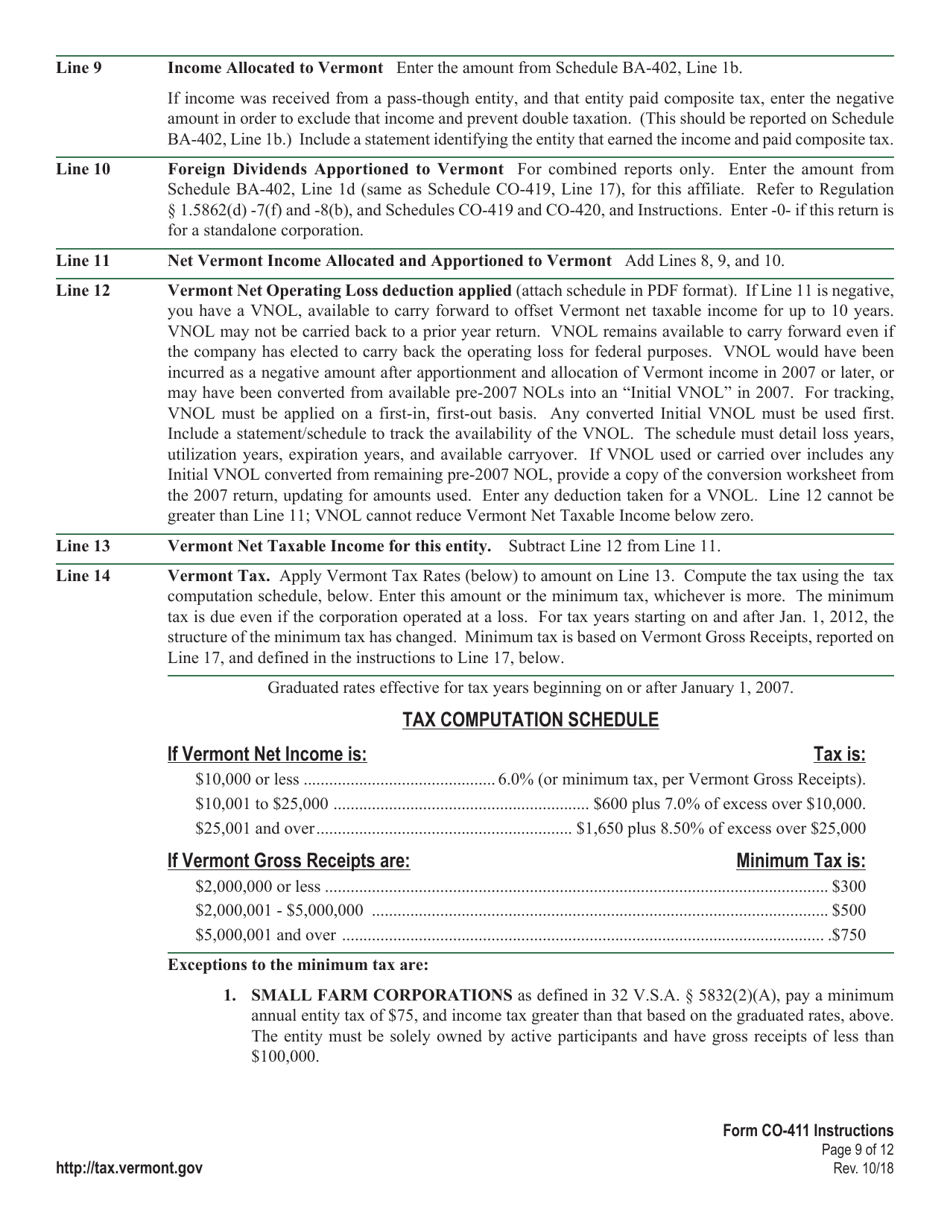

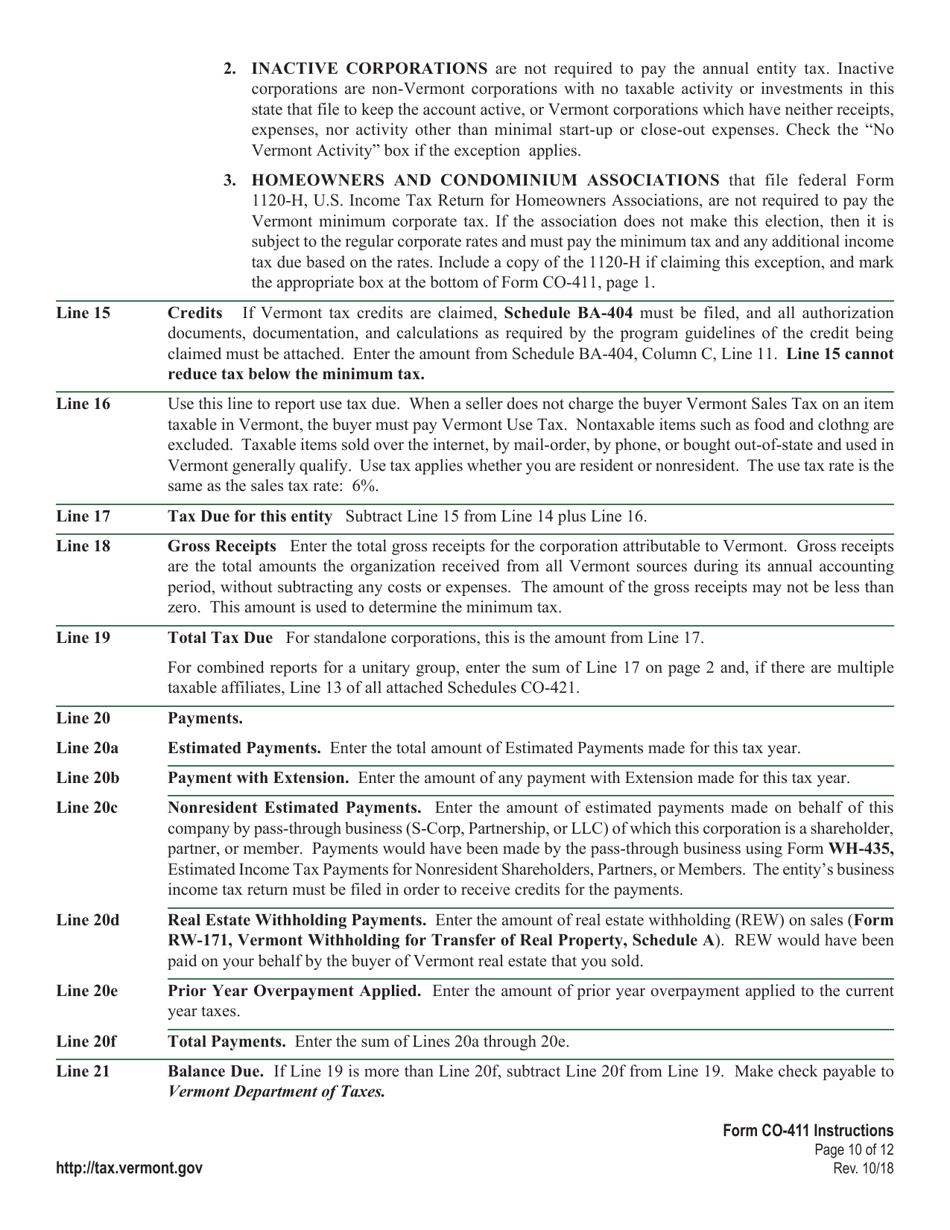

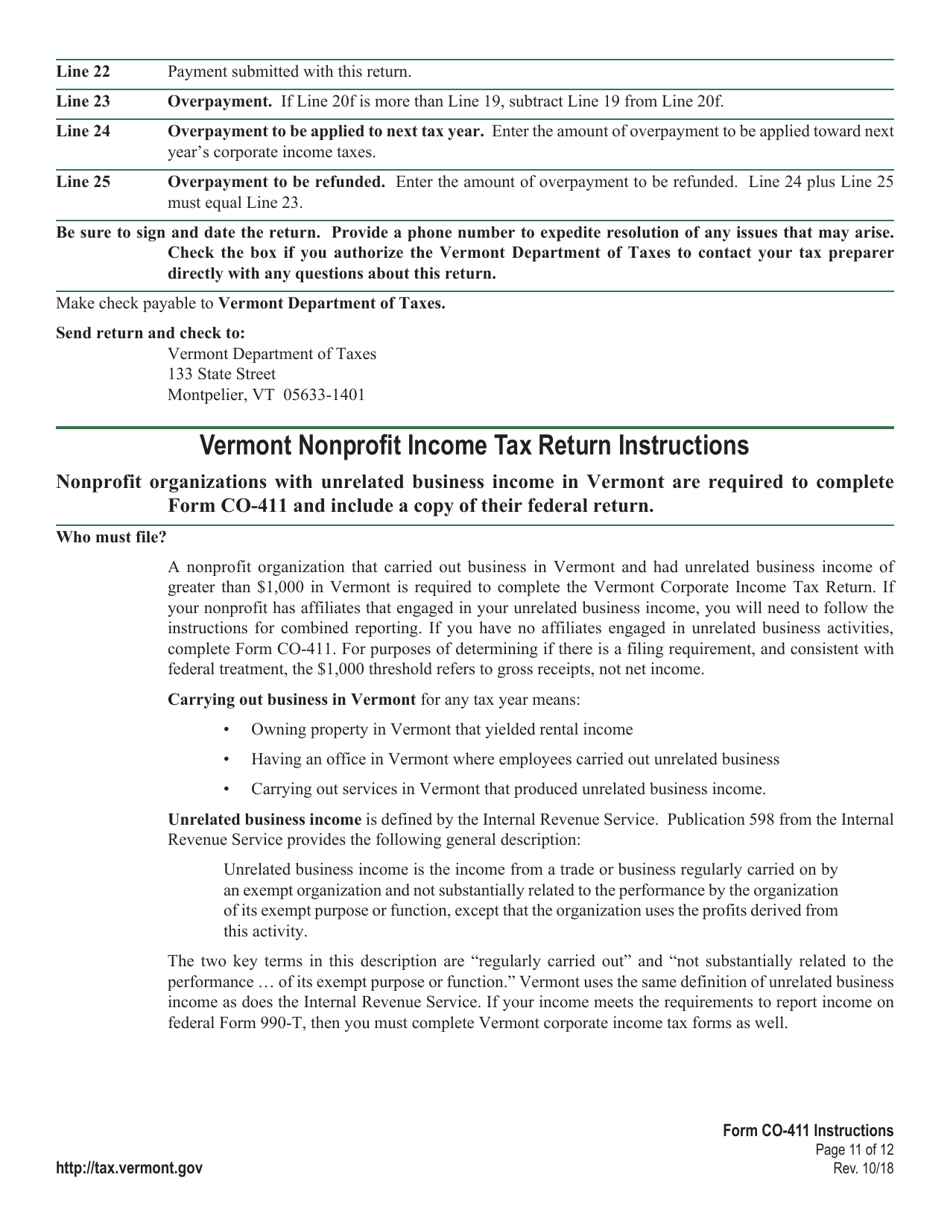

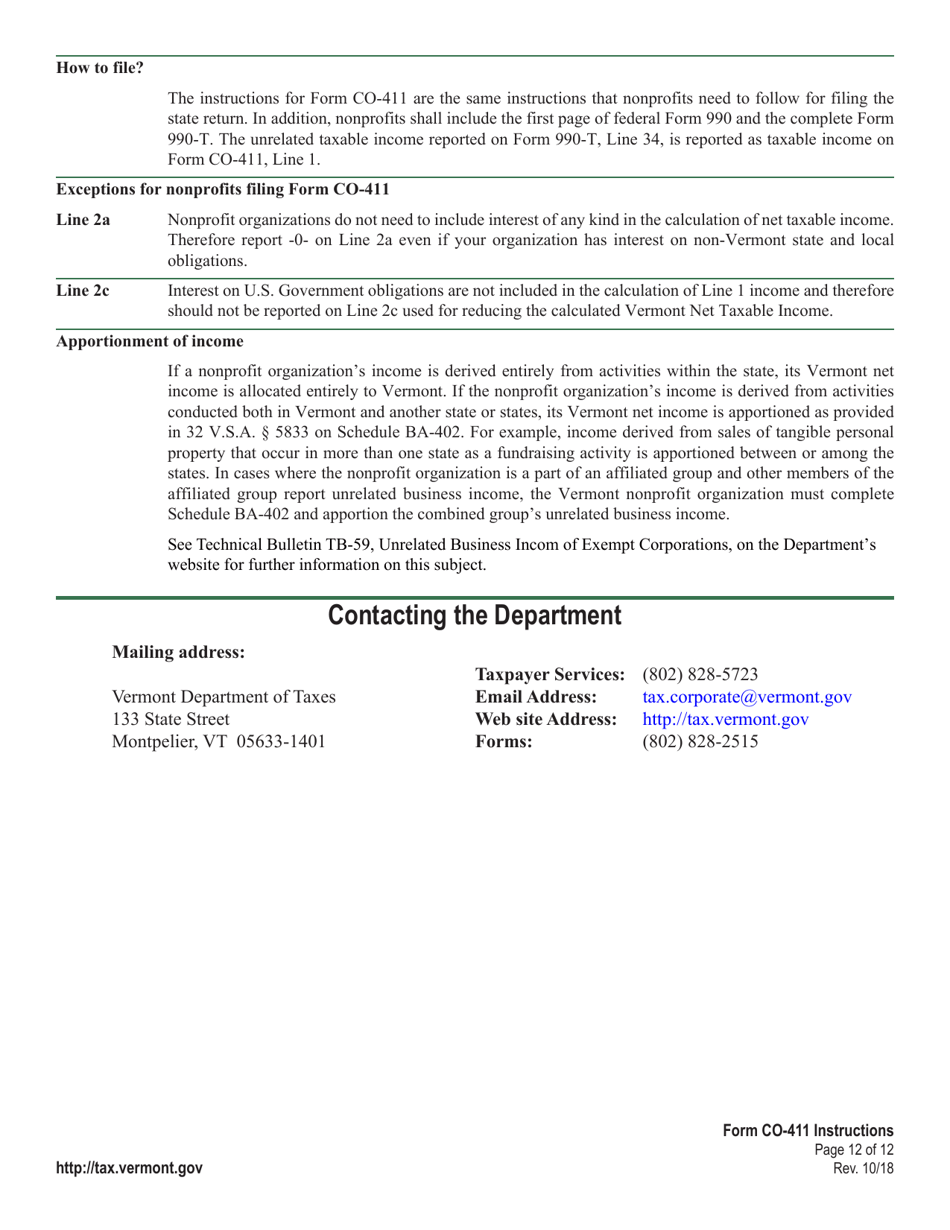

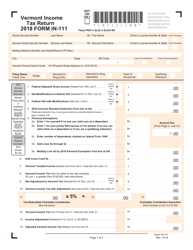

Instructions for VT Form CO-411 Corporate Income Tax Return - Vermont

This document contains official instructions for VT Form CO-411 , Corporate Income Tax Return - a form released and collected by the Vermont Department of Taxes. An up-to-date fillable VT Form CO-411 is available for download through this link.

FAQ

Q: What is the VT Form CO-411?

A: The VT Form CO-411 is the Corporate Income Tax Return for the state of Vermont.

Q: Who needs to file the VT Form CO-411?

A: All corporations doing business in Vermont, including domestic and foreign corporations, need to file the VT Form CO-411.

Q: What information is required on the VT Form CO-411?

A: The form requires information about the corporation's income, deductions, credits, and apportionment factors.

Q: When is the due date for filing the VT Form CO-411?

A: The due date for filing the VT Form CO-411 is the 15th day of the third month following the close of the tax year.

Q: Is there an extension available for filing the VT Form CO-411?

A: Yes, corporations can request an extension to file the VT Form CO-411, but any tax owed must be paid by the original due date.

Q: Are there any penalties for late filing of the VT Form CO-411?

A: Yes, late filing of the VT Form CO-411 may result in penalties and interest.

Q: Are there any other forms or schedules that need to be attached to the VT Form CO-411?

A: Depending on the corporation's specific circumstances, additional forms or schedules may need to be attached to the VT Form CO-411.

Instruction Details:

- This 12-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Vermont Department of Taxes.

1

2

3

4

5

6

7

8

9

10

11

12