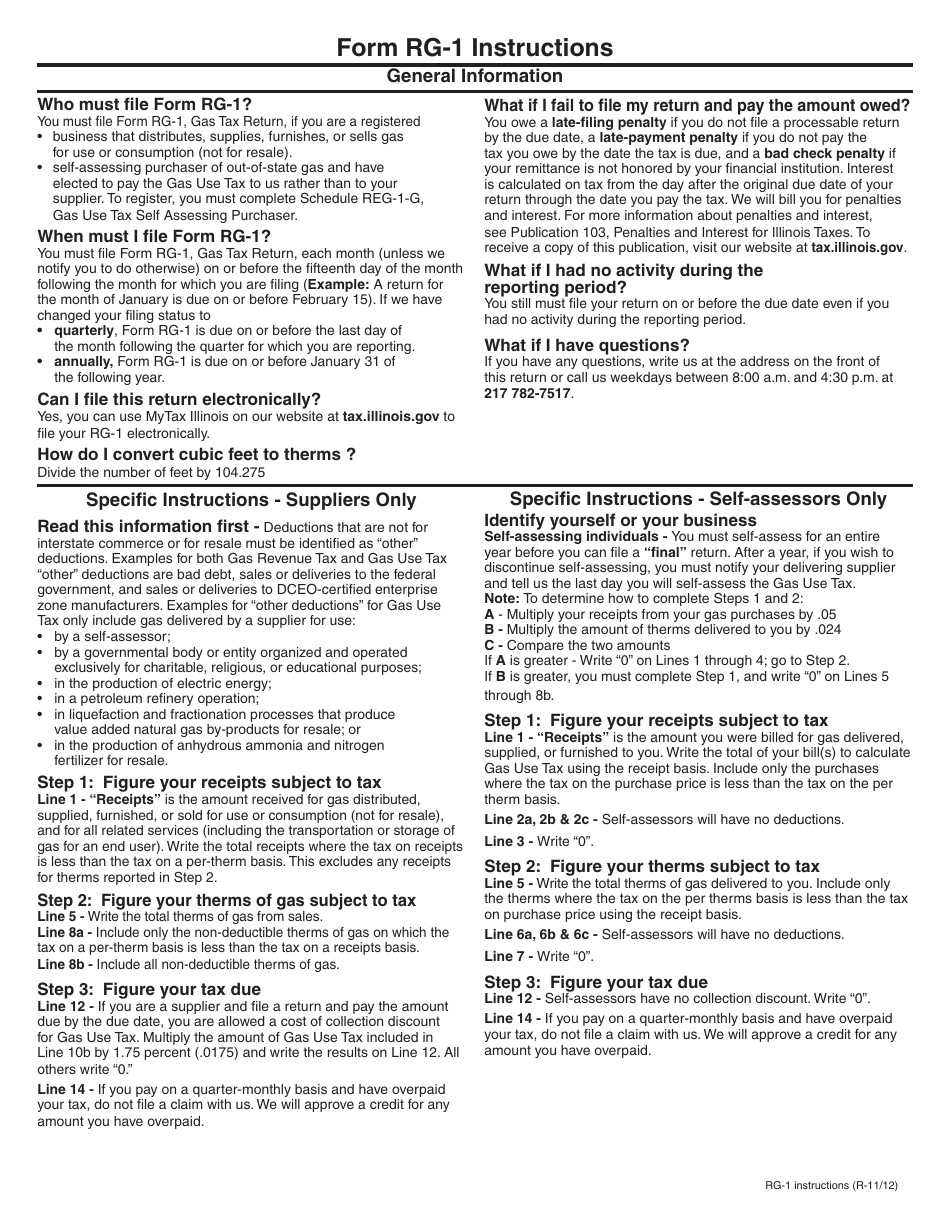

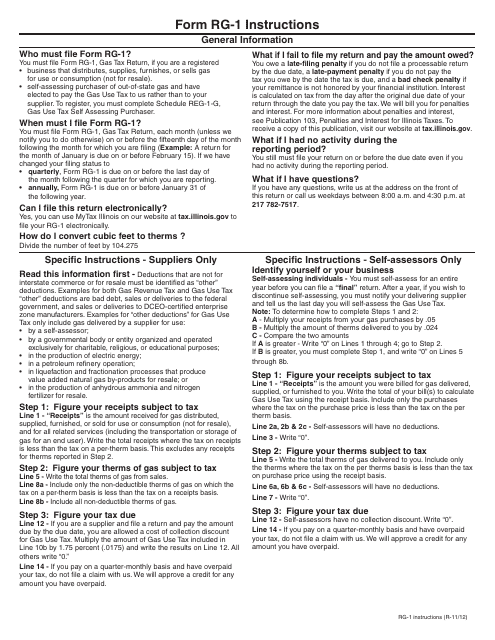

Instructions for Form RG-1 Gas Tax Return - Illinois

This document contains official instructions for Form RG-1 , Gas Tax Return - a form released and collected by the Illinois Department of Revenue.

FAQ

Q: What is Form RG-1?

A: Form RG-1 is a Gas Tax Return form used in Illinois.

Q: Who needs to file Form RG-1?

A: Anyone who sells or distributes gasoline in Illinois needs to file Form RG-1.

Q: What is the purpose of Form RG-1?

A: The purpose of Form RG-1 is to report and pay the Illinois gas tax.

Q: How often do I need to file Form RG-1?

A: Form RG-1 must be filed monthly.

Q: What information do I need to provide on Form RG-1?

A: You need to provide information about the fuel sold or distributed as well as corresponding tax amounts.

Q: What is the due date for submitting Form RG-1?

A: Form RG-1 must be submitted by the 20th day of the following month.

Q: What are the consequences of not filing Form RG-1?

A: Failure to file Form RG-1 may result in penalties and interest charges.

Q: Is there any other documentation required with Form RG-1?

A: No, you only need to submit the completed Form RG-1.

Instruction Details:

- This 1-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Illinois Department of Revenue.