![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form QBA

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form QBA

for the current year.

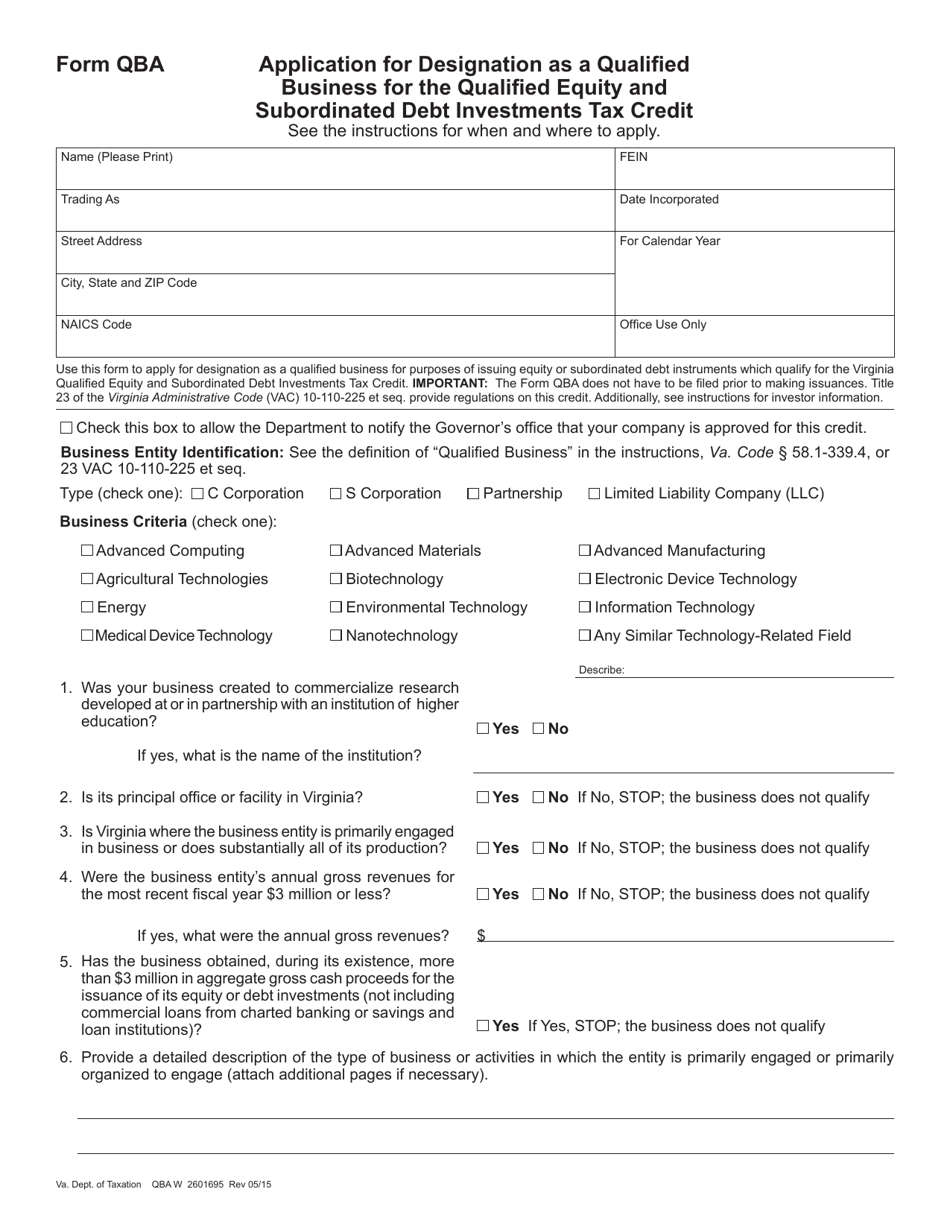

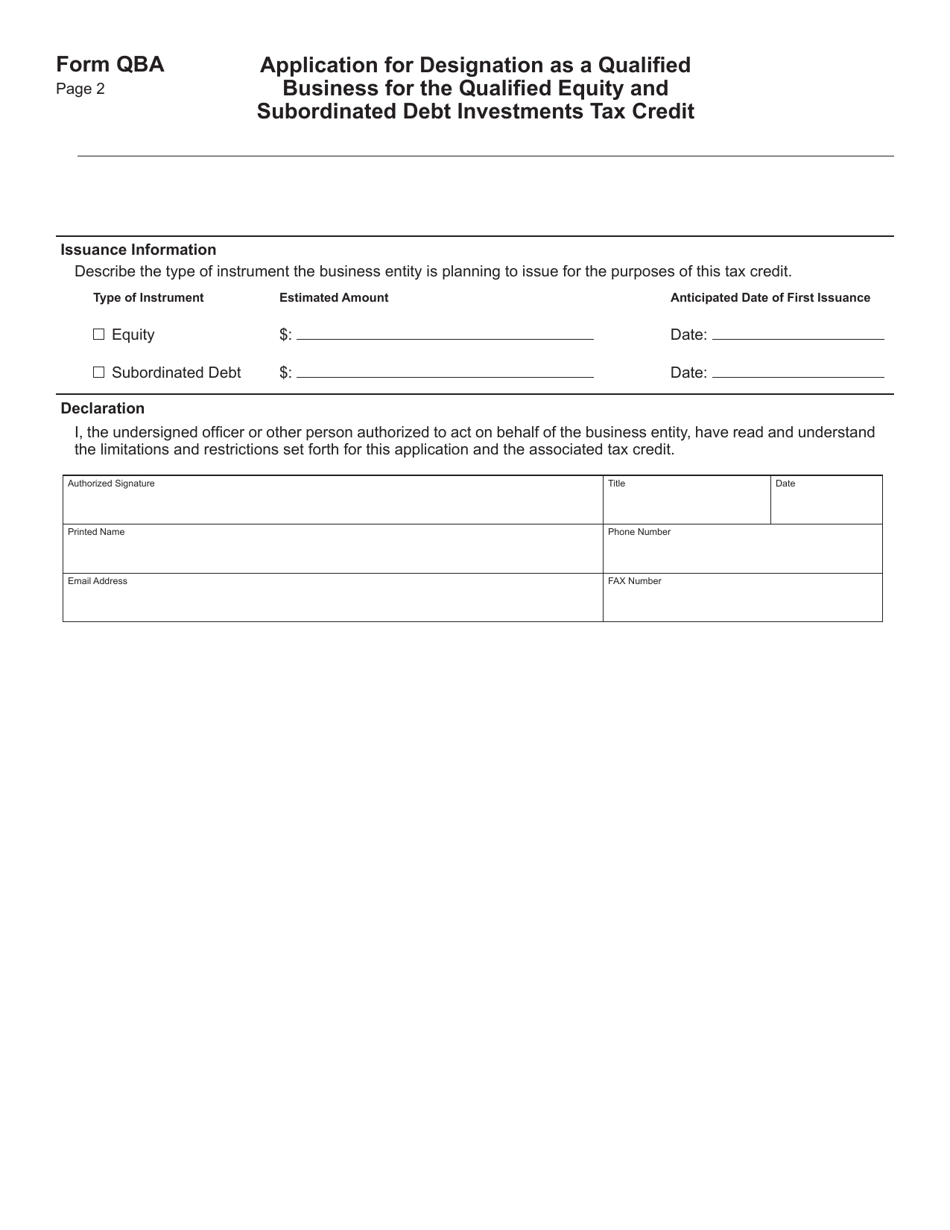

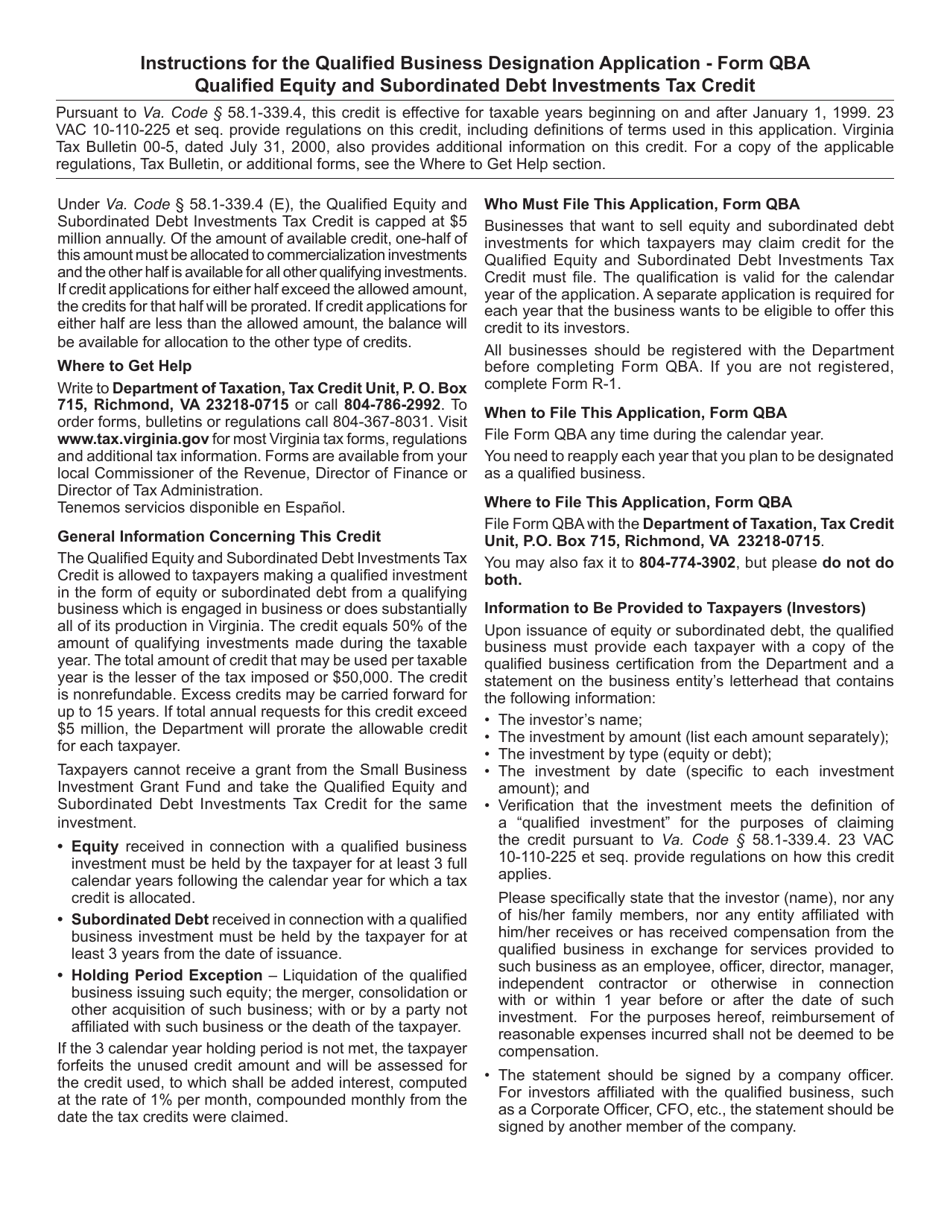

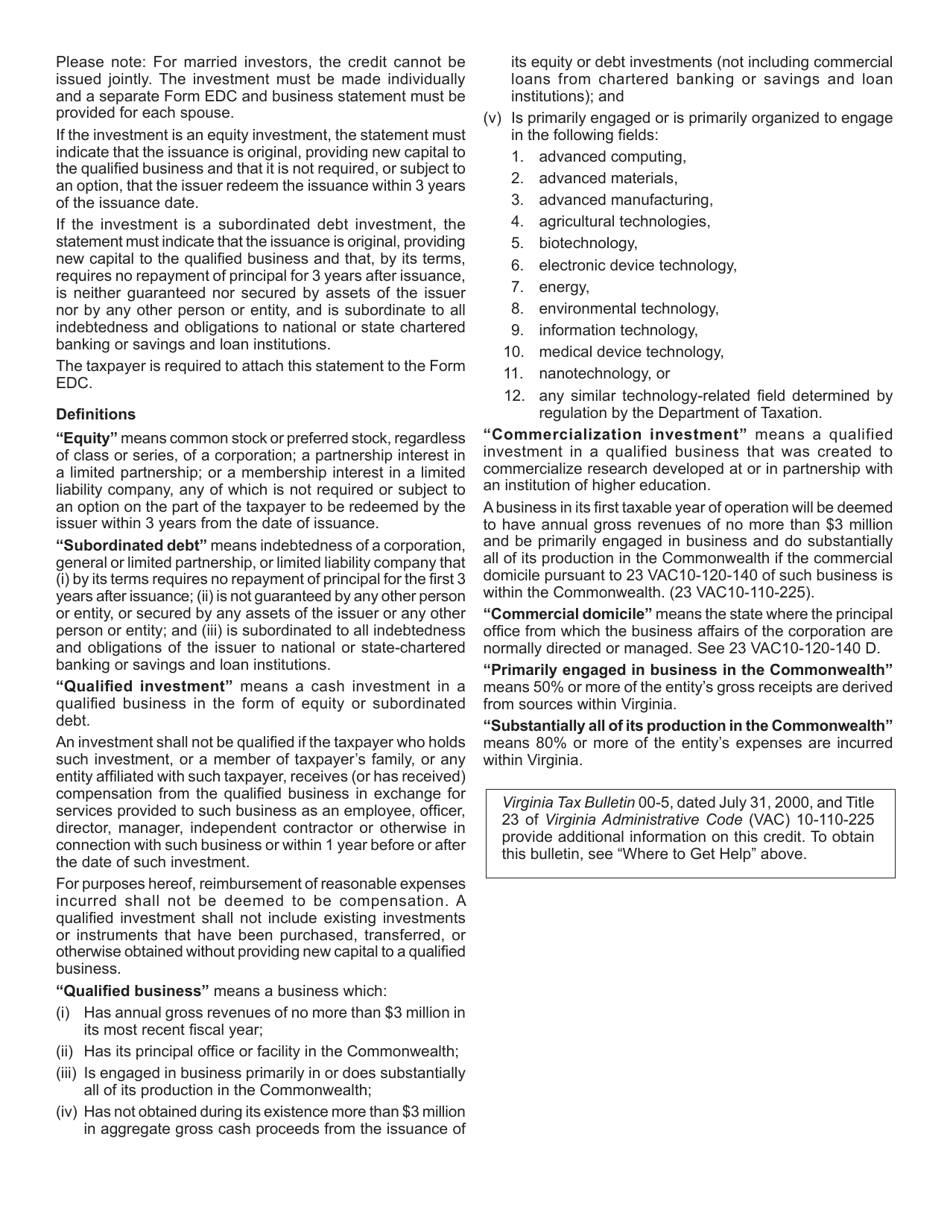

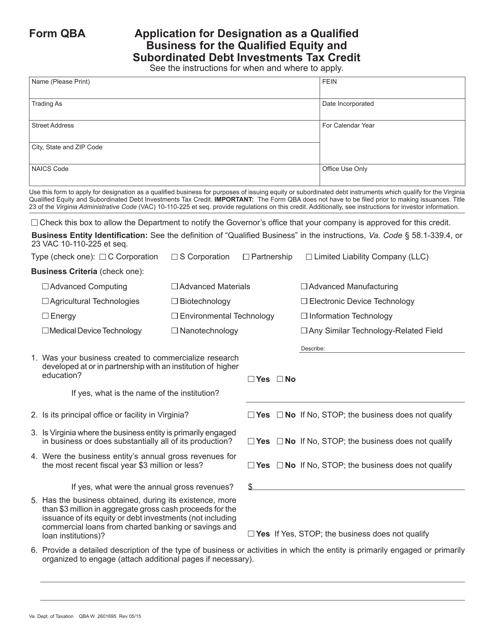

Form QBA Application for Designation as a Qualified Business for the Qualified Equity and Subordinated Debt Investments Tax Credit - Virginia

What Is Form QBA?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the QBA Application for Designation?

A: The QBA Application for Designation is a form used to apply for designation as a Qualified Business for the Qualified Equity and Subordinated Debt Investments Tax Credit in Virginia.

Q: What is the Qualified Equity and Subordinated Debt Investments Tax Credit?

A: The Qualified Equity and Subordinated Debt Investments Tax Credit is a tax credit available in Virginia for investments in certain qualified businesses.

Q: Who can apply for designation as a Qualified Business?

A: Any business that meets the eligibility criteria can apply for designation as a Qualified Business.

Q: What are the eligibility criteria for designation as a Qualified Business?

A: The eligibility criteria vary depending on the type of business and the investment amount. The specific requirements are outlined in the application form.

Q: How do I submit the QBA Application for Designation?

A: The application can be submitted electronically through the Virginia Business One Stop (VBO) portal or by mail.

Q: Are there any fees for submitting the application?

A: Yes, there is a non-refundable application fee. The fee amount is specified in the application form.

Form Details:

- Released on May 1, 2015;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form QBA by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.

Download Form QBA Application for Designation as a Qualified Business for the Qualified Equity and Subordinated Debt Investments Tax Credit - Virginia

1

2

3

4