![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CIT

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CIT

for the current year.

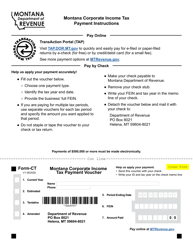

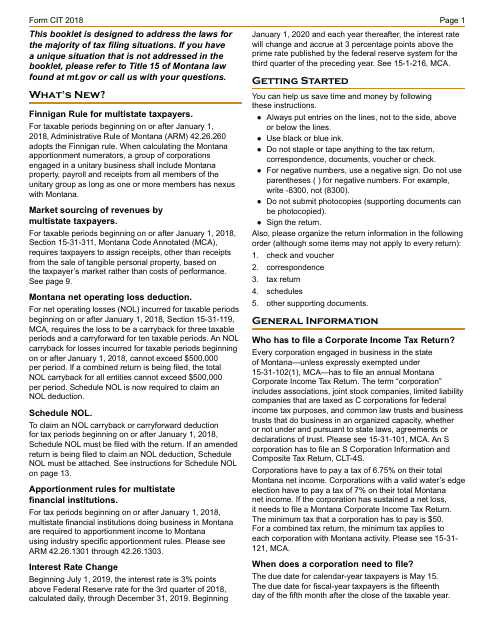

Instructions for Form CIT Montana Corporate Income Tax Return - Montana

This document contains official instructions for Form CIT , Montana Corporate Income Tax Return - a form released and collected by the Montana Department of Revenue. An up-to-date fillable Form CIT is available for download through this link.

FAQ

Q: What is Form CIT?

A: Form CIT is the Montana Corporate Income Tax Return.

Q: Who needs to file Form CIT?

A: All corporations doing business in Montana need to file Form CIT.

Q: What is the purpose of Form CIT?

A: Form CIT is used to report and calculate corporate incometax owed to the state of Montana.

Q: What information is required to complete Form CIT?

A: Form CIT requires information such as gross receipts, expenses, deductions, and credits.

Q: When is Form CIT due?

A: Form CIT is due on the 15th day of the fourth month following the close of the tax year.

Q: Are there any penalties for failing to file Form CIT?

A: Yes, there are penalties for failing to file Form CIT, including late filing penalties and interest on any unpaid taxes.

Q: Can I file Form CIT electronically?

A: Yes, Montana offers electronic filing options for Form CIT.

Q: Is there a minimum income threshold for filing Form CIT?

A: Yes, corporations with gross income of $1,800 or less are not required to file Form CIT.

Q: What if I need an extension to file Form CIT?

A: You can request a six-month extension to file Form CIT by submitting Form EXT-15 before the original due date.

Instruction Details:

- This 17-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Montana Department of Revenue.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17