![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form IL-1040 Schedule F

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form IL-1040 Schedule F

for the current year.

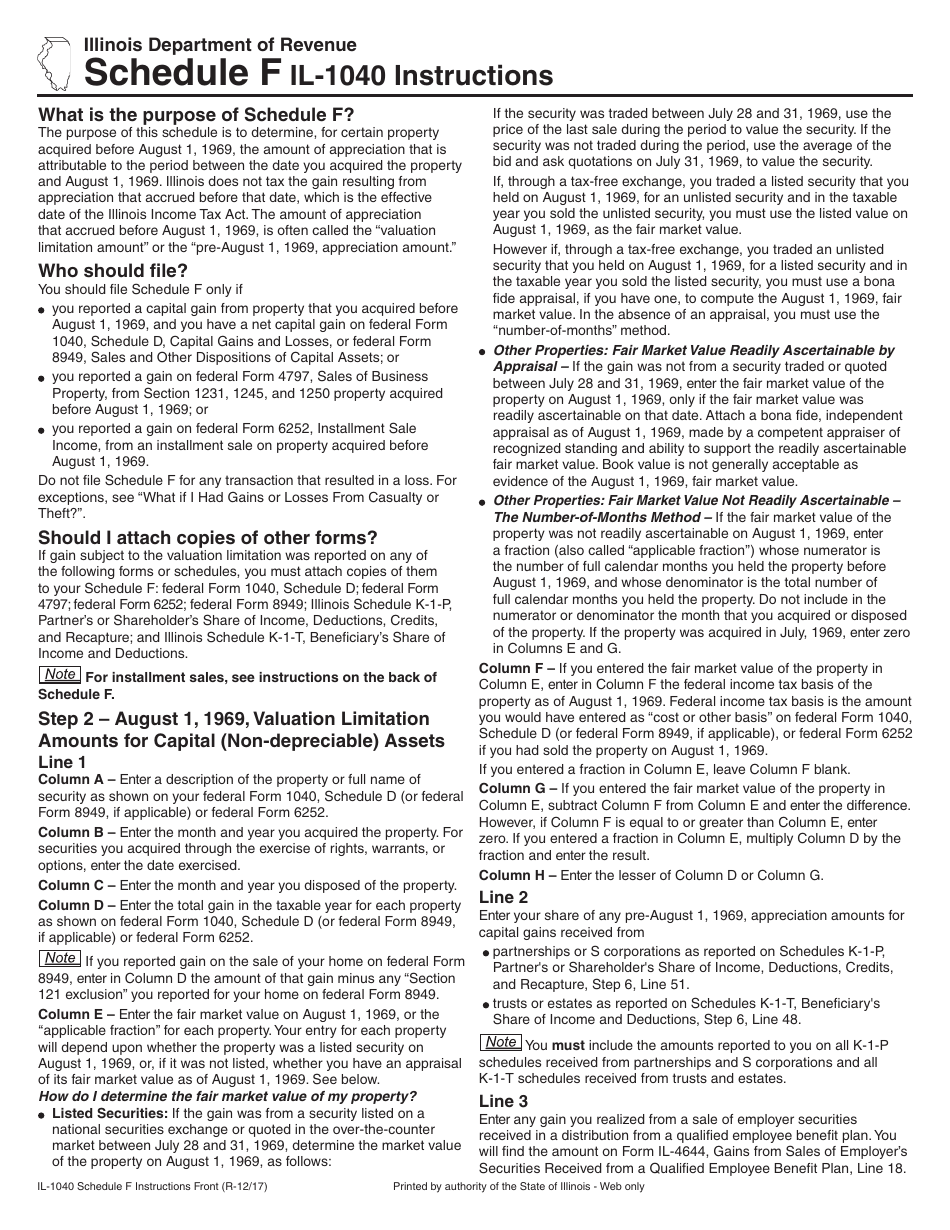

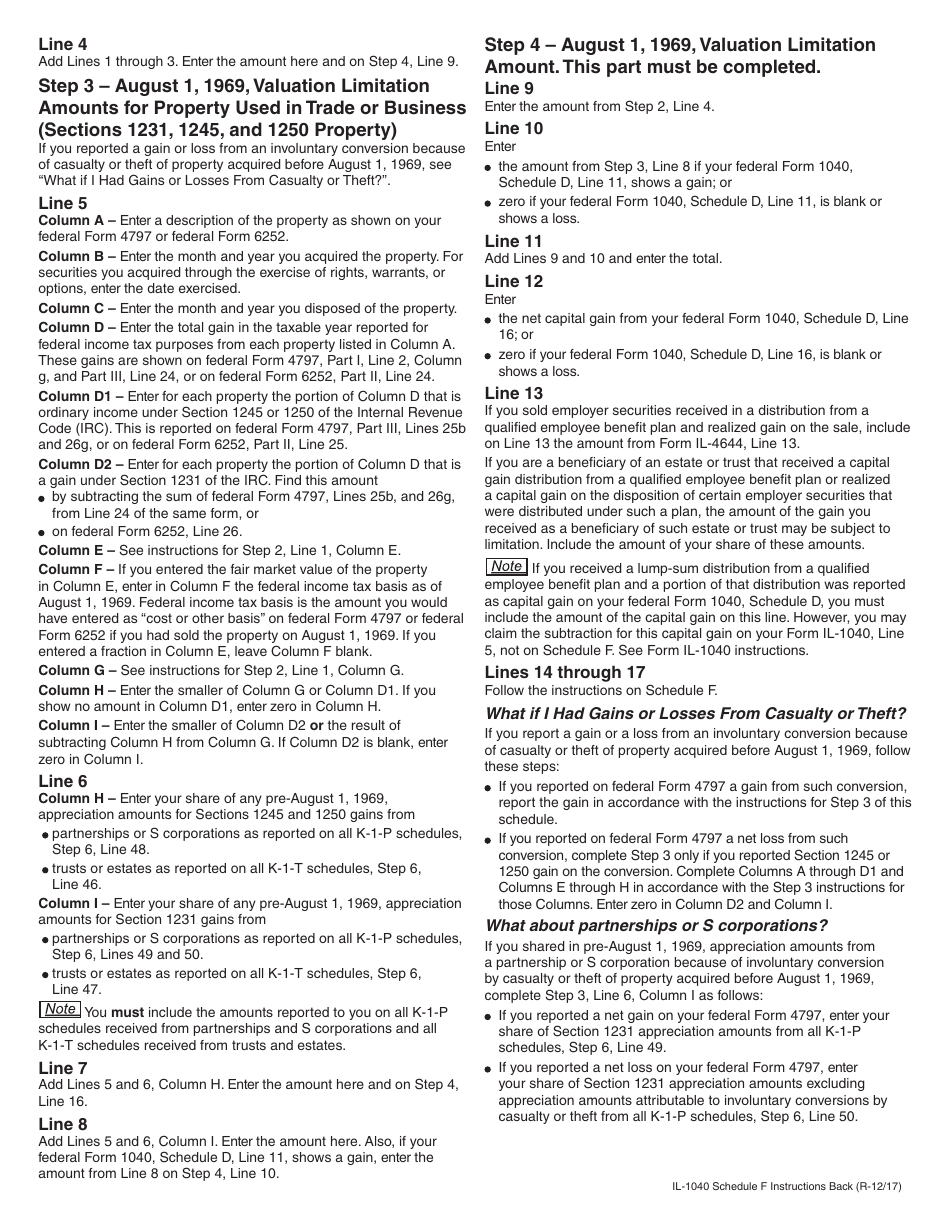

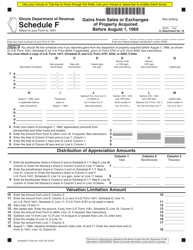

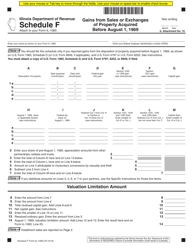

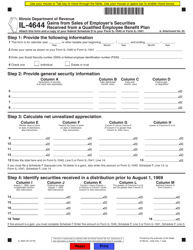

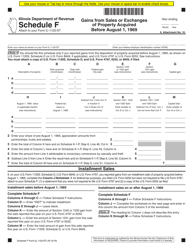

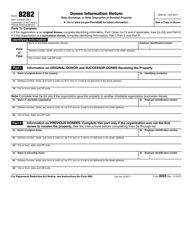

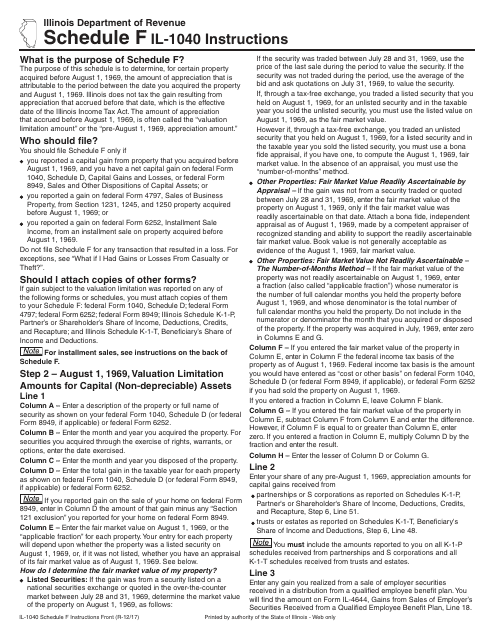

Instructions for Form IL-1040 Schedule F Gains From Sales or Exchanges of Property Acquired Before August 1, 1969 - Illinois

This document contains official instructions for Form IL-1040 Schedule F, Gains From Sales or Exchanges of Property Acquired Before August 1, 1969 - a form released and collected by the Illinois Department of Revenue. An up-to-date fillable Form IL-1040 Schedule F is available for download through this link.

