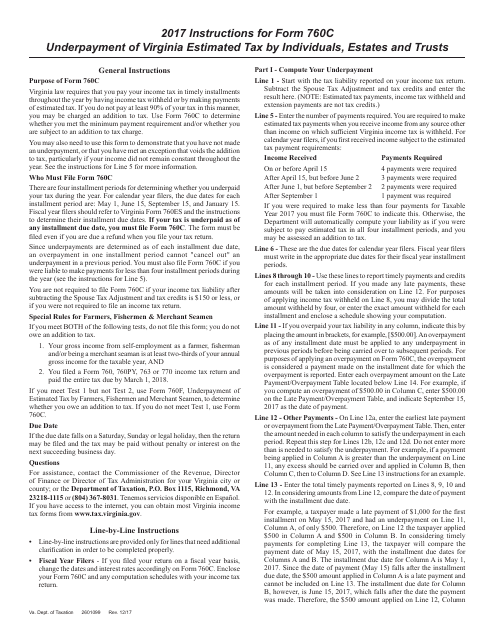

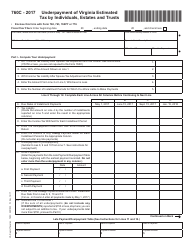

Instructions for Form 760C Underpayment of Virginia Estimated Tax by Individuals, Estates and Trusts - Virginia

This document contains official instructions for Form 760C , Underpayment of Virginia Estimated Tax by Individuals, Estates and Trusts - a form released and collected by the Virginia Department of Taxation. An up-to-date fillable Form 760C is available for download through this link.

FAQ

Q: What is Form 760C?

A: Form 760C is a form used to report underpayment of Virginia estimated tax by individuals, estates, and trusts.

Q: Who needs to fill out Form 760C?

A: Individuals, estates, and trusts who have underpaid their Virginia estimated tax must fill out Form 760C.

Q: What is considered an underpayment of Virginia estimated tax?

A: Underpayment of Virginia estimated tax occurs when the amount of tax paid throughout the year is less than the required amount.

Q: When is Form 760C due?

A: Form 760C is generally due by the same date as your Virginia income tax return, which is May 1st.

Q: What happens if I don't file Form 760C?

A: Failure to file Form 760C may result in penalties and interest on the underpaid amount.

Q: What documents do I need to complete Form 760C?

A: You will need your Virginia income tax return, your federal income tax return, and any other supporting documentation related to your estimated tax payments.

Q: Can I make a payment with Form 760C?

A: Yes, you can include a payment for the underpaid amount with Form 760C.

Instruction Details:

- This 2-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Virginia Department of Taxation.

Download Instructions for Form 760C Underpayment of Virginia Estimated Tax by Individuals, Estates and Trusts - Virginia

1

2