![]() This version of the form is not currently in use and is provided for reference only. Download this version of

SBA Form 1920

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

SBA Form 1920

for the current year.

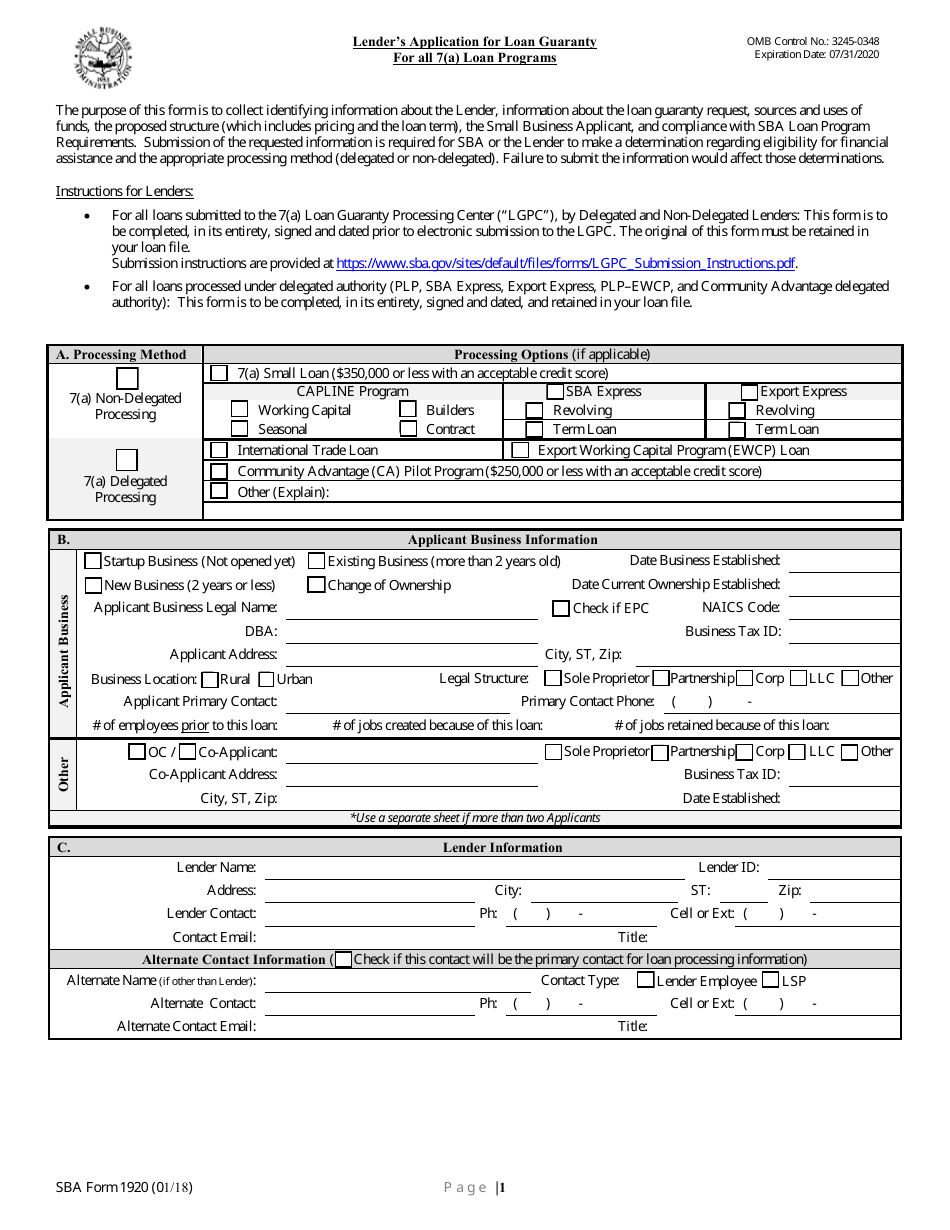

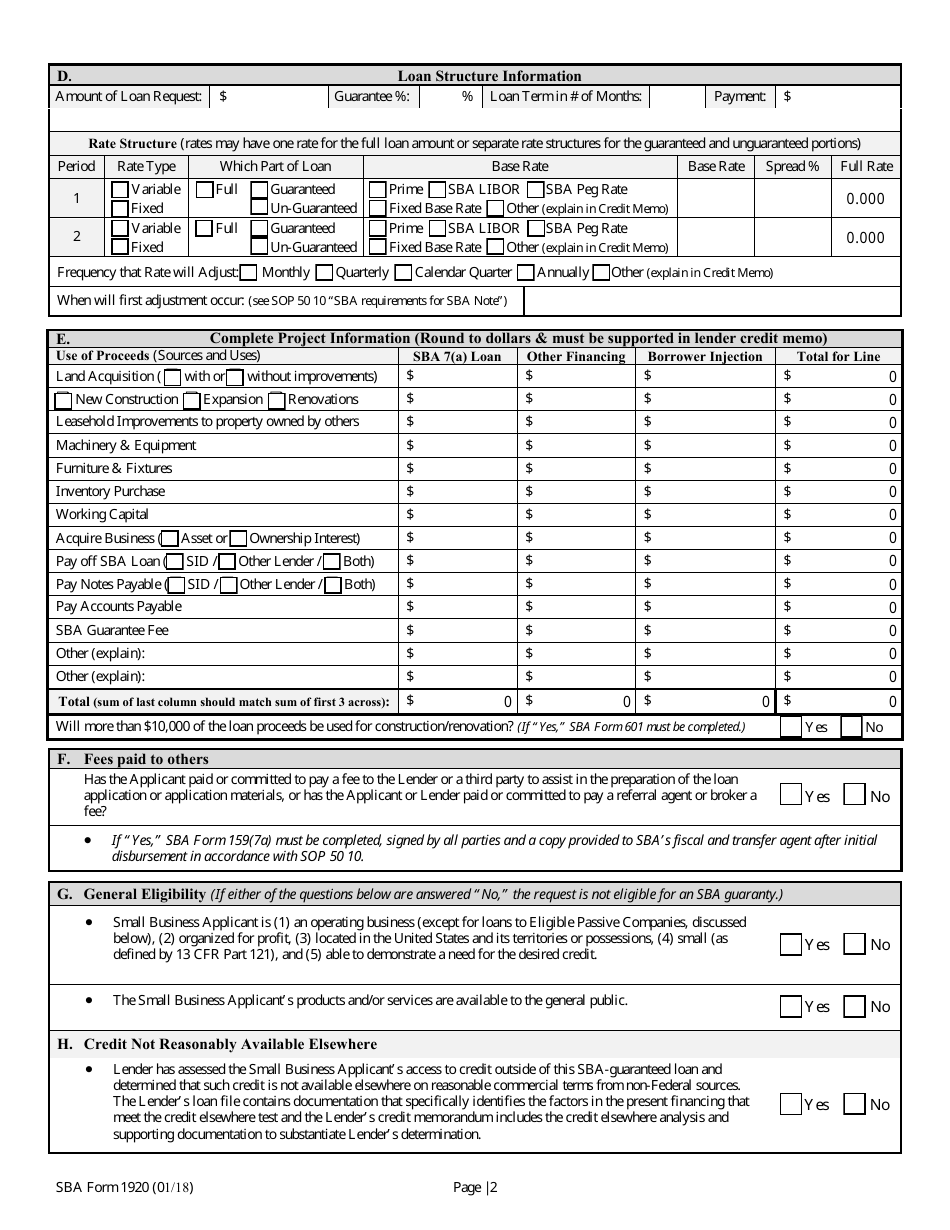

