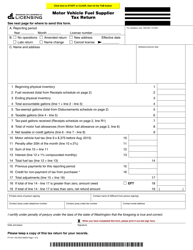

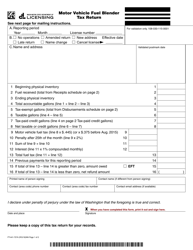

Instructions for Form FT-441-754 Motor Vehicle Fuel Supplier Tax Return - Washington

This document contains official instructions for Form FT-441-754 , Motor Vehicle Fuel Supplier Tax Return - a form released and collected by the Washington State Department of Licensing.

FAQ

Q: What is Form FT-441-754?

A: Form FT-441-754 is a Motor Vehicle Fuel Supplier Tax Return in Washington.

Q: Who needs to file Form FT-441-754?

A: Motor Vehicle Fuel Suppliers in Washington need to file Form FT-441-754.

Q: What is the purpose of Form FT-441-754?

A: The purpose of Form FT-441-754 is to report and pay motor vehicle fuel taxes in Washington as a supplier.

Q: When is the deadline to file Form FT-441-754?

A: Form FT-441-754 must be filed on a monthly basis, with the due date falling on or before the 25th day of the following month.

Q: What information is required on Form FT-441-754?

A: Form FT-441-754 requires information such as fuel sales and gallons delivered, credits and adjustments, and tax calculations.

Q: Are there any penalties for late filing of Form FT-441-754?

A: Yes, there are penalties for late filing or failure to file Form FT-441-754, including interest charges on unpaid taxes.

Q: Can I file Form FT-441-754 electronically?

A: Yes, Washington State allows electronic filing of Form FT-441-754 through their eFile system.

Instruction Details:

- This 2-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Washington State Department of Licensing.

Download Instructions for Form FT-441-754 Motor Vehicle Fuel Supplier Tax Return - Washington

1

2