![]() This version of the form is not currently in use and is provided for reference only. Download this version of

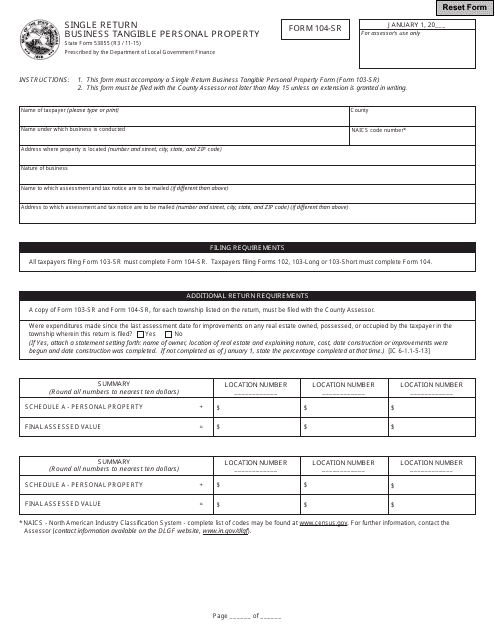

State Form 53855 (104-SR)

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

State Form 53855 (104-SR)

for the current year.

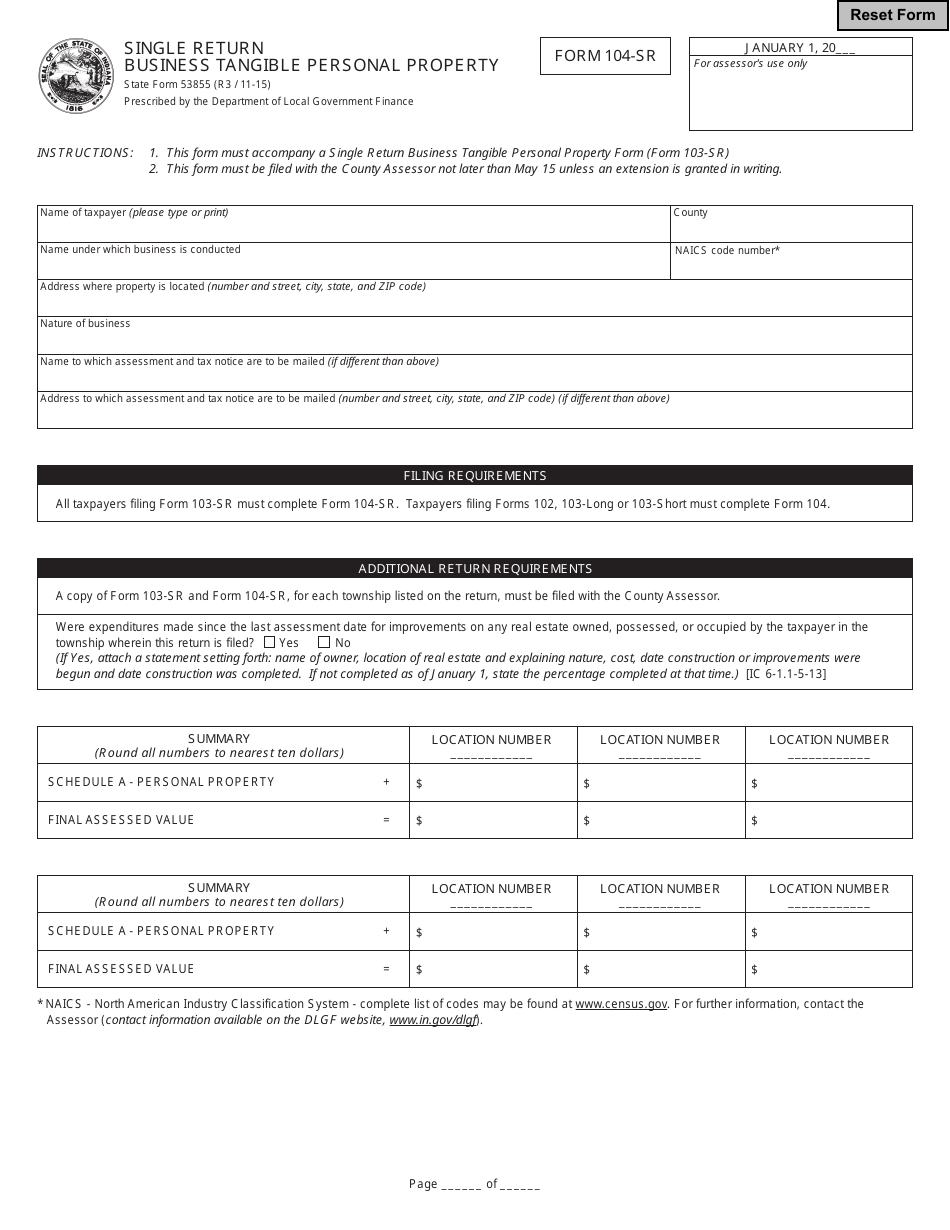

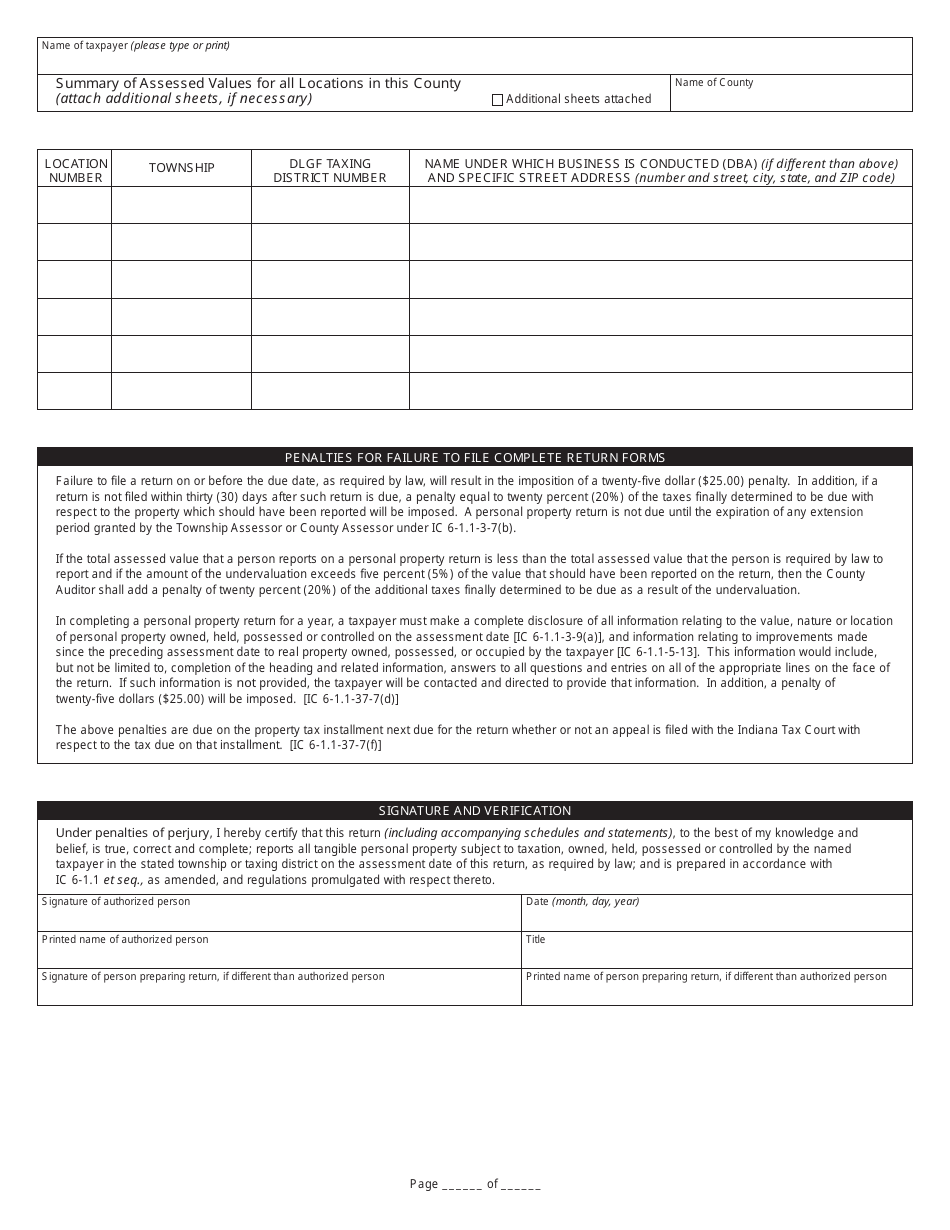

State Form 53855 (104-SR) Single Return Business Tangible Personal Property - Indiana

What Is State Form 53855 (104-SR)?

This is a legal form that was released by the Indiana Department of Local Government Finance - a government authority operating within Indiana. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 53855?

A: Form 53855 is the Single Return Business Tangible Personal Property form used in Indiana.

Q: Who needs to file Form 53855?

A: Businesses in Indiana that own tangible personal property need to file Form 53855.

Q: What is tangible personal property?

A: Tangible personal property refers to physical assets such as machinery, equipment, and furniture.

Q: What is the purpose of Form 53855?

A: The purpose of Form 53855 is to report the value of tangible personal property owned by a business in Indiana for tax assessment.

Q: How often do businesses need to file Form 53855?

A: Businesses need to file Form 53855 annually, by May 15th.

Q: Are there any exemptions to filing Form 53855?

A: Yes, certain businesses may be exempt from filing Form 53855. Contact the Indiana Department of Revenue for more information.

Q: Is there a penalty for not filing Form 53855?

A: Yes, there may be penalties for failure to file Form 53855 or filing it late. It's important to comply with the filing deadline.

Form Details:

- Released on November 1, 2015;

- The latest edition provided by the Indiana Department of Local Government Finance;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of State Form 53855 (104-SR) by clicking the link below or browse more documents and templates provided by the Indiana Department of Local Government Finance.

Download State Form 53855 (104-SR) Single Return Business Tangible Personal Property - Indiana

1

2