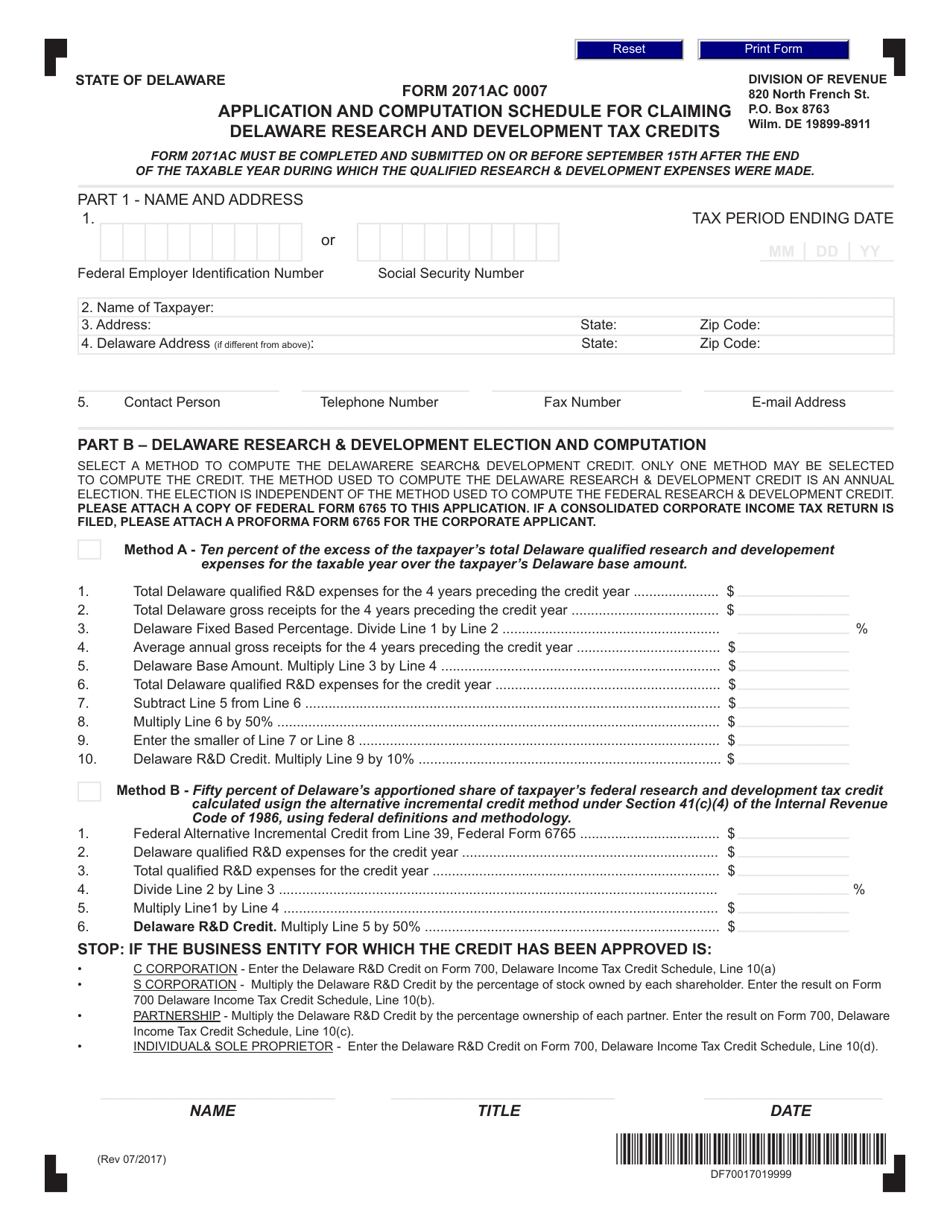

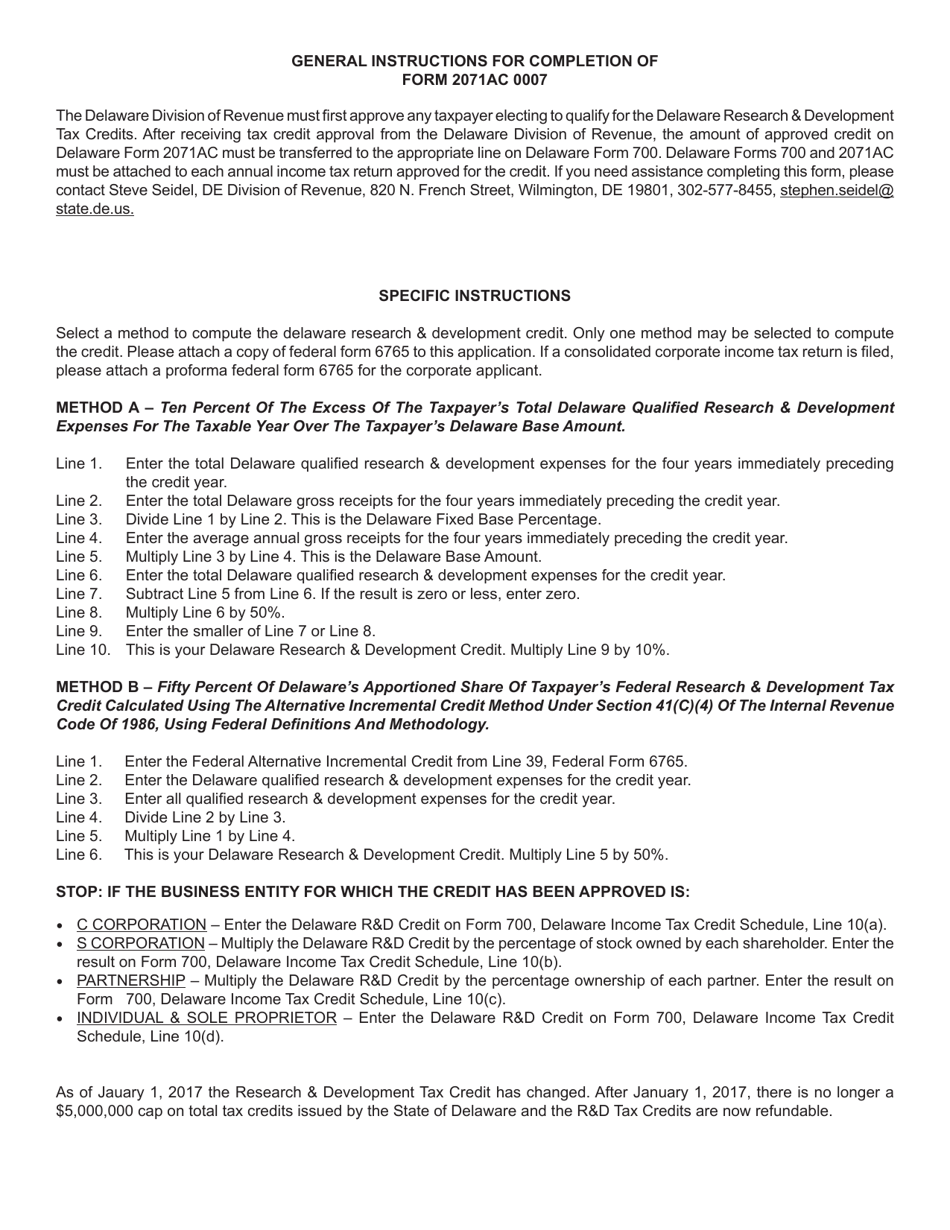

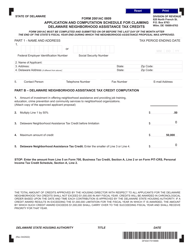

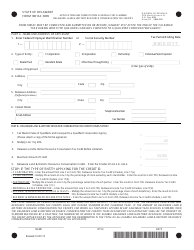

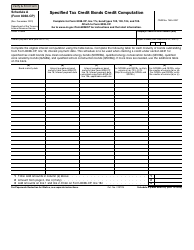

Form 2071AC 0007 Application and Computation Schedule for Claiming Delaware Research and Development Tax Credits - Delaware

What Is Form 2071AC 0007?

This is a legal form that was released by the Delaware Department of Finance - Division of Revenue - a government authority operating within Delaware. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 2071AC 0007?

A: Form 2071AC 0007 is an Application and Computation Schedule for Claiming Delaware Research and Development Tax Credits.

Q: What are Delaware Research and Development Tax Credits?

A: Delaware Research and Development Tax Credits are credits that businesses can claim for qualified research and development activities conducted in Delaware.

Q: Who can use Form 2071AC 0007?

A: Businesses that have conducted qualified research and development activities in Delaware can use Form 2071AC 0007 to apply for and compute their tax credits.

Q: What information is required on Form 2071AC 0007?

A: Form 2071AC 0007 requires information about the business, the research and development activities conducted, and the computation of the tax credits.

Q: Are there any deadlines for filing Form 2071AC 0007?

A: Yes, the deadlines for filing Form 2071AC 0007 vary each year and are specified by the Delaware Division of Revenue. It is important to file the form by the designated deadline to claim the tax credits.

Q: Can I claim Delaware Research and Development Tax Credits if I am not based in Delaware?

A: No, Delaware Research and Development Tax Credits are specific to businesses that have conducted qualified research and development activities in Delaware.

Q: What should I do if I need help with Form 2071AC 0007?

A: If you need assistance with Form 2071AC 0007, you can contact the Delaware Division of Revenue or consult a tax professional.

Q: Can I claim Delaware Research and Development Tax Credits for previous years?

A: Yes, you can typically claim Delaware Research and Development Tax Credits for previous years. However, specific rules and limitations may apply, so it is advisable to consult the Delaware Division of Revenue or a tax professional for guidance.

Form Details:

- Released on August 1, 2017;

- The latest edition provided by the Delaware Department of Finance - Division of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 2071AC 0007 by clicking the link below or browse more documents and templates provided by the Delaware Department of Finance - Division of Revenue.

Download Form 2071AC 0007 Application and Computation Schedule for Claiming Delaware Research and Development Tax Credits - Delaware

1

2