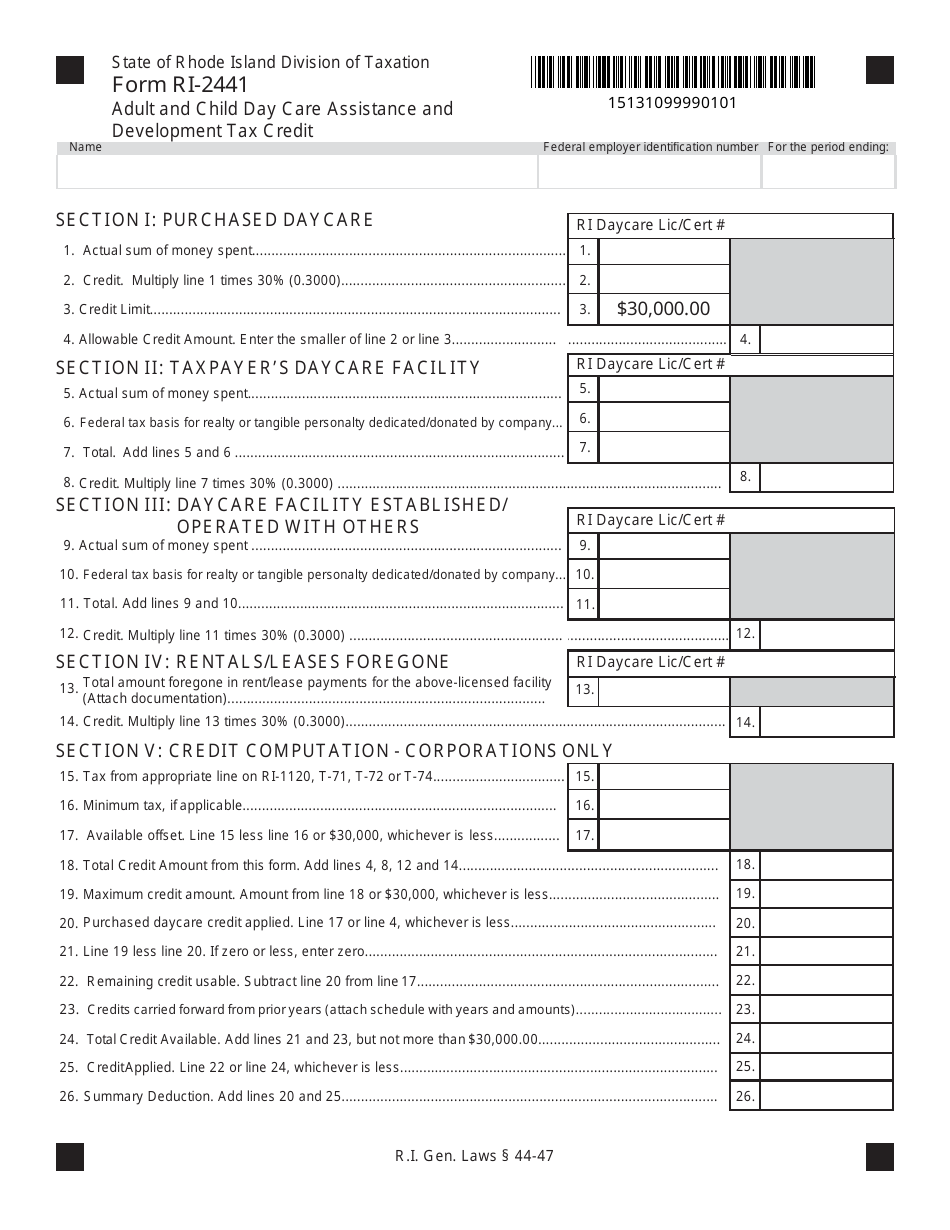

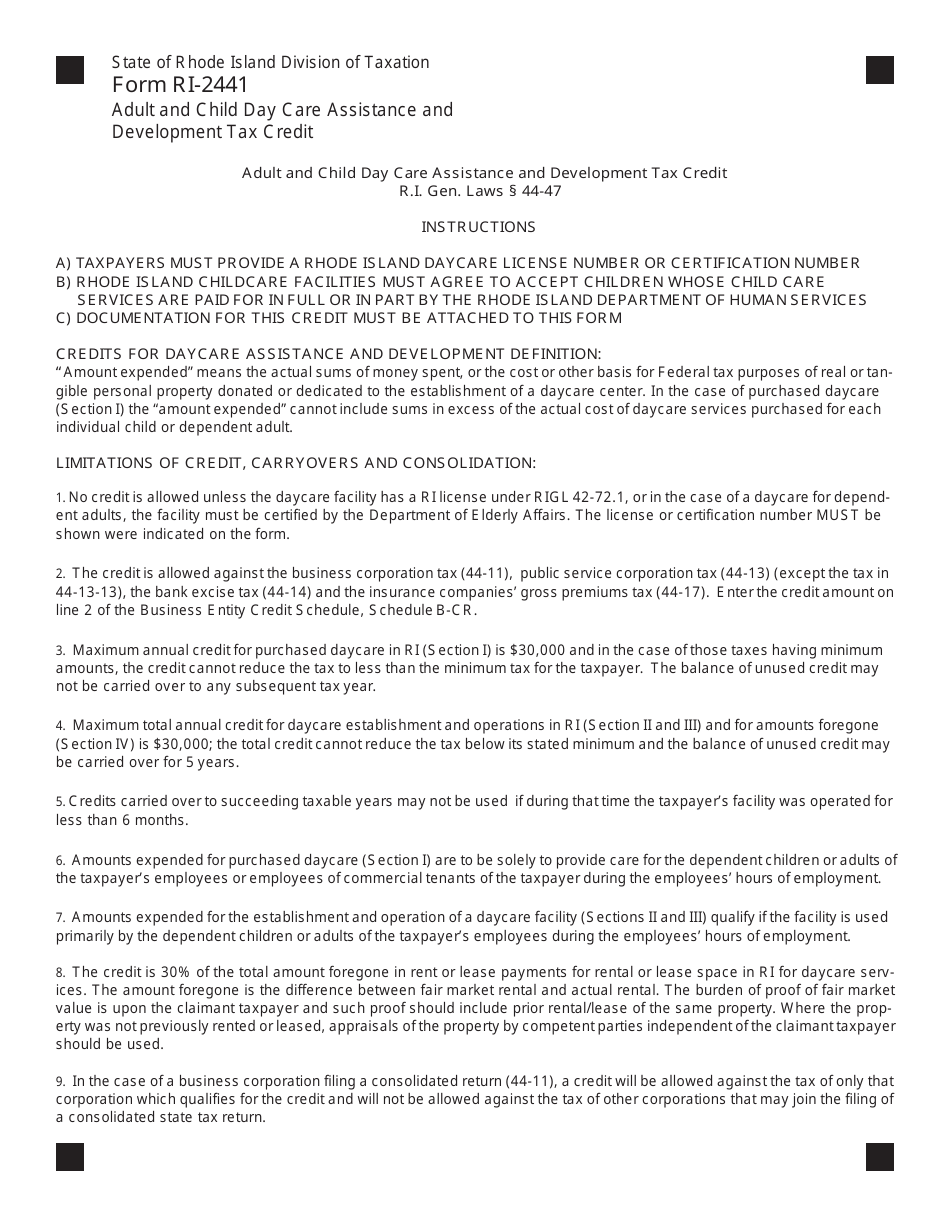

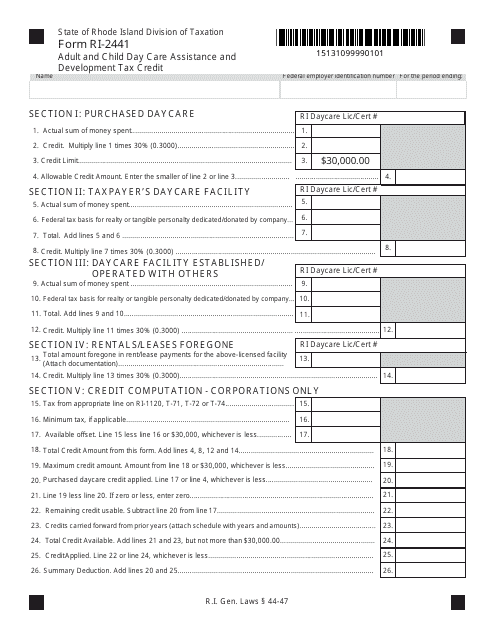

Form RI-2441 Adult and Child Day Care Assistance and Development Tax Credit - Rhode Island

Fill PDF Online

Fill out online for free

without registration or credit card

Download Form RI-2441 Adult and Child Day Care Assistance and Development Tax Credit - Rhode Island

1

2