![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form GST524

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form GST524

for the current year.

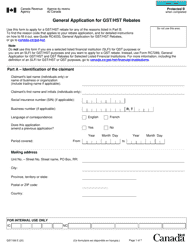

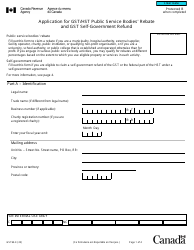

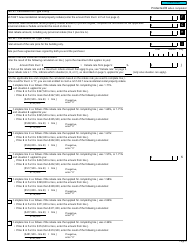

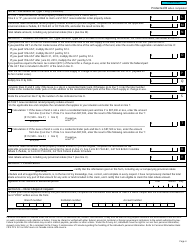

Form GST524 Gst / Hst New Residential Rental Property Rebate Application - Canada

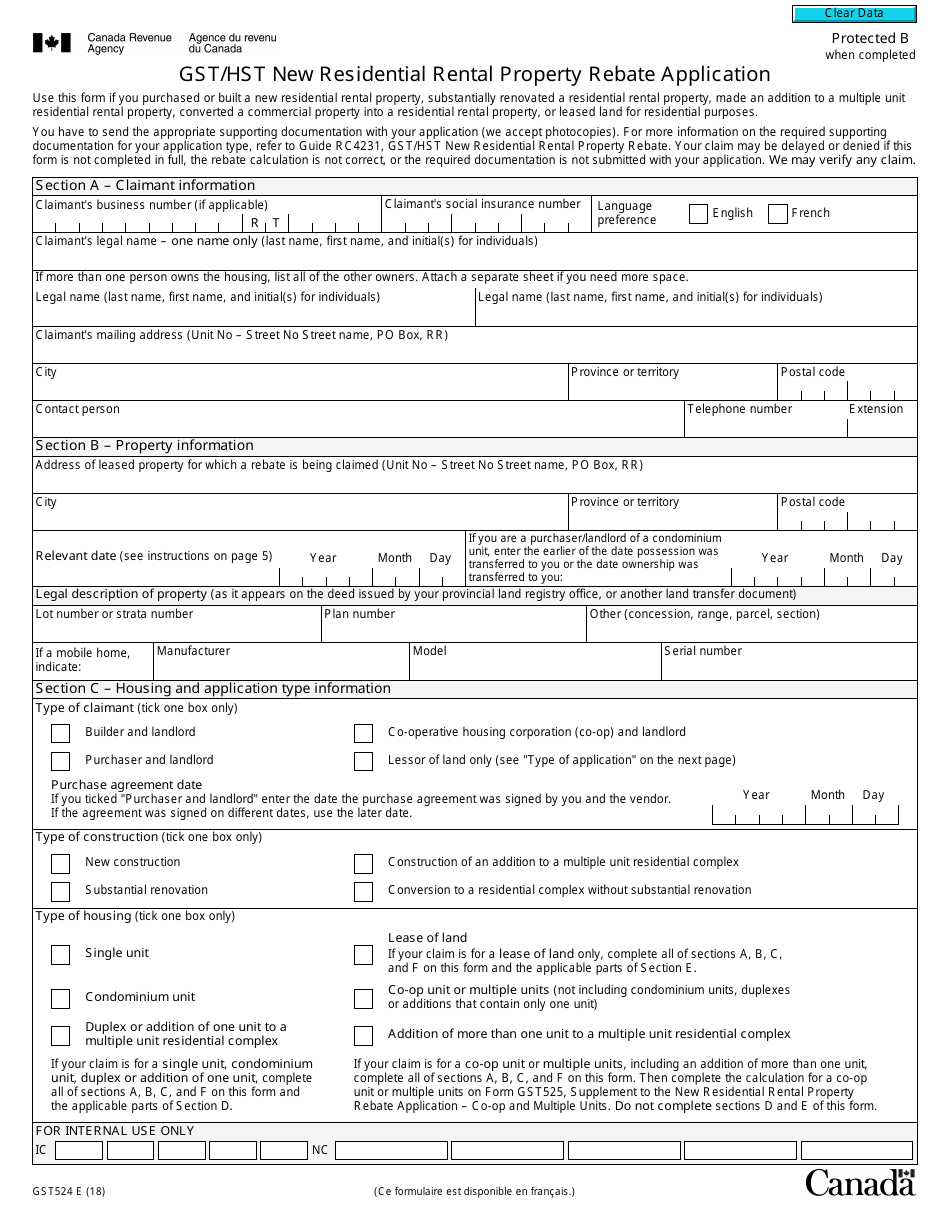