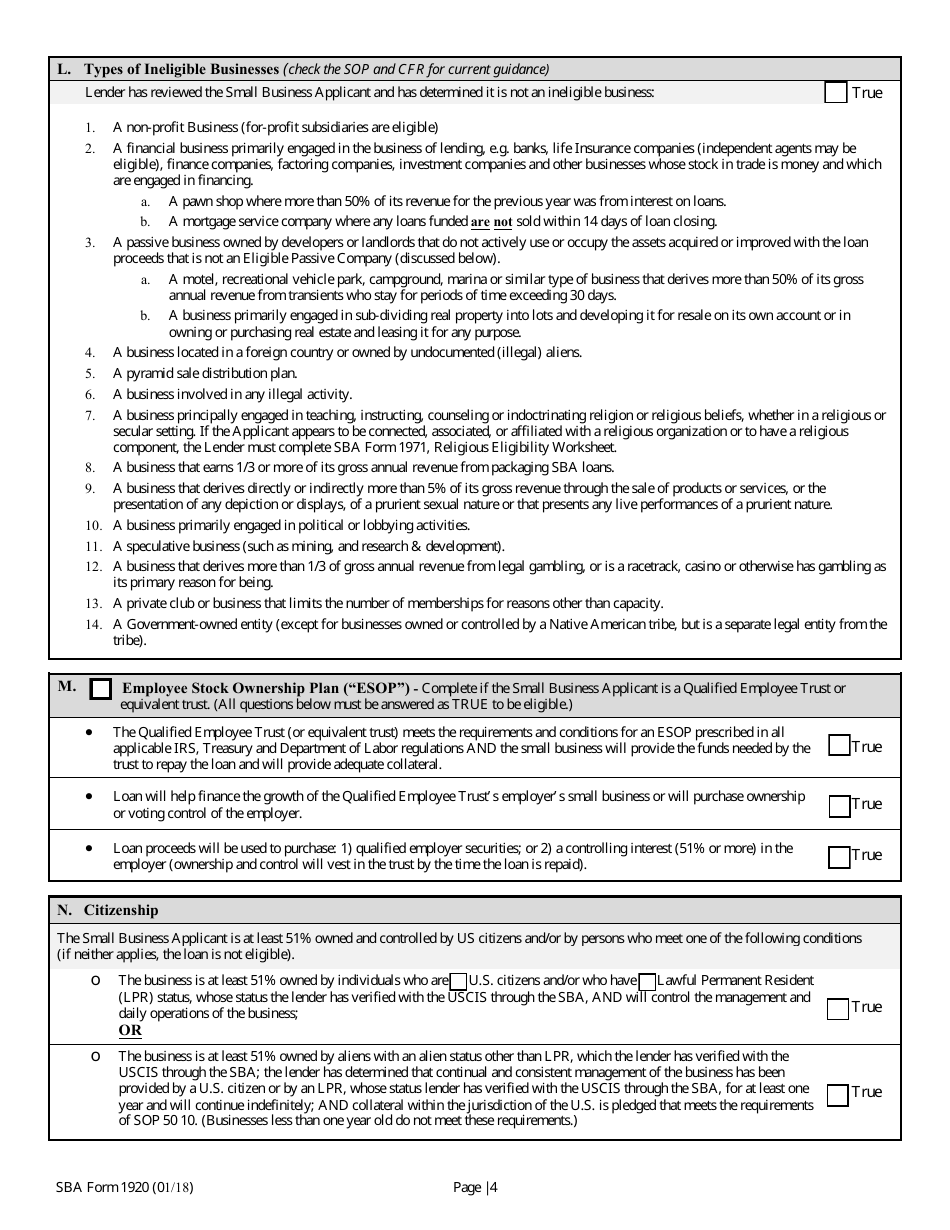

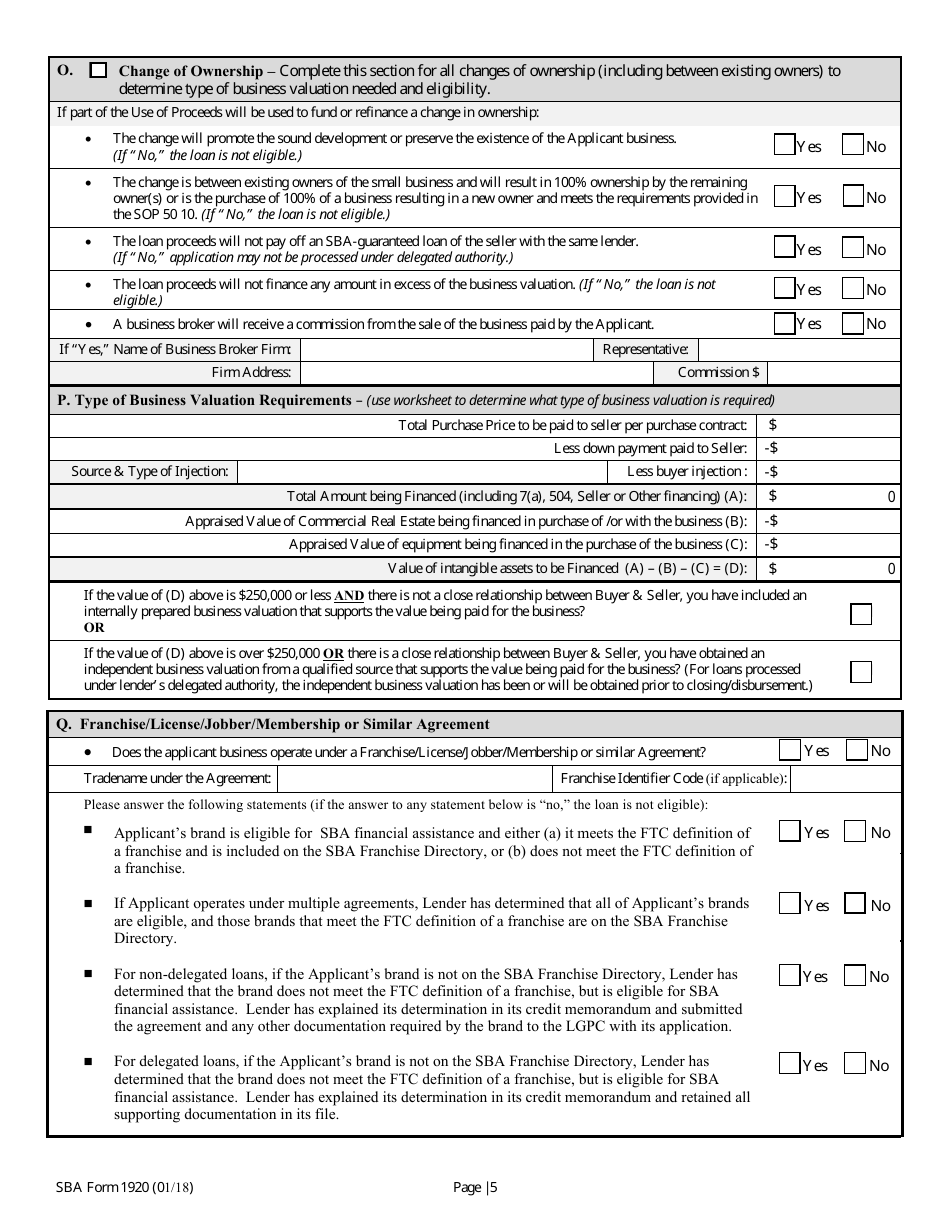

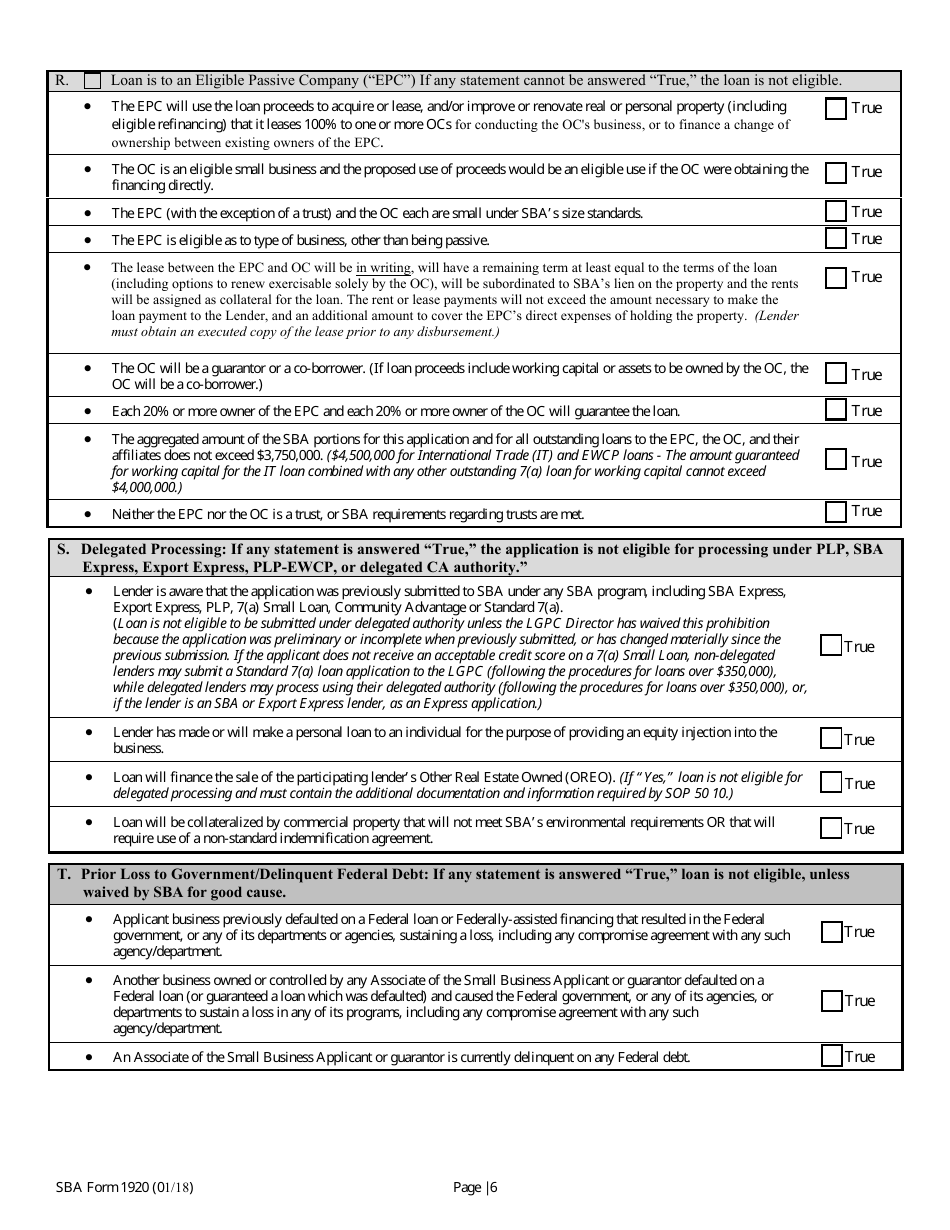

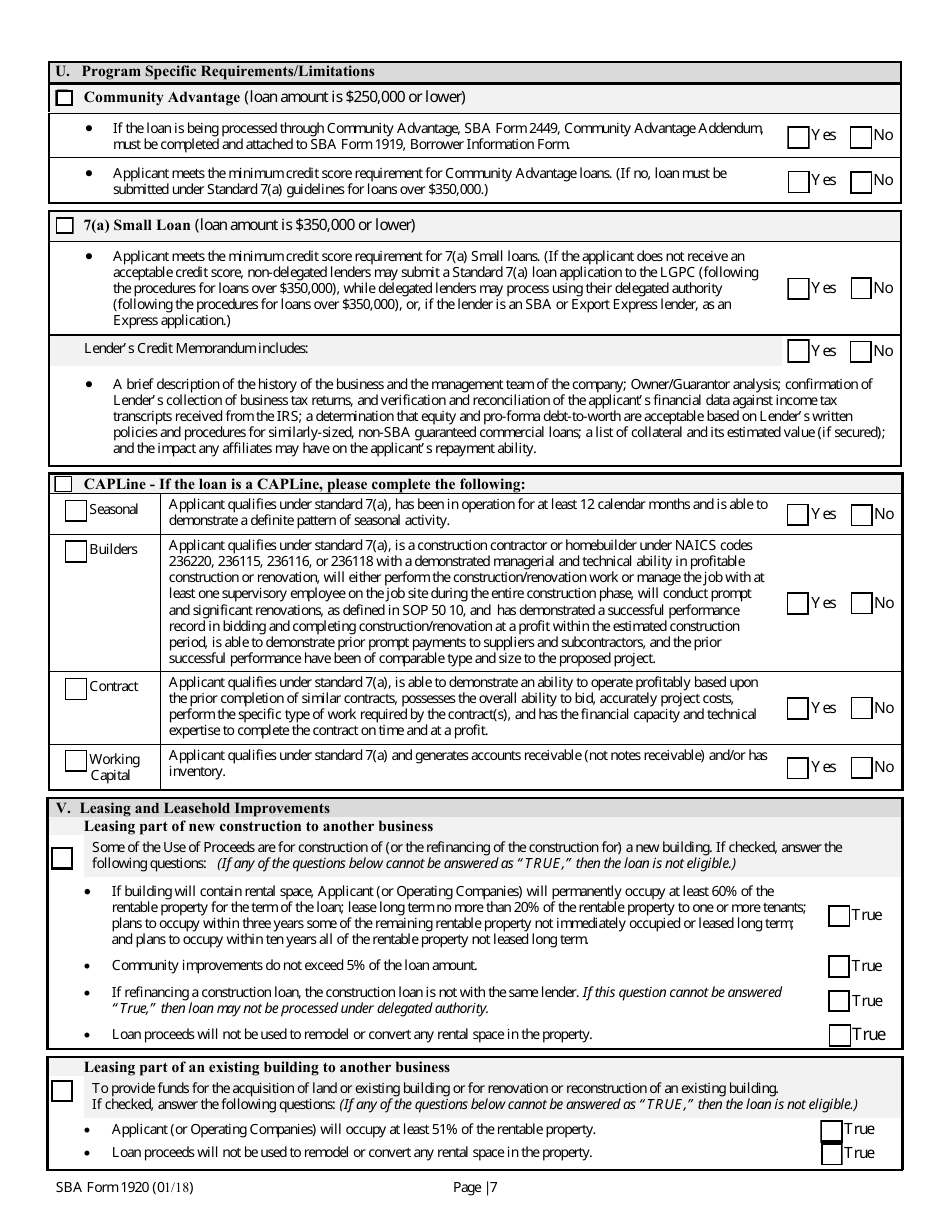

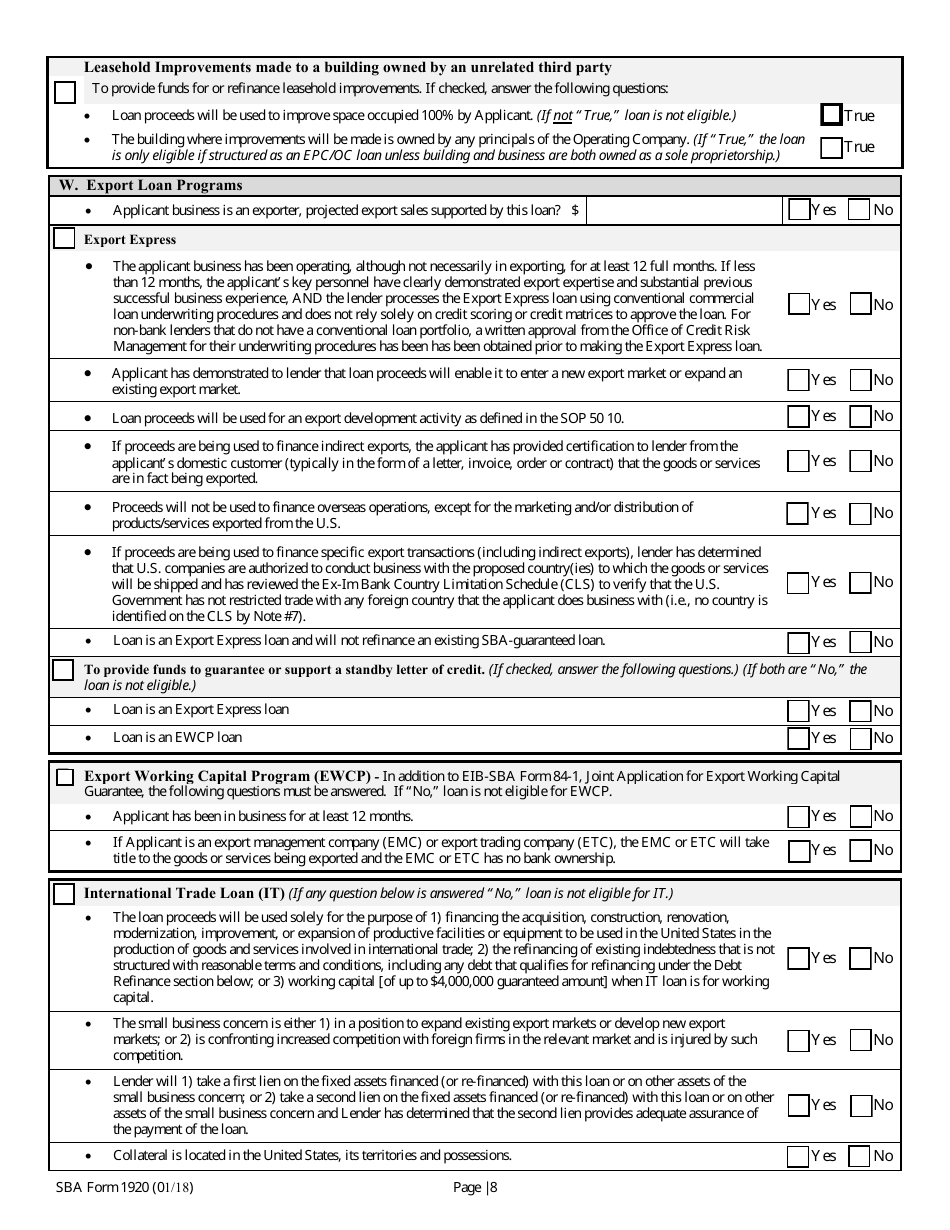

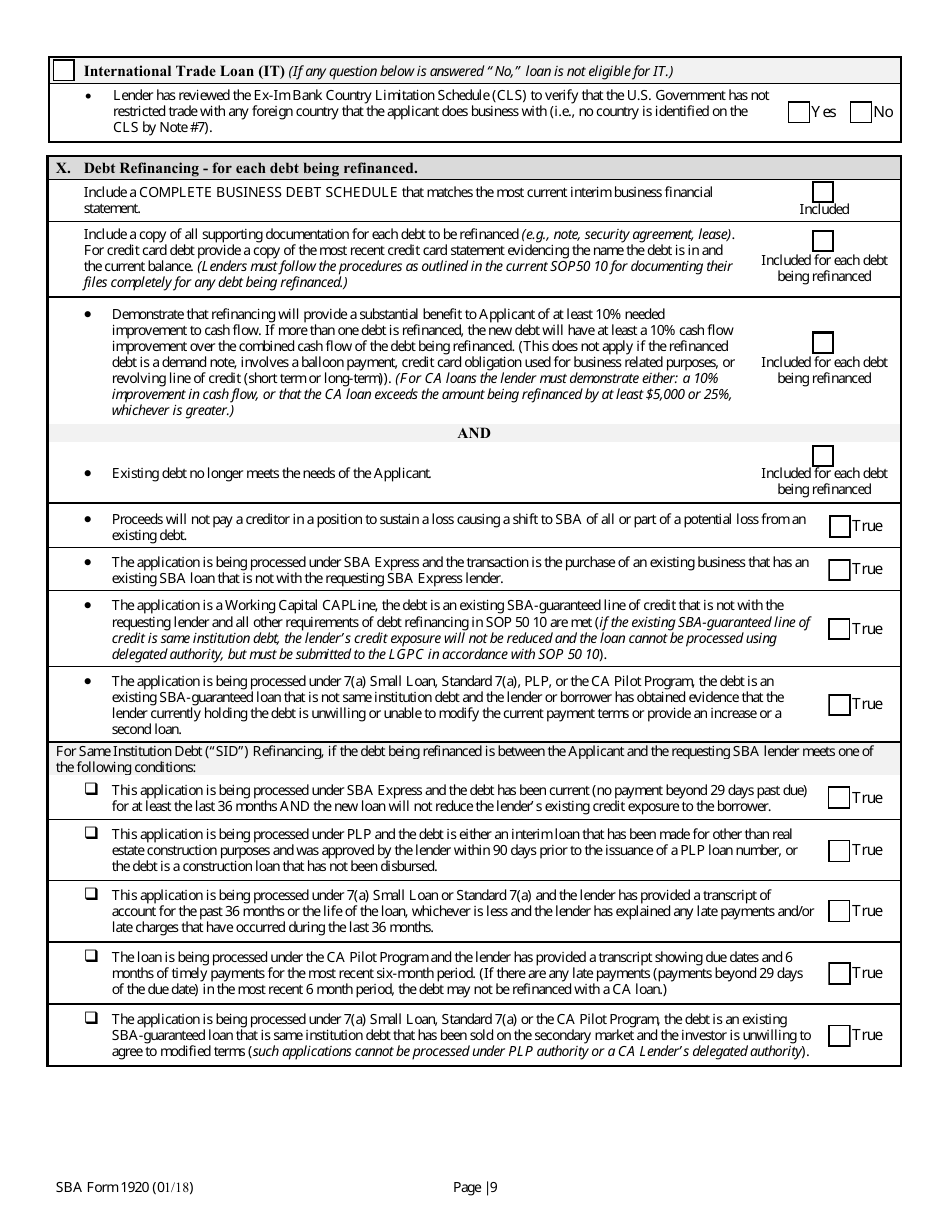

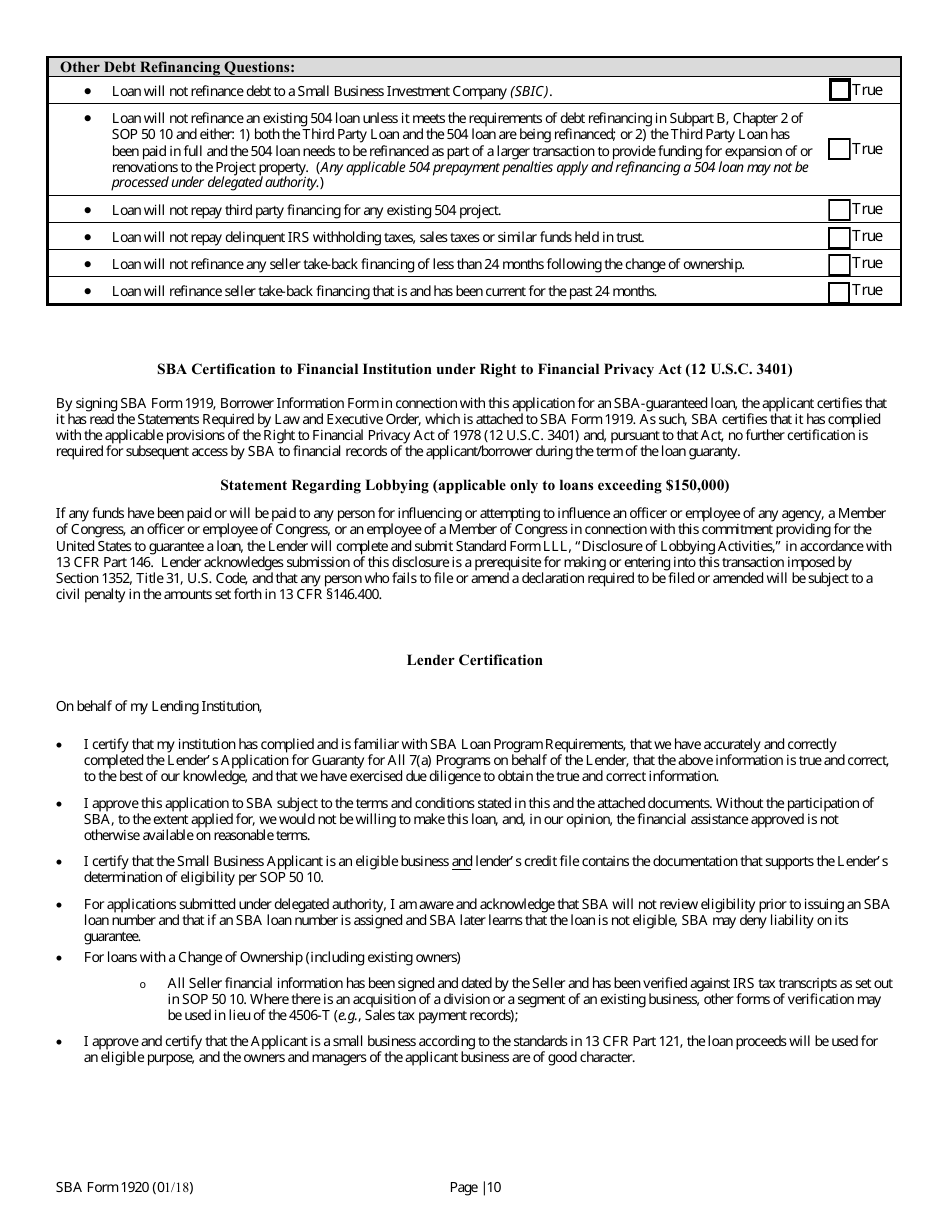

