![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1120-PC Schedule M-3

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1120-PC Schedule M-3

for the current year.

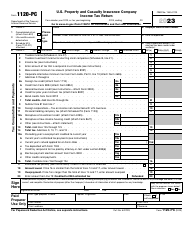

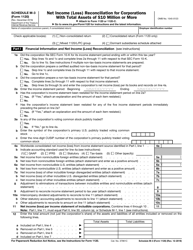

Instructions for IRS Form 1120-PC Schedule M-3 Net Income (Loss) Reconciliation for U.S. Property and Casualty Insurance Companies With Total Assets of $10 Million or More

This document contains official instructions for IRS Form 1120-PC Schedule M-3, Total Assets of $10 Million or More - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1120-PC Schedule M-3 is available for download through this link.

FAQ

Q: What is Form 1120-PC?

A: Form 1120-PC is used by U.S. property and casualtyinsurance companies to report their income (or loss) to the IRS.

Q: What is Schedule M-3?

A: Schedule M-3 is an additional form that must be completed by U.S. property and casualty insurance companies with total assets of $10 million or more.

Q: What is the purpose of Schedule M-3?

A: Schedule M-3 is used to reconcile the net income (or loss) reported on Form 1120-PC with the financial statement income (or loss) of the company.

Q: Who is required to complete Schedule M-3?

A: U.S. property and casualty insurance companies with total assets of $10 million or more are required to complete Schedule M-3.

Q: What information do I need to complete Schedule M-3?

A: You will need your company's financial statements, income tax return, and other relevant financial information to complete Schedule M-3.

Q: Are there any penalties for not completing Schedule M-3?

A: Yes, there may be penalties for failure to complete Schedule M-3 or for inaccurately completing the form.

Q: Can I file Form 1120-PC without completing Schedule M-3?

A: No, if you are required to complete Schedule M-3, it must be included with your Form 1120-PC filing.

Q: Can I request an extension to file Form 1120-PC and Schedule M-3?

A: Yes, you can request an extension to file Form 1120-PC and Schedule M-3 using Form 7004.

Instruction Details:

- This 24-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 1120-PC Schedule M-3 Net Income (Loss) Reconciliation for U.S. Property and Casualty Insurance Companies With Total Assets of $10 Million or More

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24