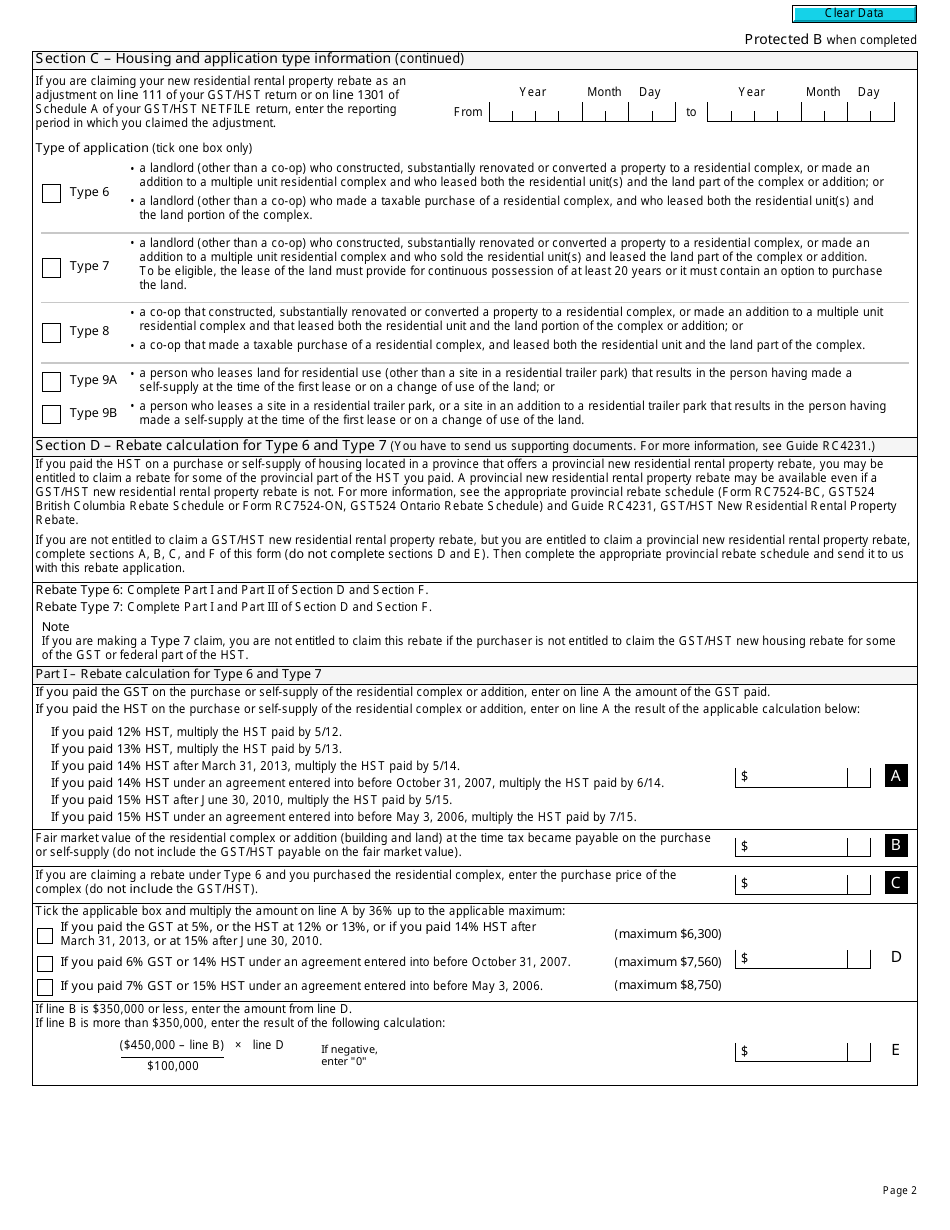

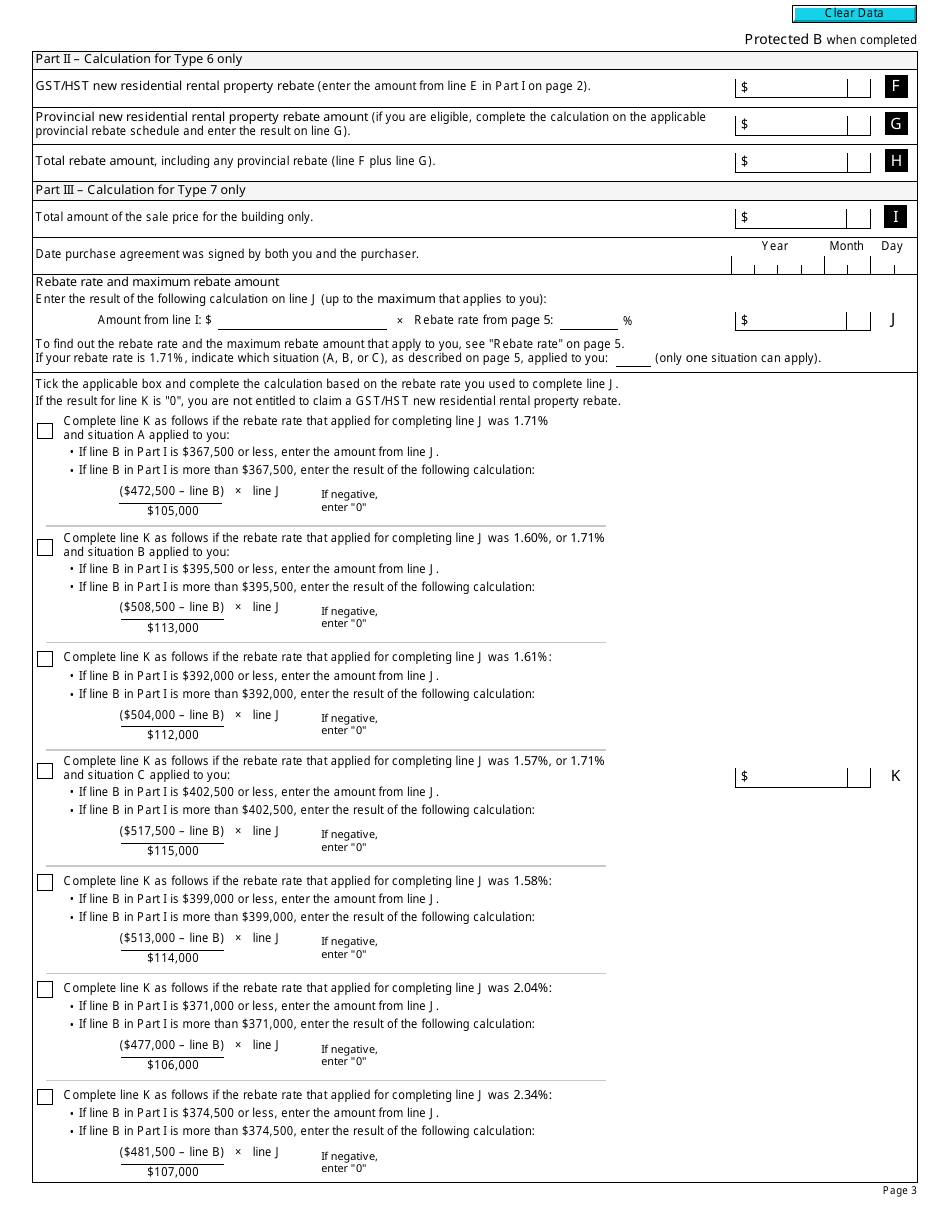

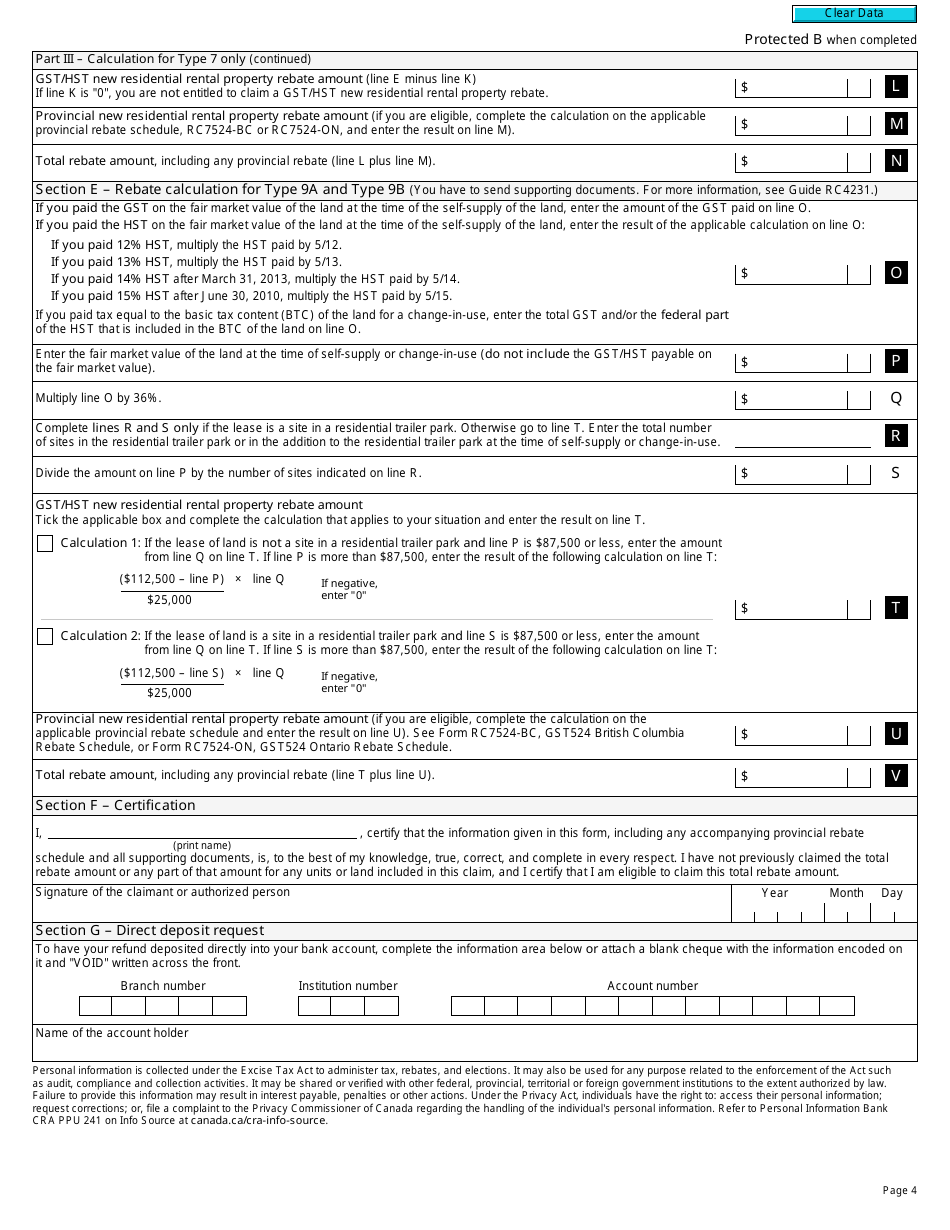

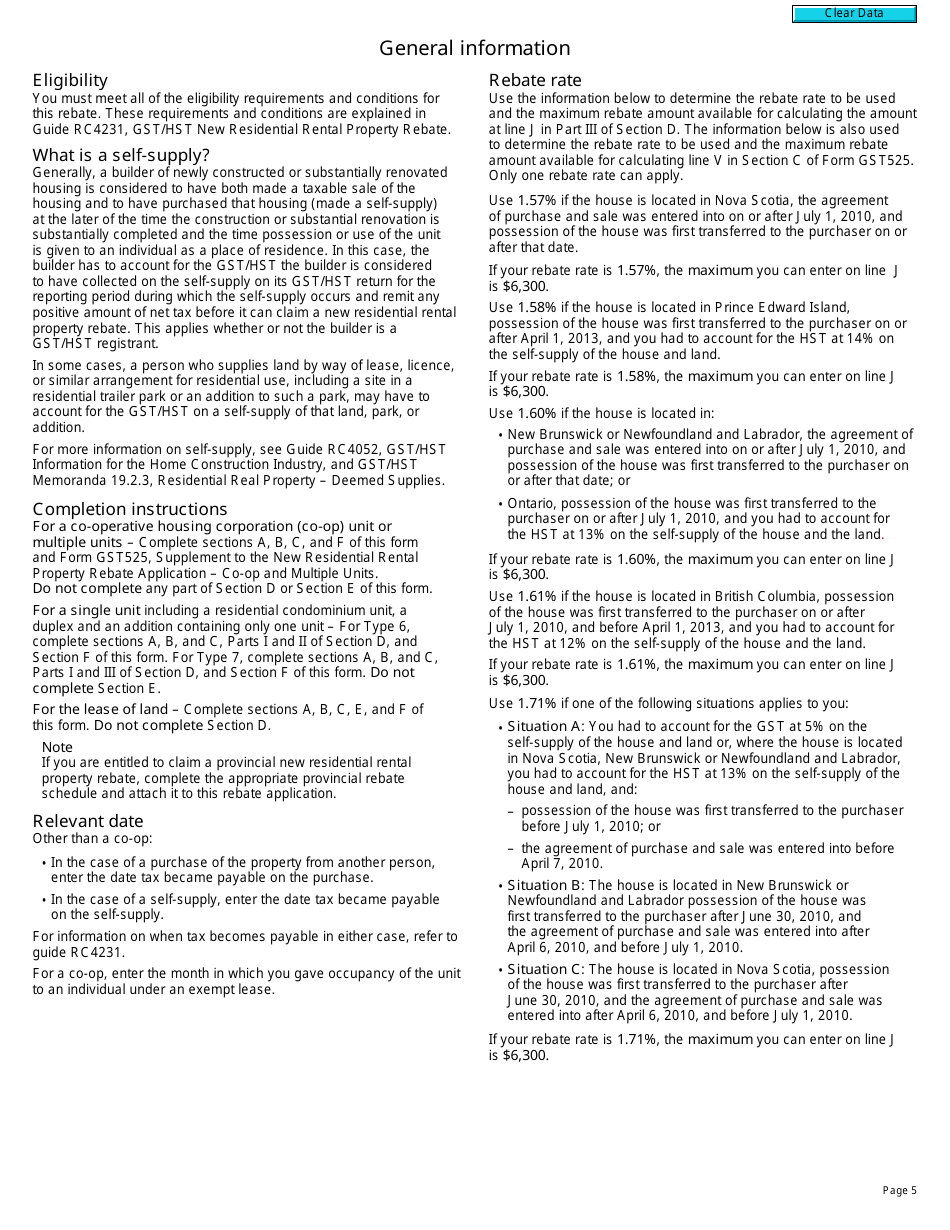

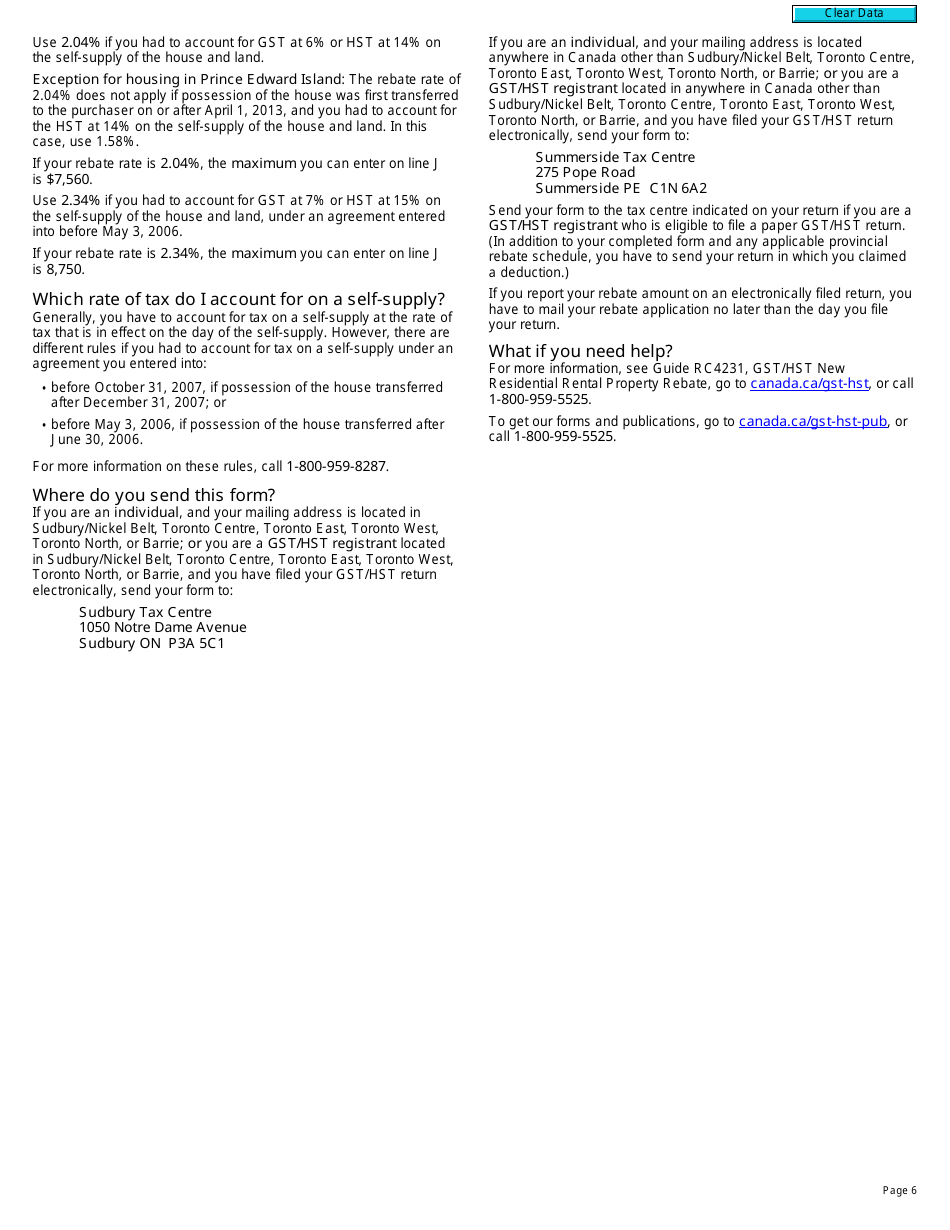

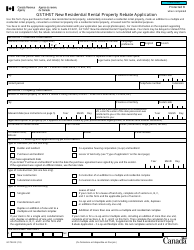

Form GST524 GST/HST New Residential Rental Property Rebate Application is used by landlords or property owners in Canada to apply for a rebate on the Goods and Services Tax (GST) or Harmonized Sales