![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 765

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 765

for the current year.

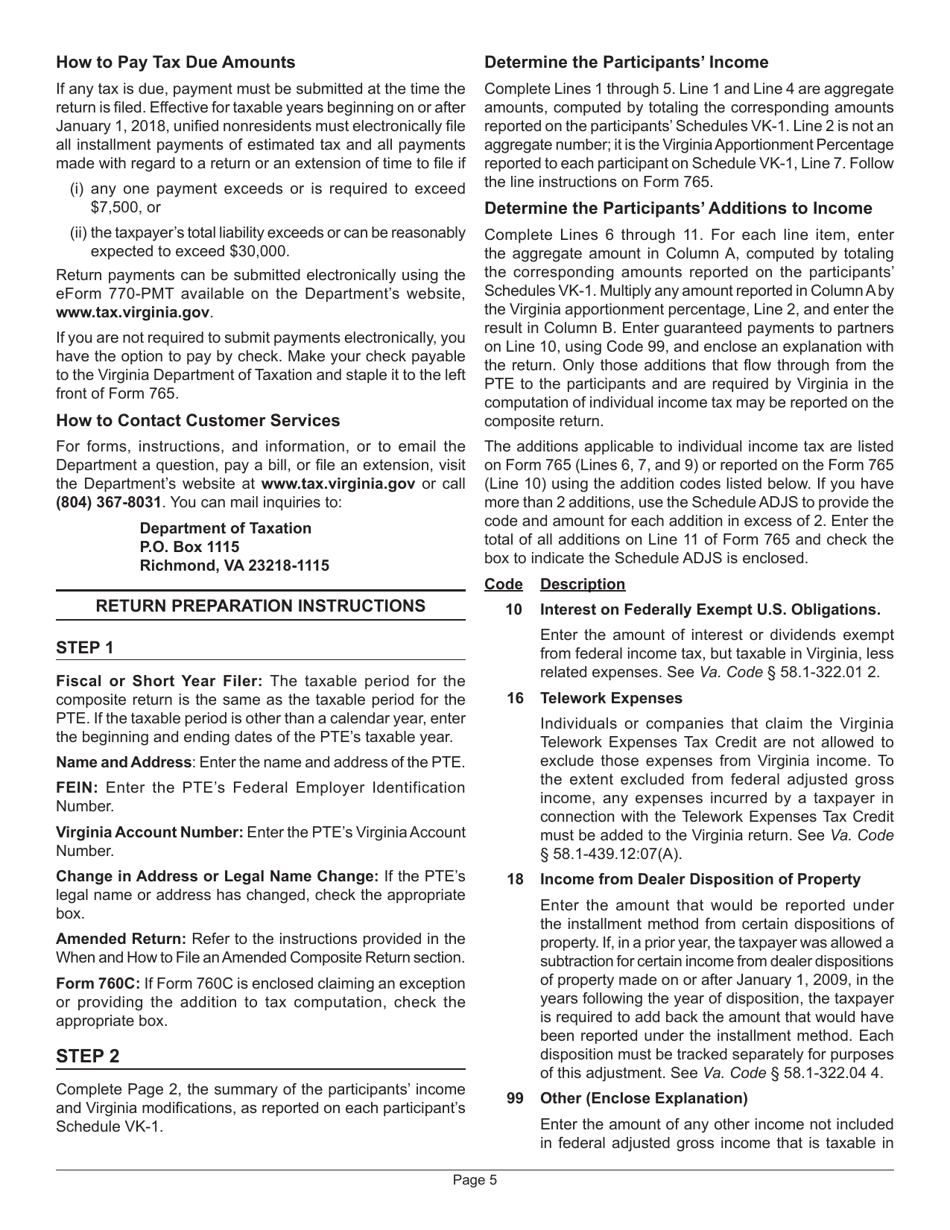

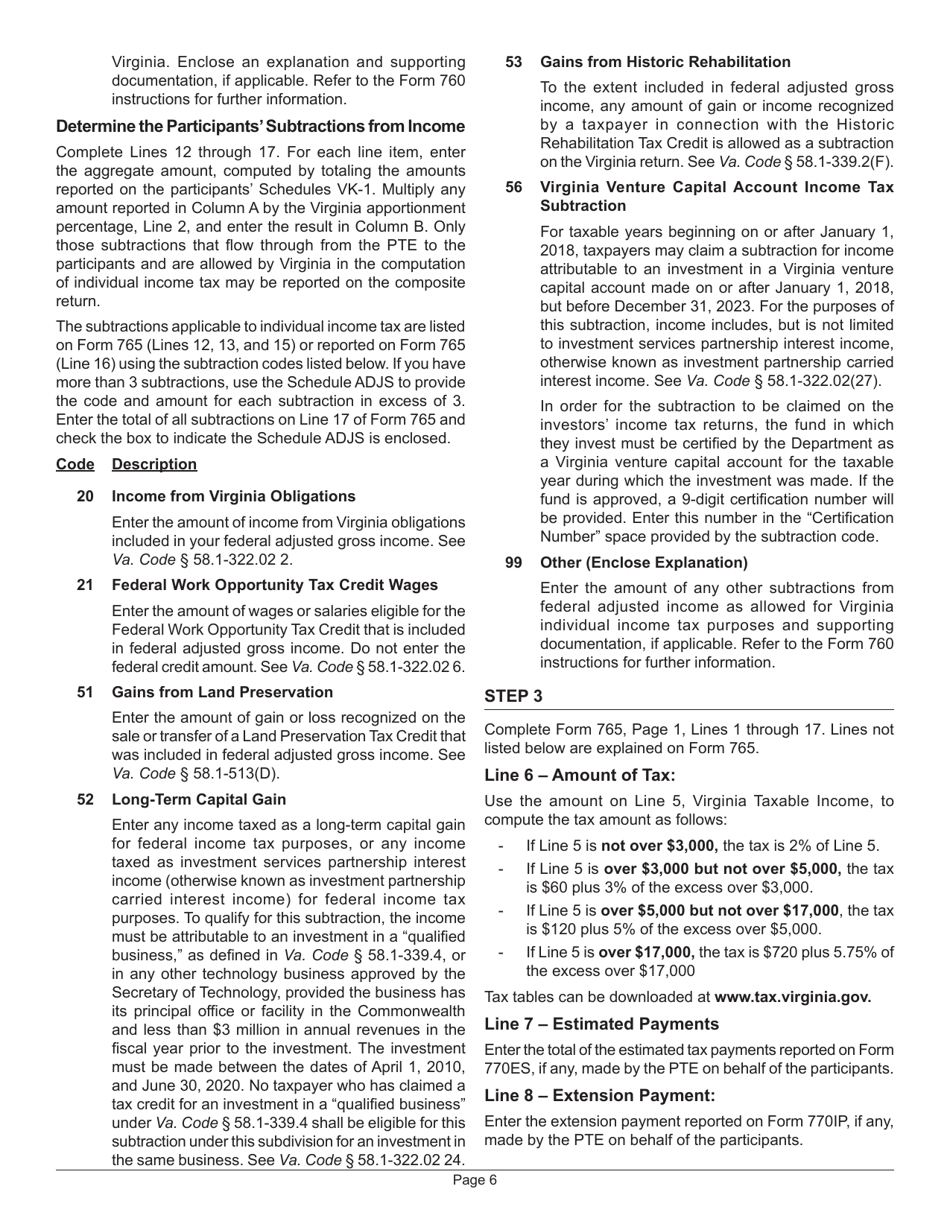

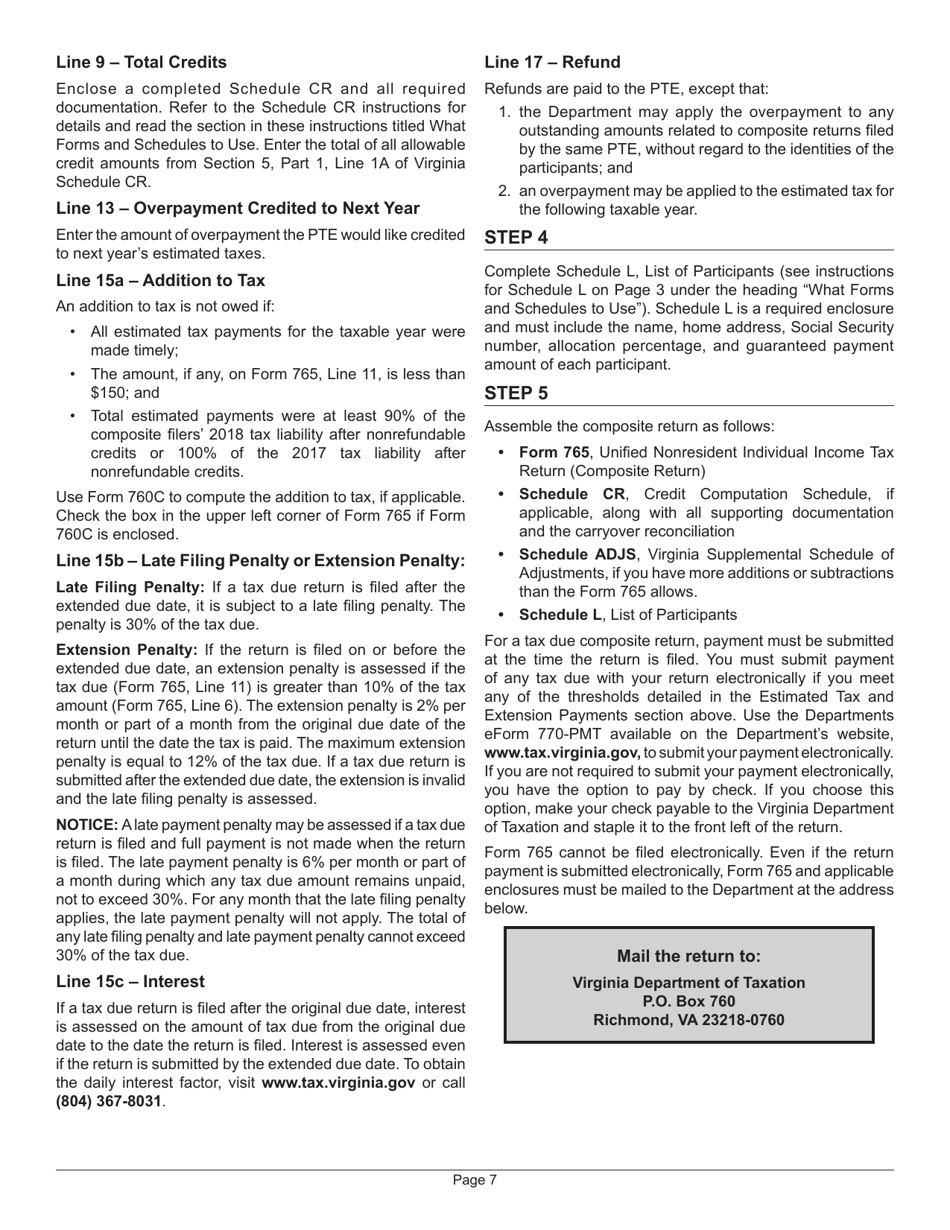

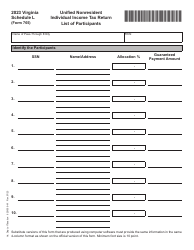

Instructions for Form 765 Unified Nonresident Individual Income Tax Return (Composite Return) - Virginia

This document contains official instructions for Form 765 , Unified Nonresident Individual Income Tax Return (Composite Return) - a form released and collected by the Virginia Department of Taxation. An up-to-date fillable Form 765 is available for download through this link.

FAQ

Q: What is Form 765?

