![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form GST532

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form GST532

for the current year.

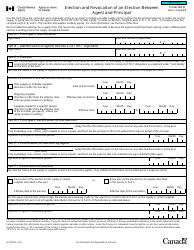

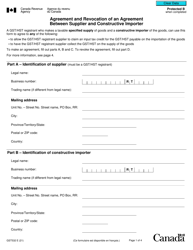

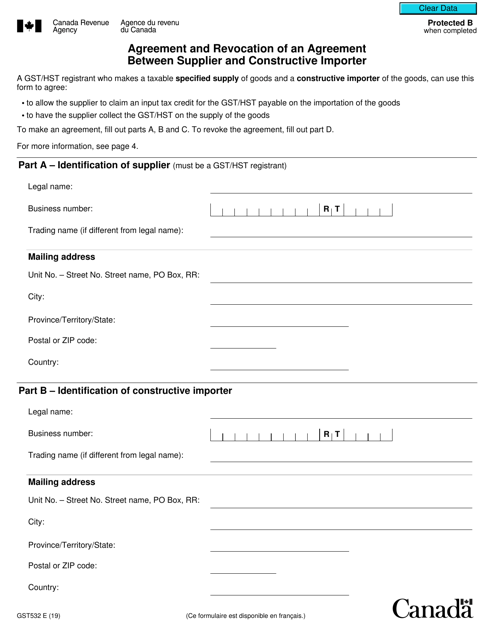

Form GST532 Agreement and Revocation of an Agreement Between Supplier and Constructive Importer - Canada