Tax (HST) paid on the purchase or construction of a new rental property. It is specifically for claiming the rebate on the GST/HST paid on the purchase or construction of a new residential rental property.

The Form GST524 GST/HST New Residential Rental Property Rebate Application is typically filed by the property owner or by their authorized representative.

FAQ

Q: What is Form GST524?

A: Form GST524 is the Gst/Hst New Residential Rental Property Rebate Application in Canada.

Q: What is the purpose of Form GST524?

A: Form GST524 is used to apply for the Gst/Hst New Residential Rental Property Rebate in Canada.

Q: Who can use Form GST524?

A: Form GST524 can be used by individuals or businesses who have recently purchased or built a new residential rental property in Canada and want to claim the GST/HST rebate.

Q: What information is required on Form GST524?

A: Form GST524 requires information such as the applicant's personal details, property information, and supporting documents to substantiate the claim.

Q: When should I submit Form GST524?

A: Form GST524 should be submitted within two years from the date the property was purchased or the construction was completed.

Q: Is there a fee to submit Form GST524?

A: No, there is no fee to submit Form GST524.

Q: What happens after I submit Form GST524?

A: After submitting Form GST524, the CRA will review the application and may request additional information if needed. If approved, the rebate will be processed and issued to the applicant.

Q: Can I claim the rebate if I am not a Canadian resident?

A: No, only Canadian residents are eligible to claim the Gst/Hst New Residential Rental Property Rebate.

Download Form GST524 Gst / Hst New Residential Rental Property Rebate Application - Canada

1

2

3

4

5

6