A: Form 765 is the Unified Nonresident Individual Income Tax Return (Composite Return) for the state of Virginia.

Q: Who needs to file Form 765?

A: Nonresident individuals who derive income from Virginia sources and choose to file a composite return on behalf of certain qualifying nonresident owners or beneficiaries.

Q: What is a composite return?

A: A composite return is a single tax return filed on behalf of multiple nonresident owners or beneficiaries of a pass-through entity.

Q: What information do I need to complete Form 765?

A: You will need information about your income from Virginia sources, as well as information about the nonresident owners or beneficiaries for whom you are filing the composite return.

Q: When is the deadline to file Form 765?

A: The deadline to file Form 765 is the same as the due date for individual income tax returns in Virginia, which is typically May 1st.

Q: Are there any penalties for late filing or noncompliance?

A: Yes, there may be penalties for late filing or noncompliance. It is important to file your return and pay any taxes owed by the deadline to avoid penalties.

Q: Can I get an extension to file Form 765?

A: Yes, you can request an extension to file Form 765. The extension must be requested by the original due date of the return and gives you an additional six months to file.

Instruction Details:

- This 7-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Virginia Department of Taxation.

Download Instructions for Form 765 Unified Nonresident Individual Income Tax Return (Composite Return) - Virginia

1

2

3

4

5

6

7