FAQ

Q: What is Form IL-1040 Schedule F?

A: Form IL-1040 Schedule F is a form used in Illinois for reporting gains from sales or exchanges of property acquired before August 1, 1969.

Q: What does Schedule F on Form IL-1040 report?

A: Schedule F on Form IL-1040 reports gains from sales or exchanges of property acquired before August 1, 1969.

Q: Who needs to file Form IL-1040 Schedule F?

A: Individuals in Illinois who have gains from sales or exchanges of property acquired before August 1, 1969 need to file Form IL-1040 Schedule F.

Q: What is the purpose of Form IL-1040 Schedule F?

A: The purpose of Form IL-1040 Schedule F is to report and calculate the amount of gains from sales or exchanges of property acquired before August 1, 1969.

Q: When is Form IL-1040 Schedule F due?

A: Form IL-1040 Schedule F is due on the same date as the individual's Form IL-1040, which is April 15th of the following tax year.

Q: Are there any specific instructions for completing Form IL-1040 Schedule F?

A: Yes, there are specific instructions provided by the Illinois Department of Revenue that should be followed when completing Form IL-1040 Schedule F.

Q: Can I e-file Form IL-1040 Schedule F?

A: Yes, you can e-file Form IL-1040 Schedule F if you are filing your Form IL-1040 electronically.

Q: What should I do if I have additional questions about Form IL-1040 Schedule F?

A: If you have additional questions about Form IL-1040 Schedule F, you should contact the Illinois Department of Revenue for assistance.

Instruction Details:

- This 2-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Illinois Department of Revenue.

Download Instructions for Form IL-1040 Schedule F Gains From Sales or Exchanges of Property Acquired Before August 1, 1969 - Illinois

1

2