![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 4255

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 4255

for the current year.

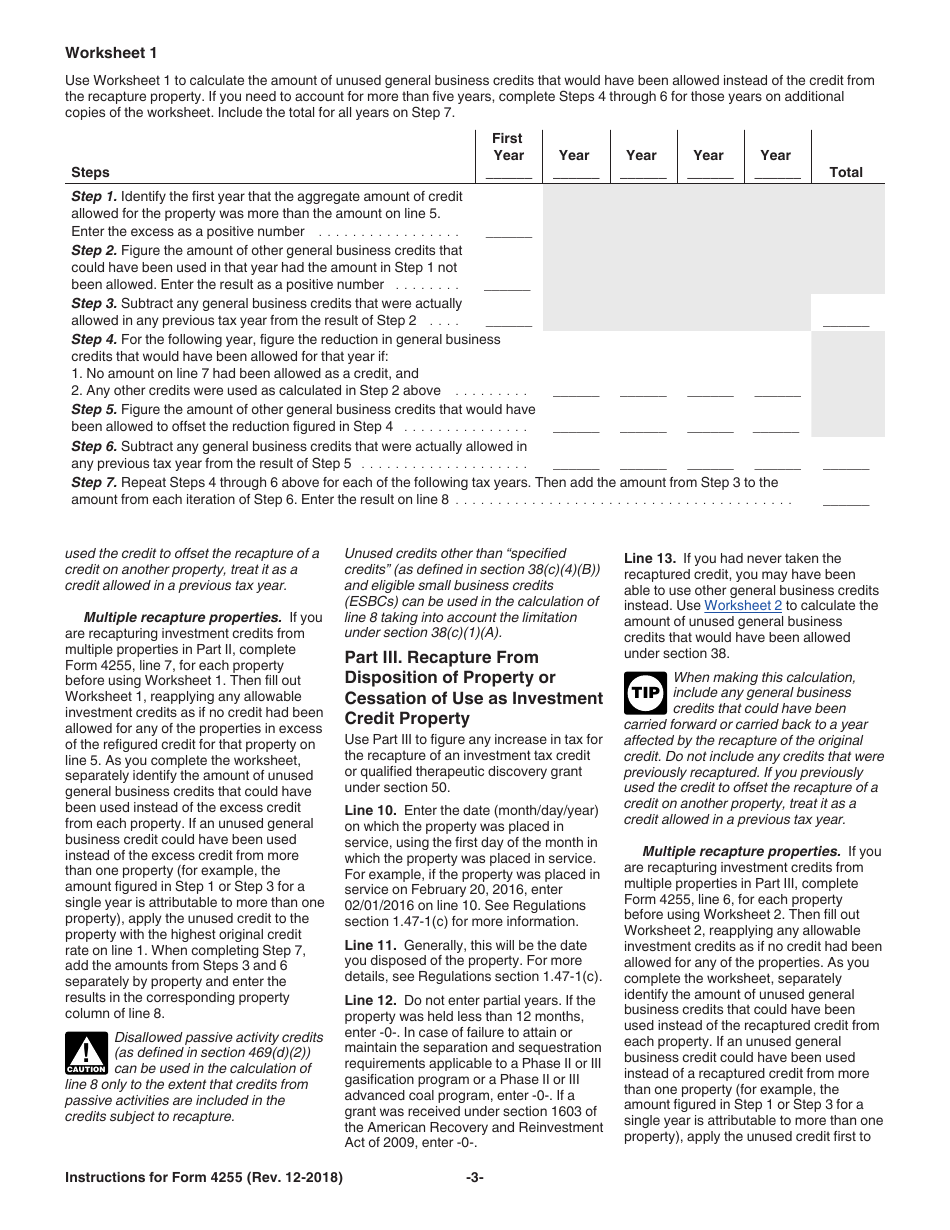

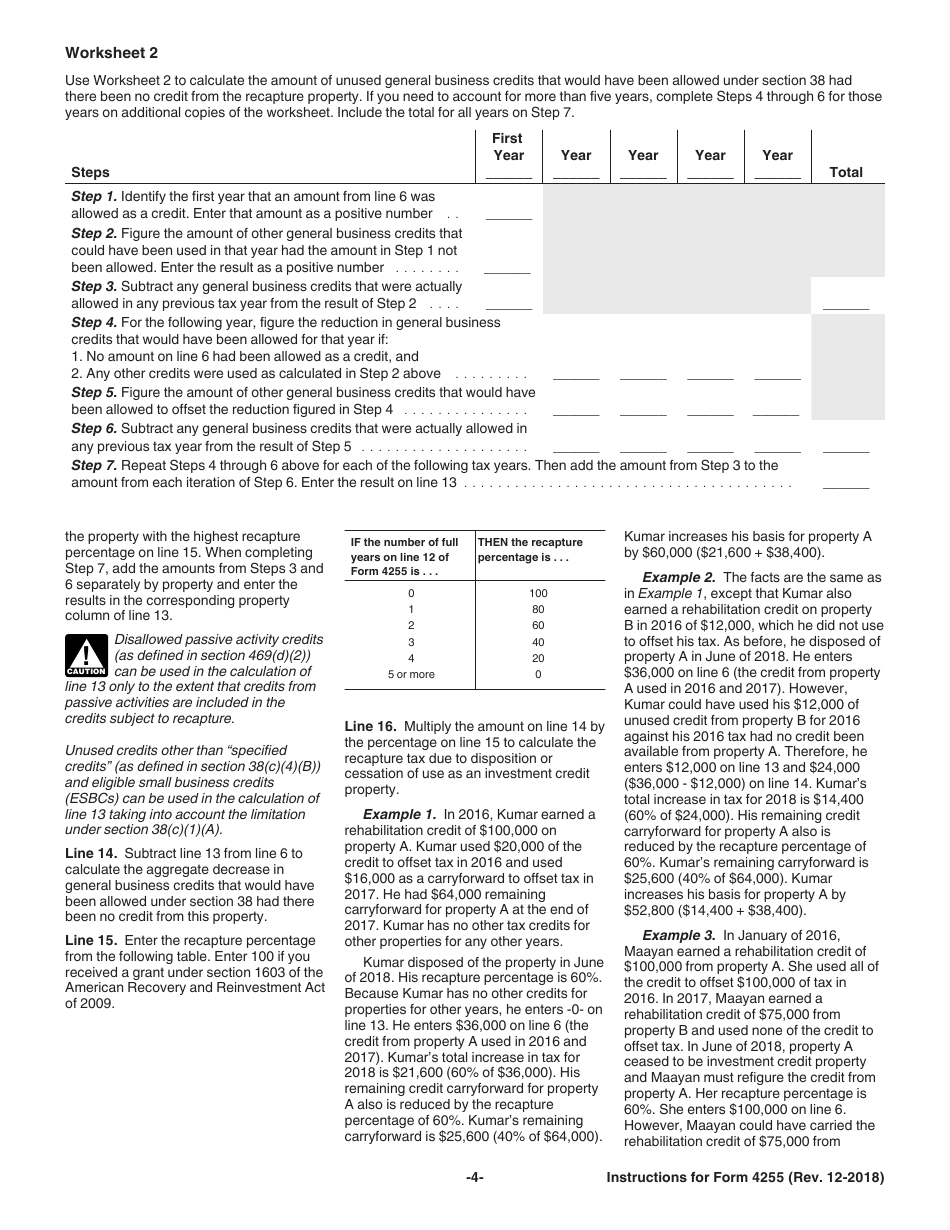

Instructions for IRS Form 4255 Recapture of Investment Credit

This document contains official instructions for IRS Form 4255 , Recapture of Investment Credit - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 4255 is available for download through this link.

FAQ

Q: What is IRS Form 4255?

A: IRS Form 4255 is a form used to recapture the investment credit.

Q: What is the purpose of Form 4255?

A: The purpose of Form 4255 is to calculate and recapture any investment credit previously claimed.

Q: Who needs to file Form 4255?

A: Individuals or businesses who have claimed an investment credit and need to recapture it must file Form 4255.

Q: What is an investment credit?

A: An investment credit is a tax benefit that allows individuals or businesses to deduct a portion of their qualified investment costs from their taxes.

Q: When should Form 4255 be filed?

A: Form 4255 should be filed in the tax year in which the recapture event occurs.

Q: What are some examples of recapture events?

A: Some examples of recapture events include the sale or disposition of the property, a change in use of the property, or a decrease in the qualified investment.

Q: Is there a deadline for filing Form 4255?

A: Yes, Form 4255 must be filed by the due date of the tax return for the tax year in which the recapture event occurs.

Q: Are there any penalties for not filing Form 4255?

A: Yes, failure to file Form 4255 when required may result in penalties and interest.

Q: Can I amend a previously filed Form 4255?

A: Yes, if you need to correct information on a previously filed Form 4255, you can file an amended form using Form 1040X.

Instruction Details:

- This 5-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5