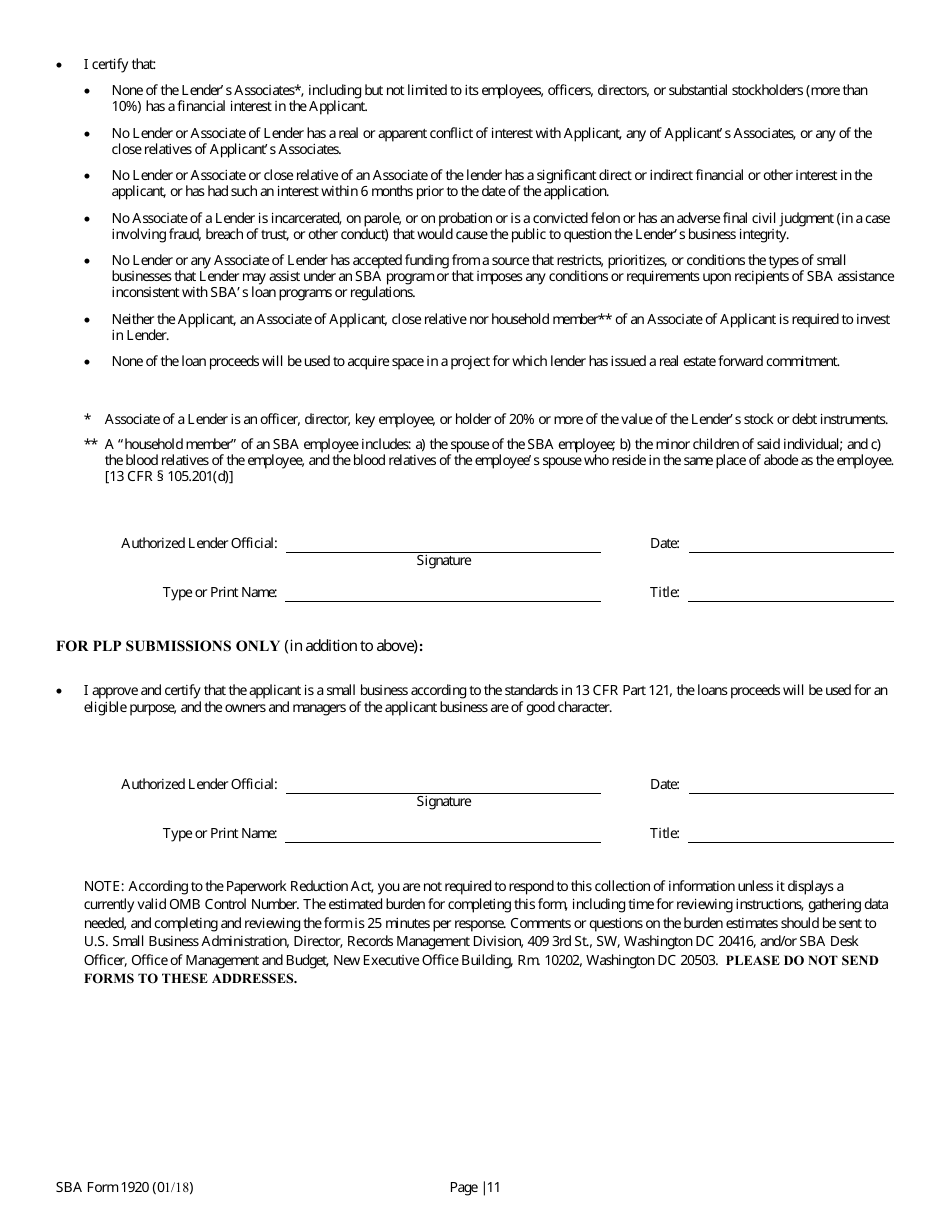

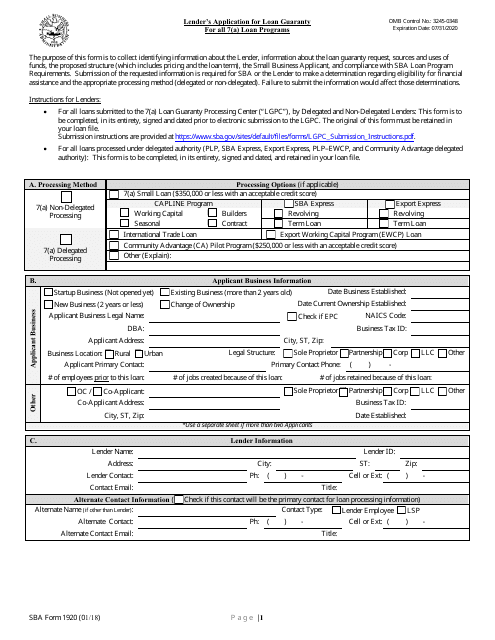

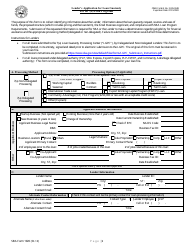

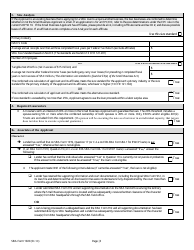

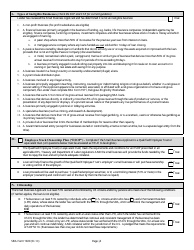

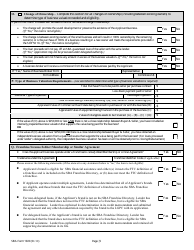

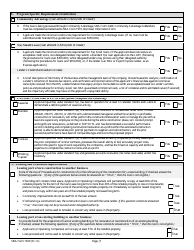

