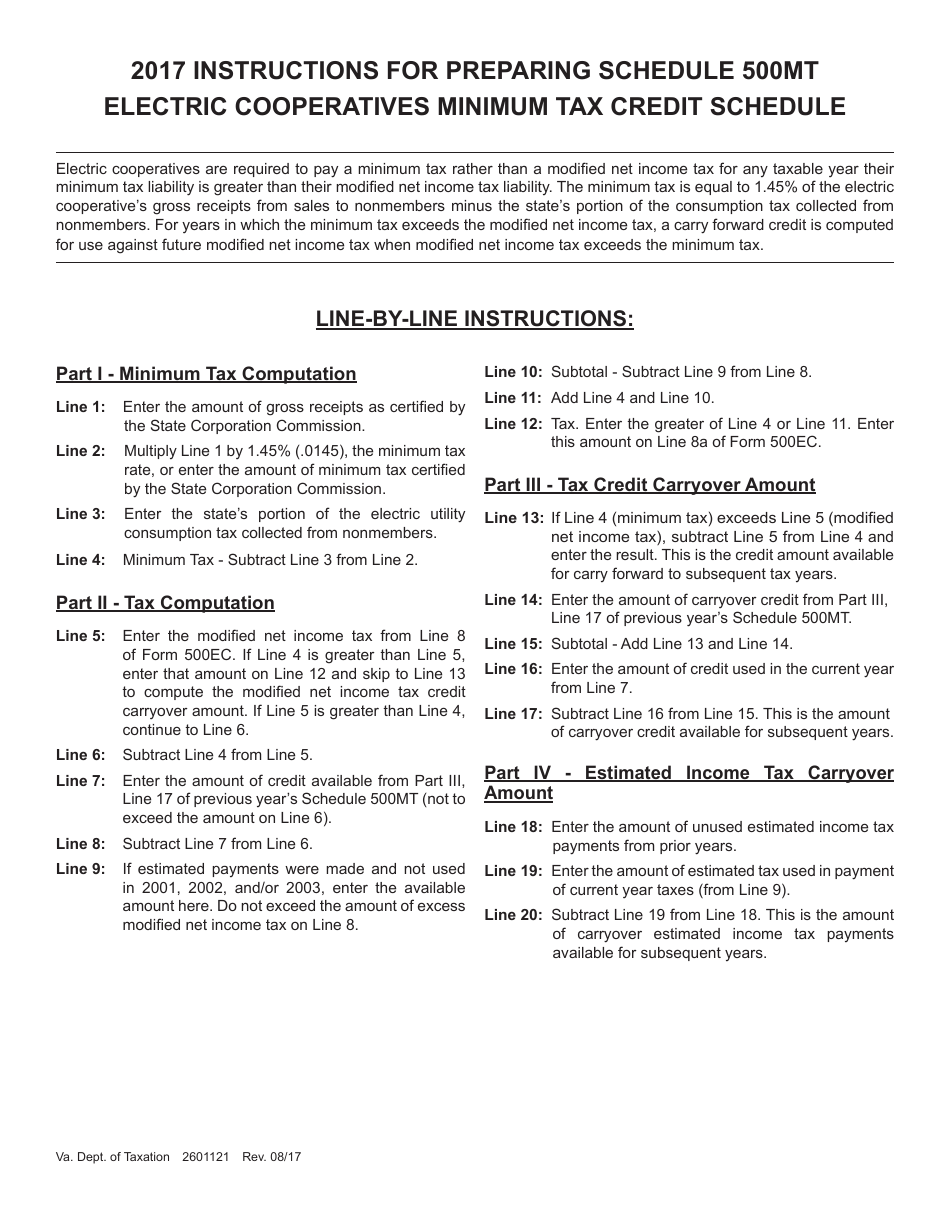

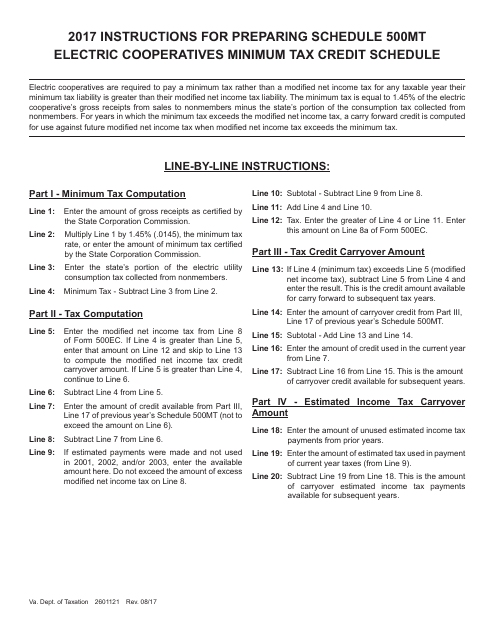

Instructions for Form 3201120-W Schedule 500MT Electric Cooperatives Minimum Tax Credit Schedule - Virginia

This document contains official instructions for Form 3201120-W Schedule 500MT, Minimum Tax Credit Schedule - a form released and collected by the Virginia Department of Taxation.

FAQ

Q: What is Form 3201120-W?

A: Form 3201120-W is a schedule for reporting the Minimum Tax Credit for Electric Cooperatives in Virginia.

Q: Who needs to complete Form 3201120-W?

A: Electric cooperatives in Virginia need to complete Form 3201120-W if they are claiming the Minimum Tax Credit.

Q: What is the purpose of Form 3201120-W?

A: Form 3201120-W is used to calculate and report the Minimum Tax Credit for Electric Cooperatives in Virginia.

Q: What is the Minimum Tax Credit for Electric Cooperatives?

A: The Minimum Tax Credit is a tax credit available to electric cooperatives in Virginia to offset their payment of minimum tax.

Q: Are there any specific instructions for completing Form 3201120-W?

A: Yes, specific instructions for completing Form 3201120-W can be found in the official instructions document provided by the Virginia Department of Taxation.

Q: When is the deadline for filing Form 3201120-W?

A: The deadline for filing Form 3201120-W is usually the same as the deadline for filing the corresponding tax return for electric cooperatives in Virginia.

Instruction Details:

- This 1-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Virginia Department of Taxation.