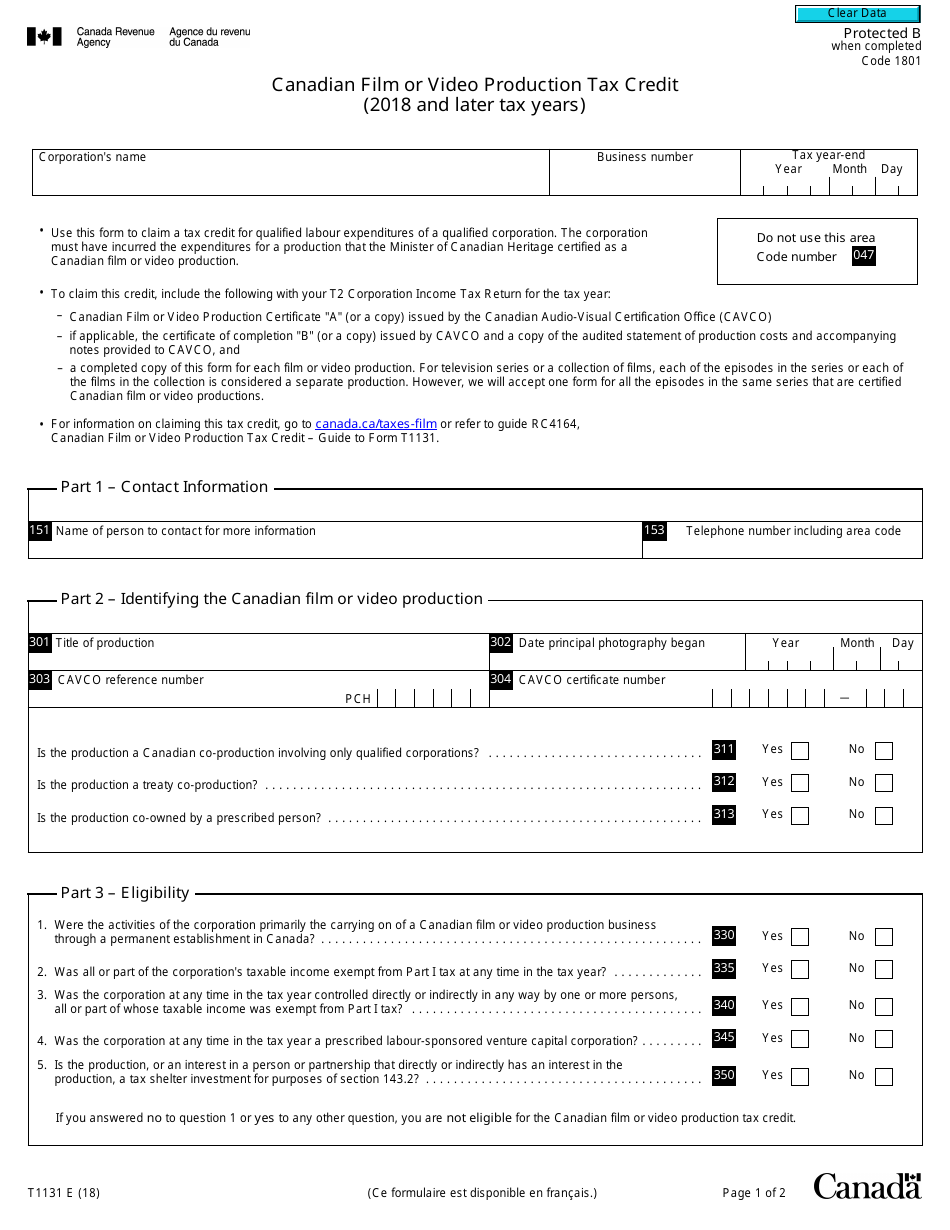

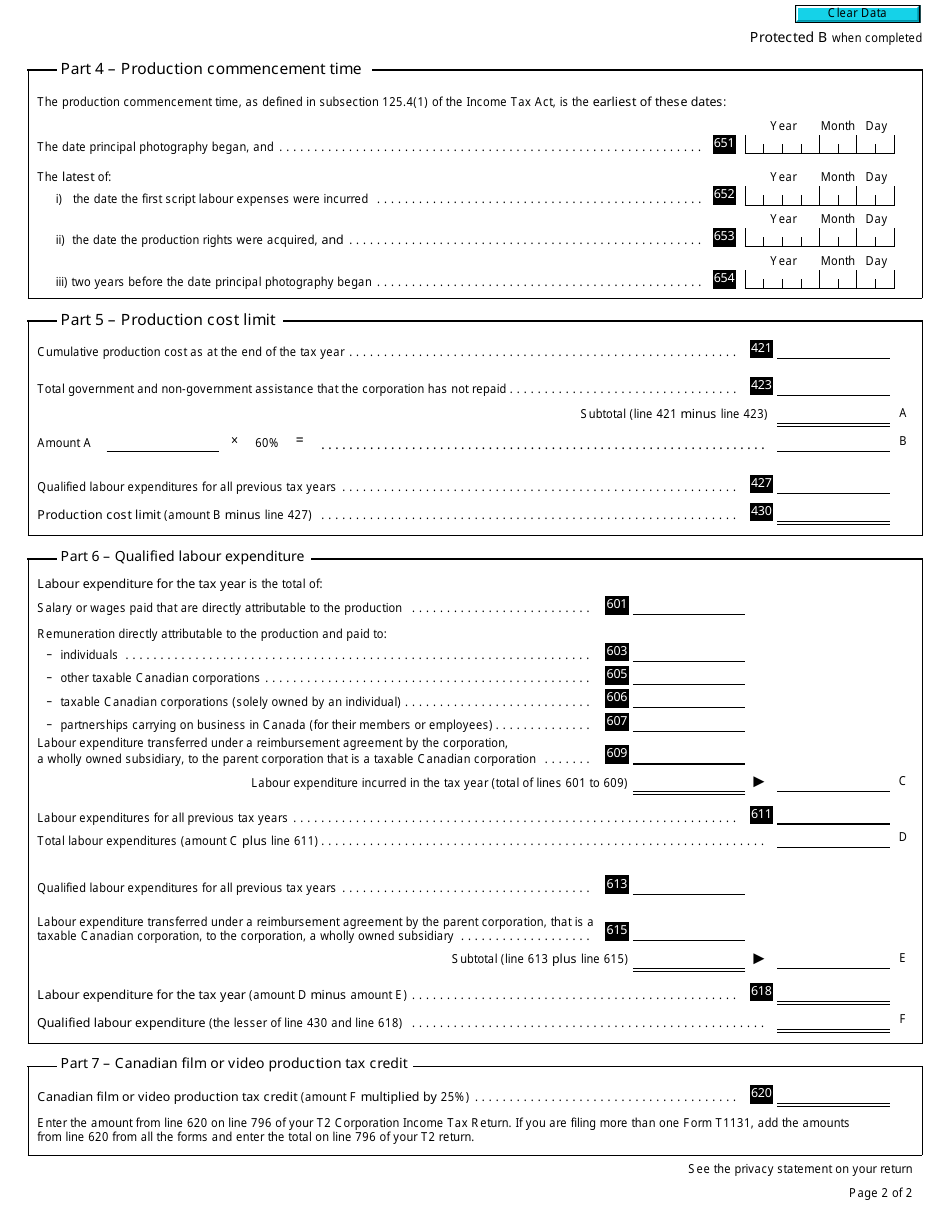

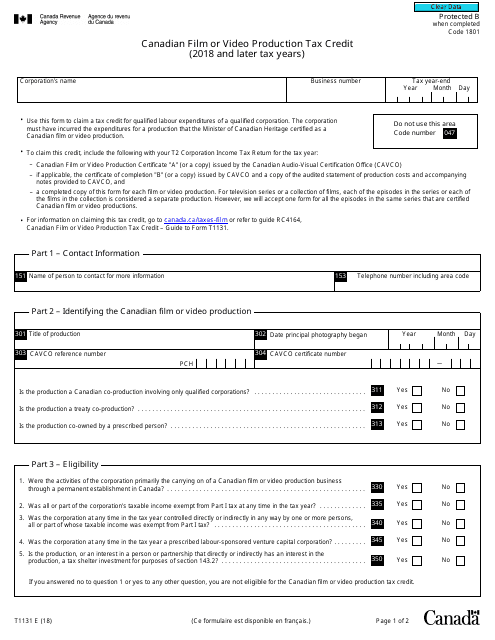

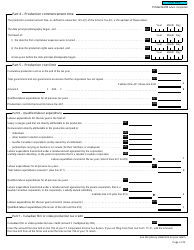

Form T1131 Canadian Film or Video Production Tax Credit (2018 and Later Tax Years) - Canada

Form T1131 is used for claiming the Canadian Film or Video Production Tax Credit. This tax credit is available for Canadian corporations that are engaged in the business of producing Canadian film or video productions. It provides tax incentives to support the Canadian film and television industry.

The Form T1131 for the Canadian Film or Video Production Tax Credit (2018 and later tax years) is filed by the film or video production company in Canada.

FAQ

Q: What is Form T1131?

A: Form T1131 is a tax form used in Canada to claim the Canadian Film or Video Production Tax Credit.

Q: What is the Canadian Film or Video Production Tax Credit?

A: The Canadian Film or Video Production Tax Credit is a tax credit provided by the Canadian government to support the production of Canadian films and videos.

Q: Who can claim the Canadian Film or Video Production Tax Credit?

A: Producers of Canadian films or videos can claim the Canadian Film or Video Production Tax Credit.

Q: What is the purpose of Form T1131?

A: Form T1131 is used to report and claim the Canadian Film or Video Production Tax Credit.

Q: When should Form T1131 be filed?

A: Form T1131 should be filed with the Canadian Revenue Agency when claiming the Canadian Film or Video Production Tax Credit.

Q: Is Form T1131 only applicable for the 2018 and later tax years?

A: Yes, Form T1131 is specific to the 2018 and later tax years.

Q: Are there any specific requirements for claiming the Canadian Film or Video Production Tax Credit?

A: Yes, there are specific eligibility criteria and requirements that must be met to claim the Canadian Film or Video Production Tax Credit.

Download Form T1131 Canadian Film or Video Production Tax Credit (2018 and Later Tax Years) - Canada

1

2