SBA Form 1920 Lender's Application for Loan Guaranty for All 7(A) Loan Programs

What Is SBA Form 1920?

This is a legal form that was released by the U.S. Small Business Administration on January 1, 2018 and used country-wide. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is SBA Form 1920?

A: SBA Form 1920 is the Lender's Application for Loan Guaranty for all 7(A) Loan Programs.

Q: What is the purpose of SBA Form 1920?

A: The purpose of SBA Form 1920 is to apply for a loan guaranty from the Small Business Administration (SBA) for the 7(A) Loan Programs.

Q: Who uses SBA Form 1920?

A: Lenders use SBA Form 1920 to apply for a loan guaranty from the SBA.

Q: What are the 7(A) Loan Programs?

A: The 7(A) Loan Programs are a series of loan programs offered by the SBA to help small businesses access capital.

Q: What information is required on SBA Form 1920?

A: SBA Form 1920 requires information about the lender, the borrower, the loan amount, and other details related to the loan application.

Form Details:

- Released on January 1, 2018;

- The latest available edition released by the U.S. Small Business Administration;

- Easy to use and ready to print;

- Yours to fill out and keep for your records;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of SBA Form 1920 by clicking the link below or browse more documents and templates provided by the U.S. Small Business Administration.

Download SBA Form 1920 Lender's Application for Loan Guaranty for All 7(A) Loan Programs

1

2

3

4

5

6

7

8

9

10

11