![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8844

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8844

for the current year.

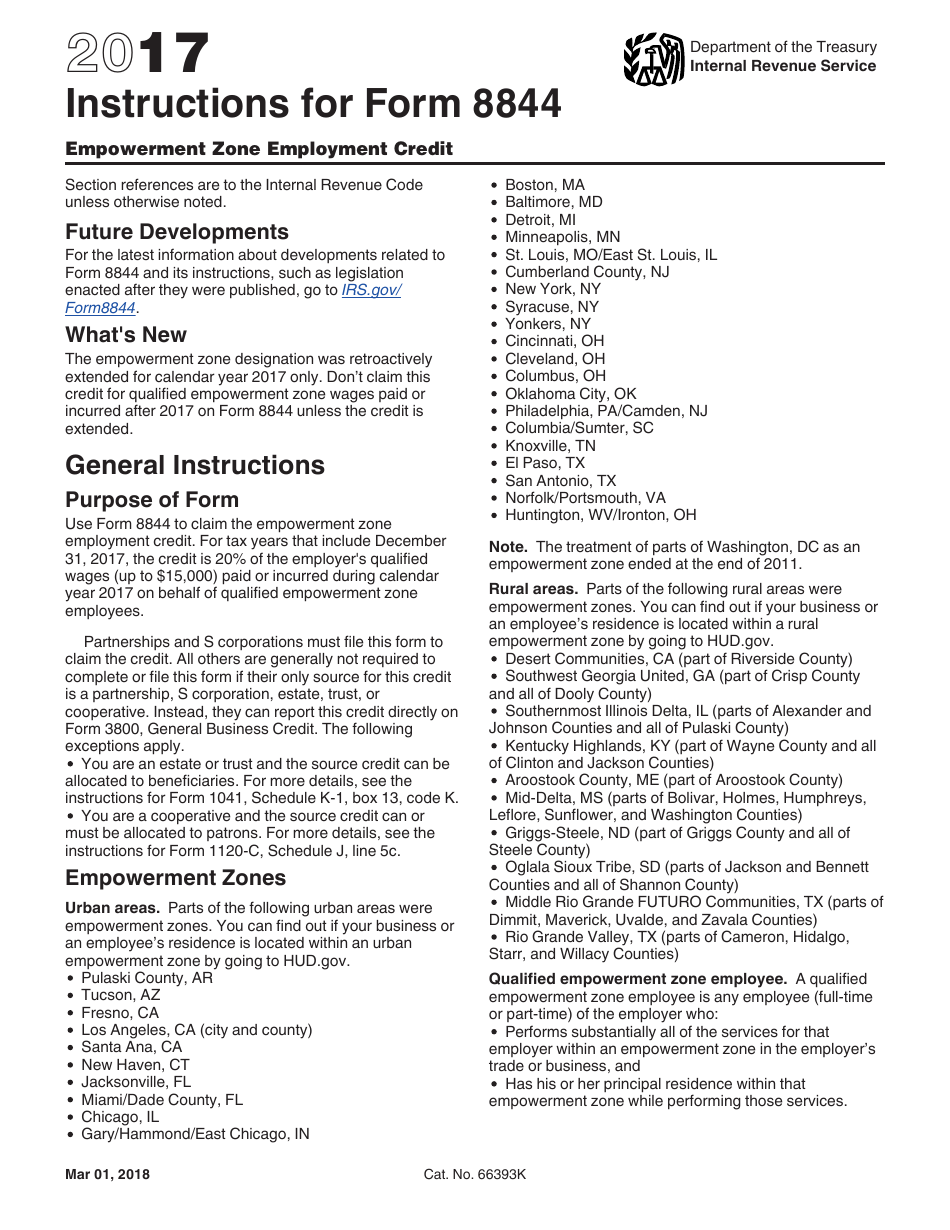

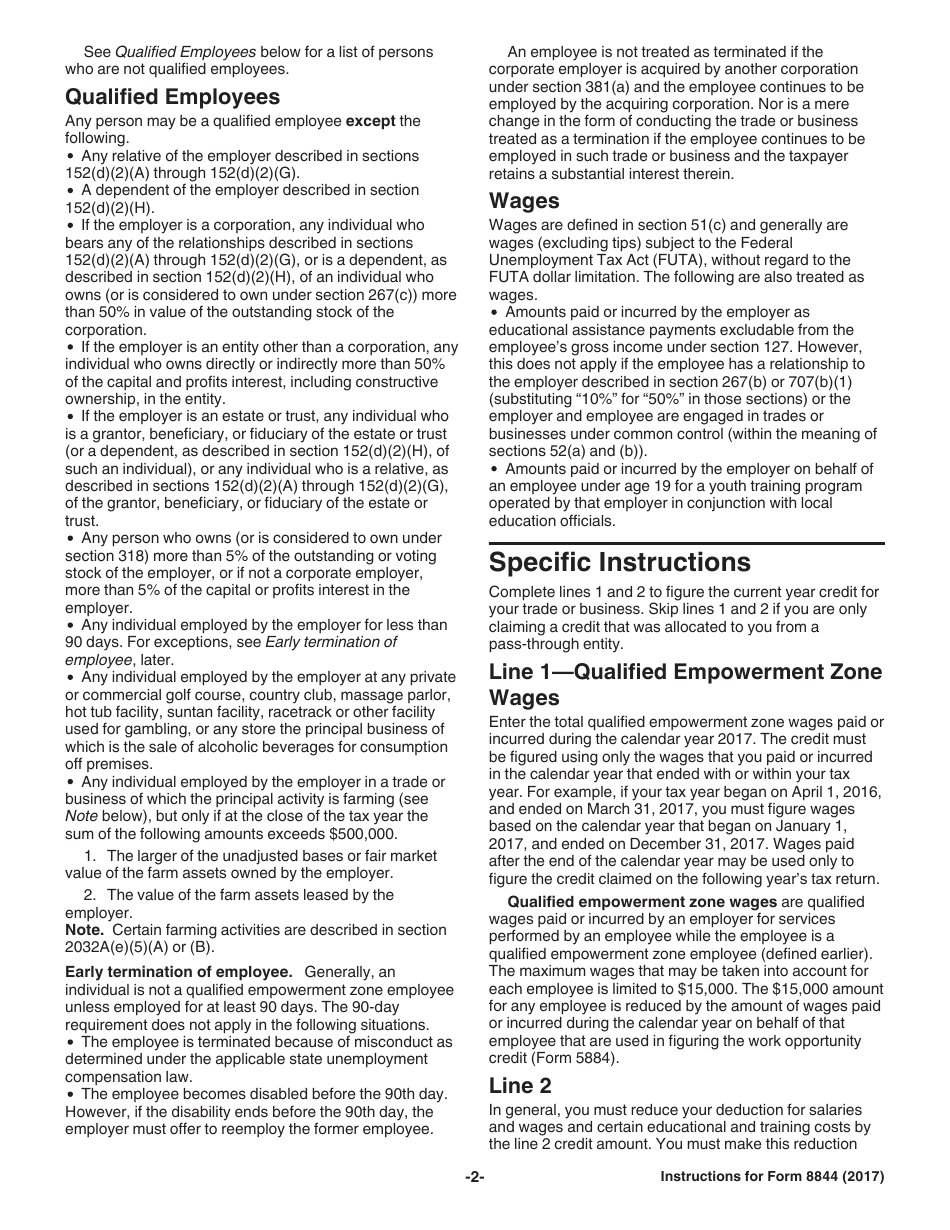

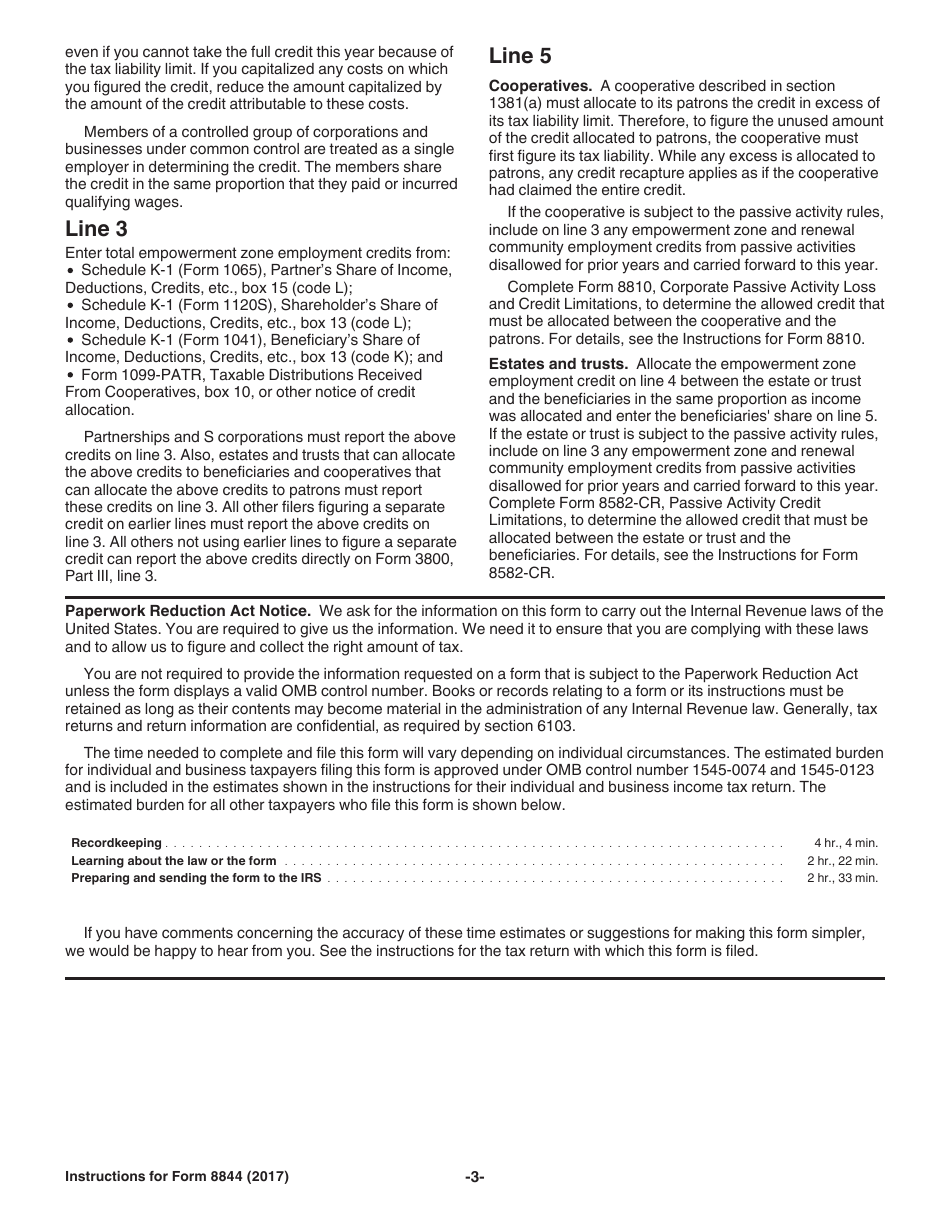

Instructions for IRS Form 8844 Empowerment Zone Employment Credit

This document contains official instructions for IRS Form 8844 , Empowerment Zone Employment Credit - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8844 is available for download through this link.

FAQ

Q: What is IRS Form 8844?

A: IRS Form 8844 is a tax form used to claim the Empowerment Zone Employment Credit.

Q: What is the Empowerment Zone Employment Credit?

A: The Empowerment Zone Employment Credit is a tax credit available to businesses that hire employees within designated empowerment zones.

Q: Who can claim the Empowerment Zone Employment Credit?

A: Businesses located in designated empowerment zones can claim this credit if they meet certain criteria.

Q: What are the criteria to qualify for the Empowerment Zone Employment Credit?

A: To qualify, businesses must hire employees who live and perform most of their work within the designated empowerment zones.

Q: How do I complete IRS Form 8844?

A: The form requires information about the business, the number of qualified employees hired, and the wages paid to them.

Q: When is the deadline to file IRS Form 8844?

A: The form must be filed with your business tax return, which is typically due on the 15th day of the fourth month after the end of the tax year.

Q: What other documentation do I need to submit with IRS Form 8844?

A: You may need to include additional documents, such as proof of employment and residency for qualified employees.

Q: Is there a limit to the amount of credit I can claim?

A: Yes, the credit is limited to a certain percentage of the wages paid to qualified employees.

Q: Can the Empowerment Zone Employment Credit be carried forward or backward?

A: No, this credit cannot be carried forward or backward.

Instruction Details:

- This 3-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3