![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form LPC-1 Schedule A

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form LPC-1 Schedule A

for the current year.

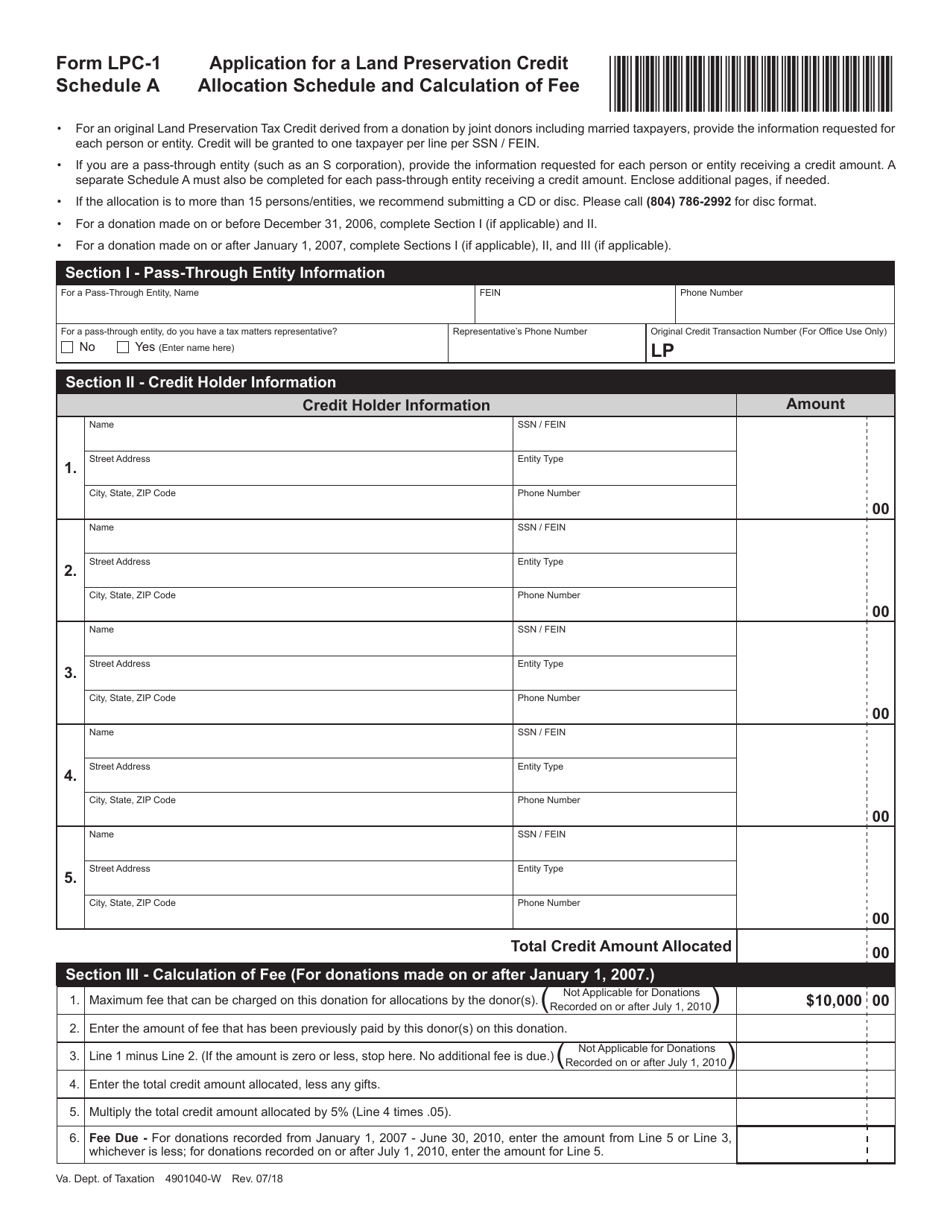

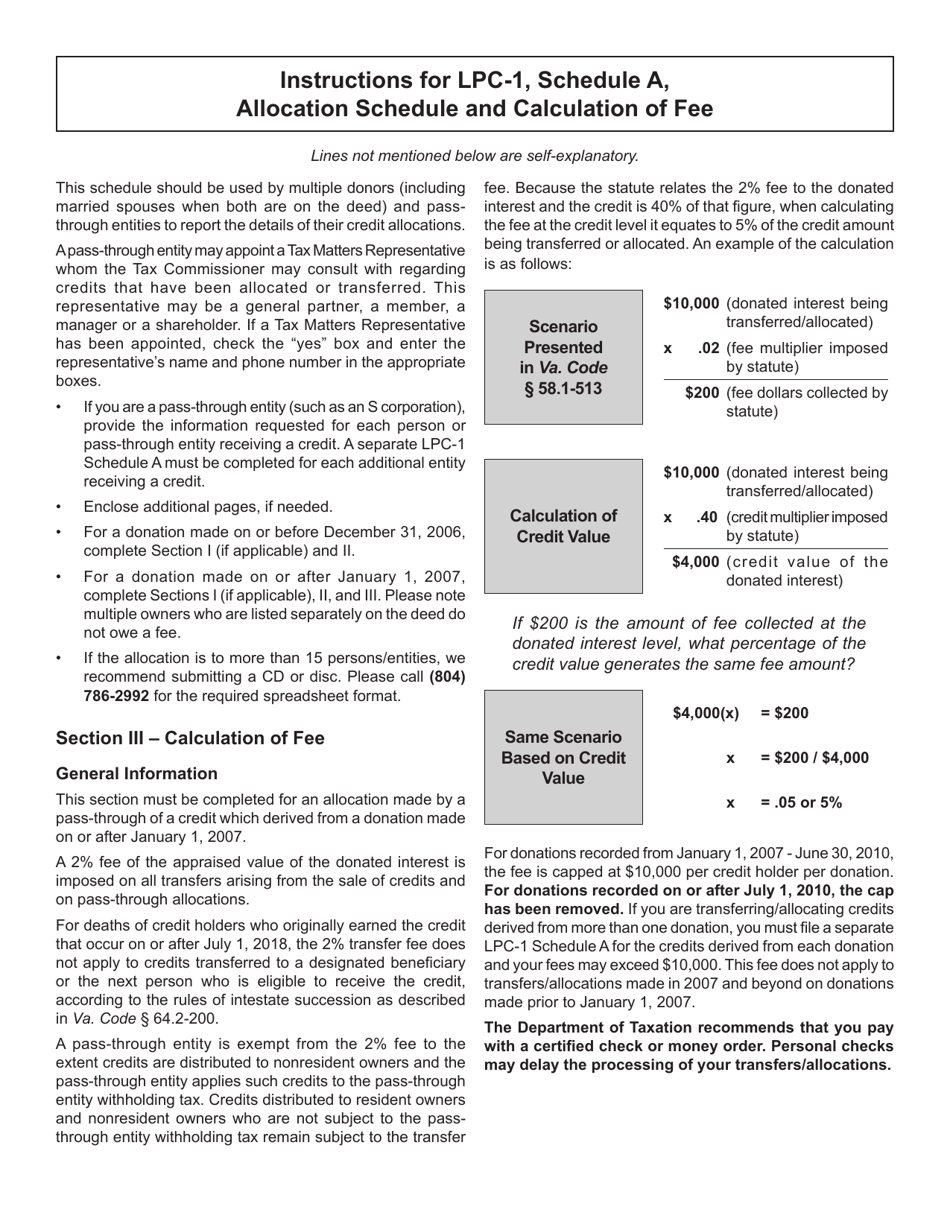

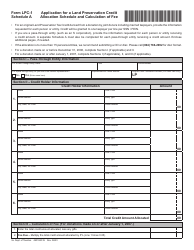

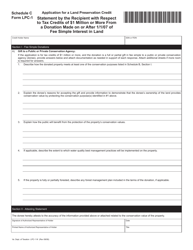

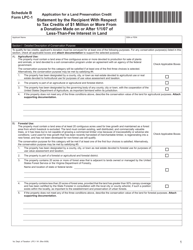

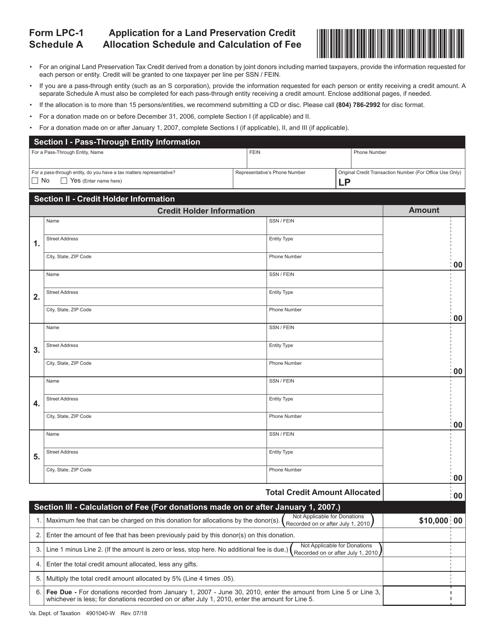

Form LPC-1 Schedule A Land Preservation Credit - Allocation Schedule and Calculation of Fee - Virginia

What Is Form LPC-1 Schedule A?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia.The document is a supplement to Form LPC-1, Application for a Land Preservation Credit. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form LPC-1 Schedule A?

A: Form LPC-1 Schedule A is a document used to report the allocation of Land Preservation Credits and calculate the associated fee in Virginia.

Q: What is the purpose of Form LPC-1 Schedule A?

A: The purpose of Form LPC-1 Schedule A is to provide detailed information on the allocation of Land Preservation Credits and calculate the fee required in Virginia.

Q: Who should use Form LPC-1 Schedule A?

A: Form LPC-1 Schedule A should be used by individuals or entities who are participating in Virginia's Land Preservation Credit program and need to report credit allocations and calculate fees.

Q: What information is required on Form LPC-1 Schedule A?

A: Form LPC-1 Schedule A requires information about the land preservation credit allocations, the fee calculation based on those allocations, and the contact information of the individual or entity submitting the form.

Q: Is there a fee for filing Form LPC-1 Schedule A?

A: Yes, there is a fee associated with filing Form LPC-1 Schedule A. The fee is calculated based on the total amount of land preservation credits being allocated.

Q: When is Form LPC-1 Schedule A due?

A: The due date for Form LPC-1 Schedule A may vary. It is important to check with the Virginia Department of Taxation or refer to the instructions provided with the form for the specific due date.

Q: What should I do if I need assistance with Form LPC-1 Schedule A?

A: If you need assistance with Form LPC-1 Schedule A, you can contact the Virginia Department of Taxation directly or consult a tax professional for guidance.

Form Details:

- Released on July 1, 2018;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form LPC-1 Schedule A by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.

Download Form LPC-1 Schedule A Land Preservation Credit - Allocation Schedule and Calculation of Fee - Virginia

1

2