![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 15

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 15

for the current year.

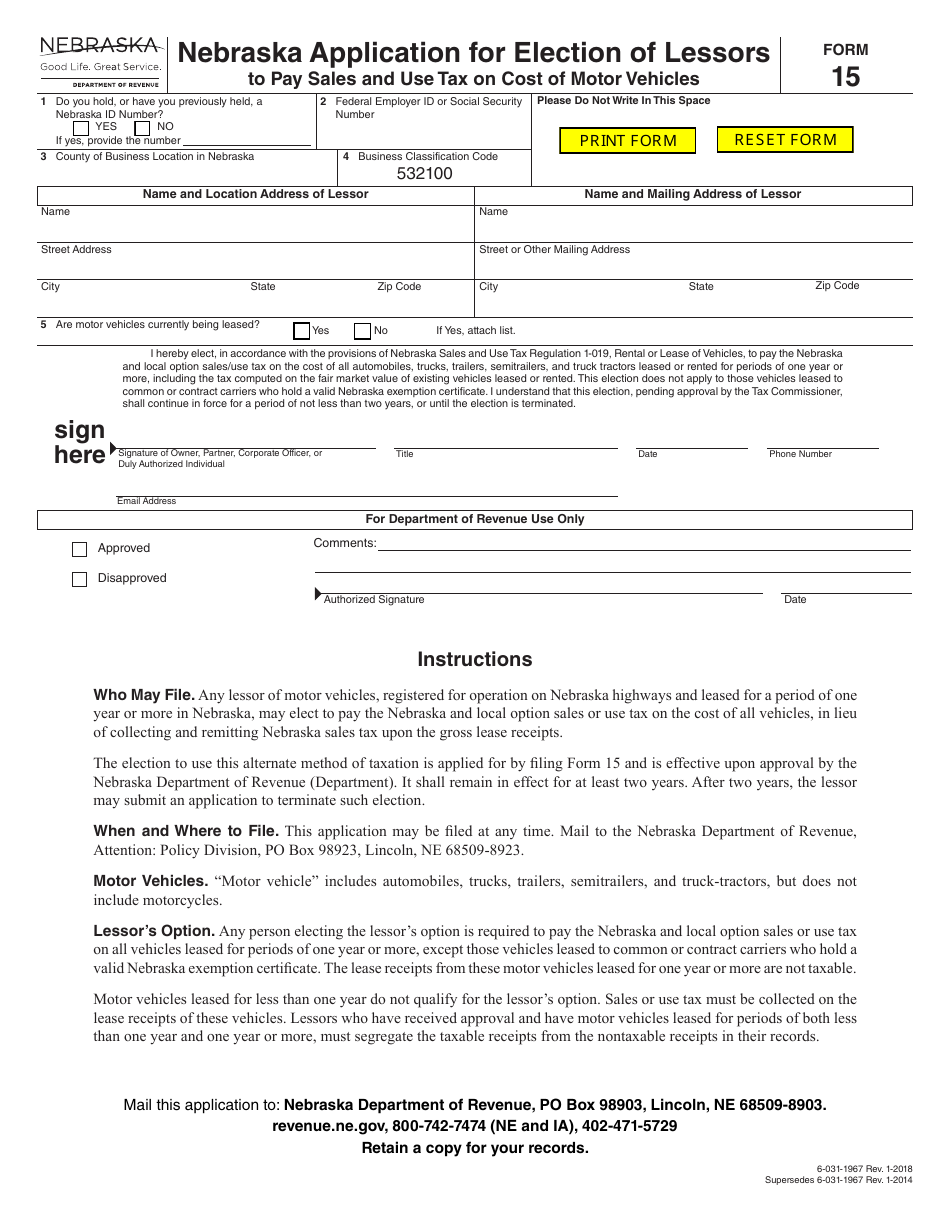

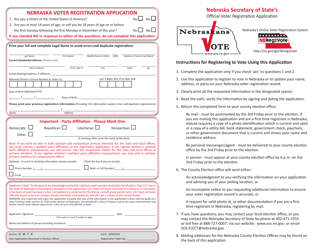

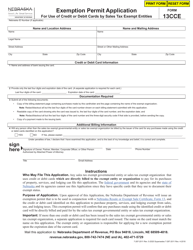

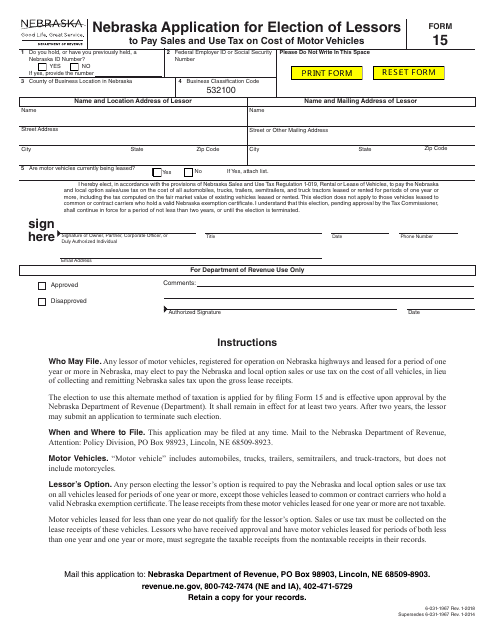

Form 15 Nebraska Application for Election of Lessors to Pay Sales and Use Tax on Cost of Motor Vehicles - Nebraska

What Is Form 15?

This is a legal form that was released by the Nebraska Department of Revenue - a government authority operating within Nebraska. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 15 Nebraska?

A: Form 15 Nebraska is an application for election of lessors to pay sales and use tax on the cost of motor vehicles.

Q: Who can use Form 15 Nebraska?

A: This form can be used by lessors who wish to elect to pay sales and use tax on the cost of motor vehicles.

Q: Why would someone use Form 15 Nebraska?

A: Someone would use Form 15 Nebraska to elect to pay sales and use tax on the cost of motor vehicles instead of having the lessee pay the tax.

Q: Is there a deadline to submit Form 15 Nebraska?

A: Yes, the form must be submitted within 30 days from the date the lease agreement is executed or the vehicle is first leased in Nebraska, whichever comes later.

Q: Are there any fees associated with submitting Form 15 Nebraska?

A: There are no fees associated with submitting Form 15 Nebraska.

Form Details:

- Released on January 1, 2018;

- The latest edition provided by the Nebraska Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 15 by clicking the link below or browse more documents and templates provided by the Nebraska Department of Revenue.

Download Form 15 Nebraska Application for Election of Lessors to Pay Sales and Use Tax on Cost of Motor Vehicles - Nebraska

1

2