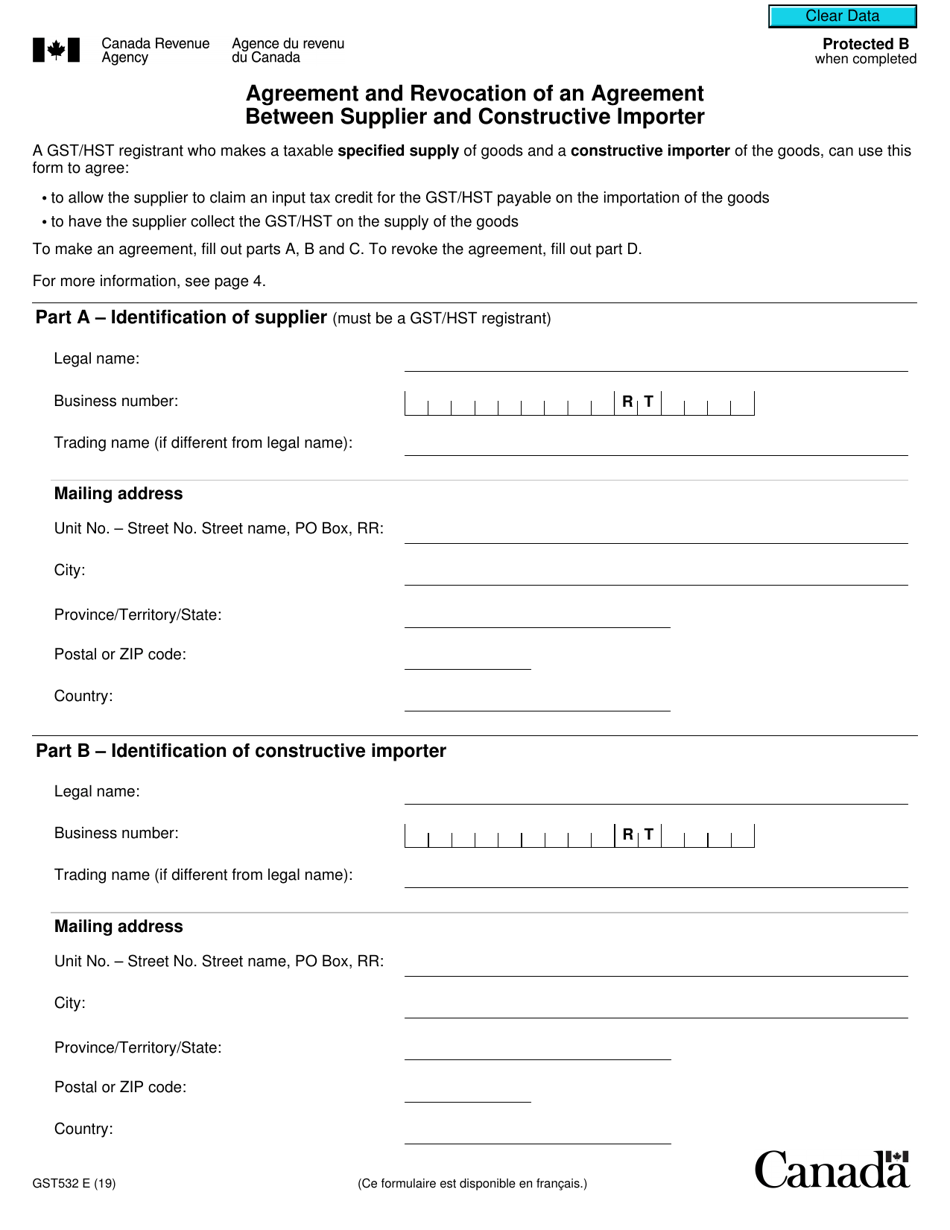

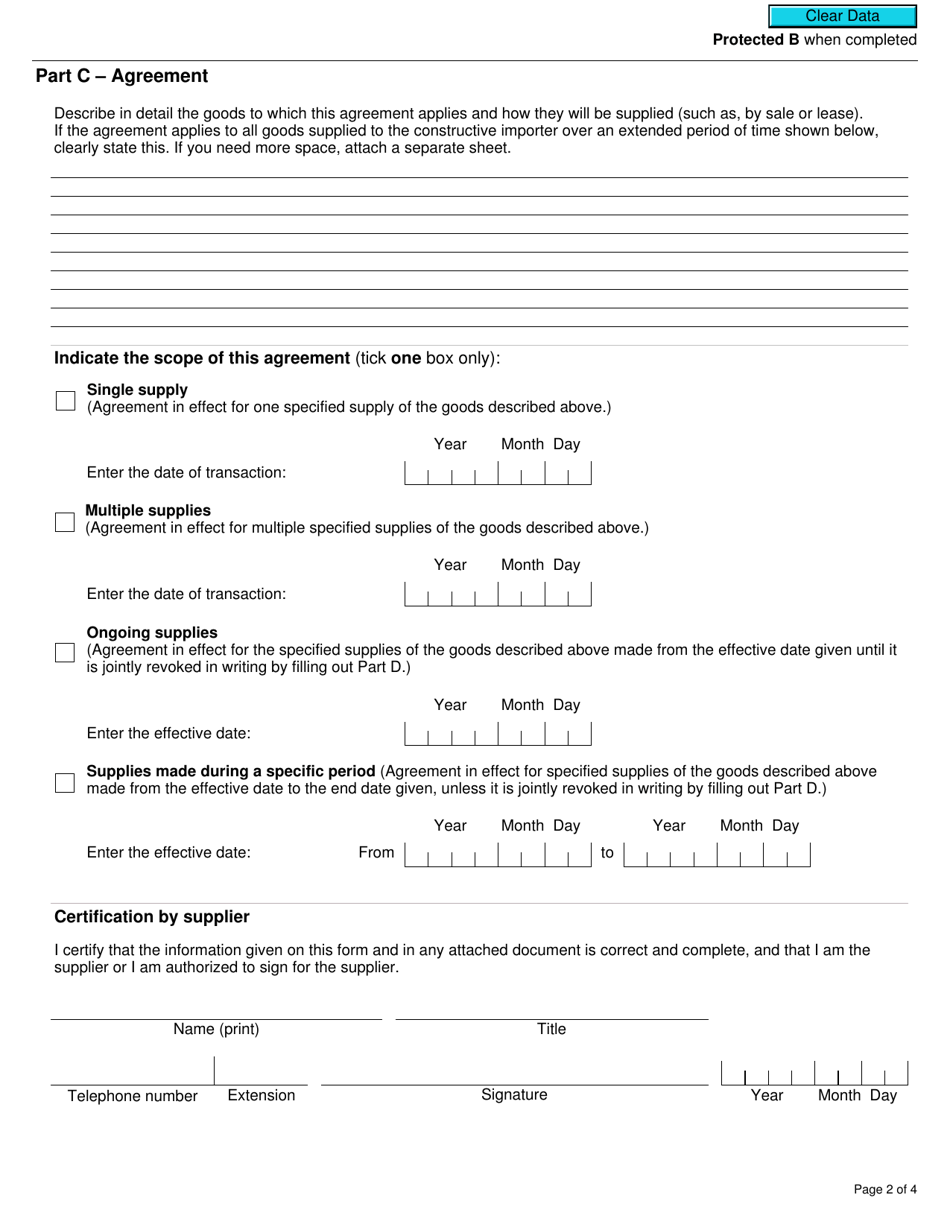

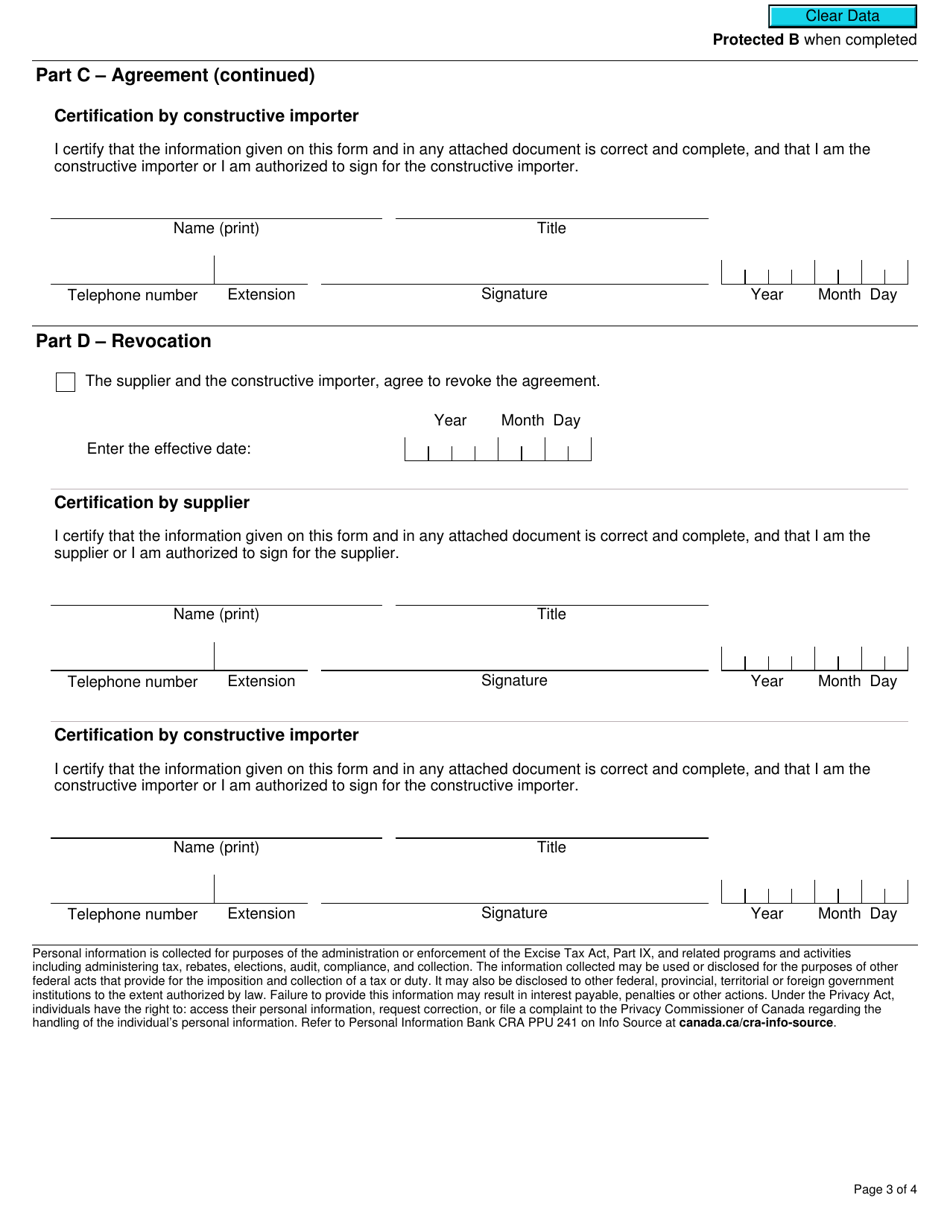

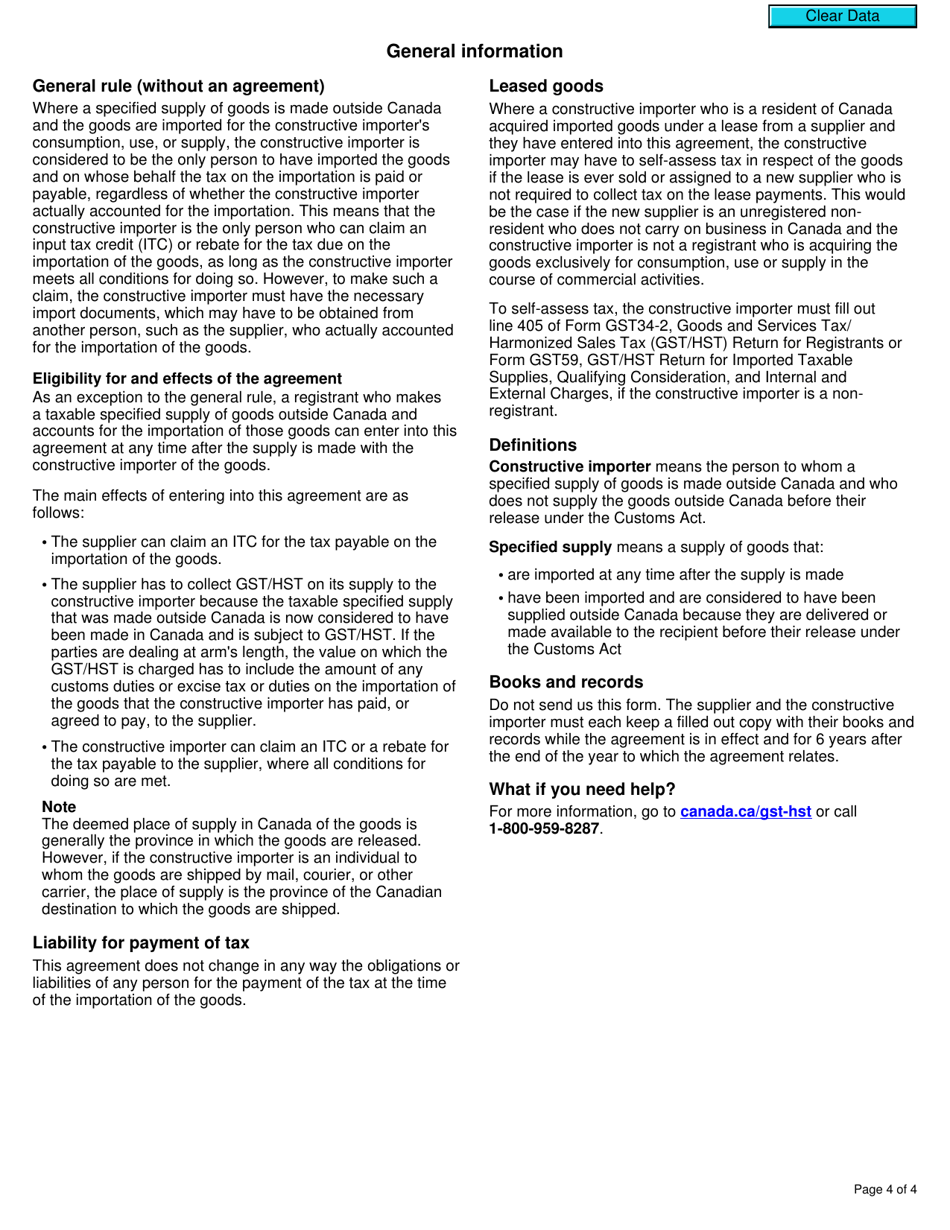

Form GST532 - Agreement and Revocation of an Agreement Between Supplier and Constructive Importer in Canada is used to establish or cancel an agreement between a supplier and a constructive importer for the collection and remittance of the Goods and Services Tax (GST). This form helps to determine the responsibility for paying the GST on imported goods.

The supplier files the Form GST532 Agreement and Revocation of an Agreement Between Supplier and Constructive Importer in Canada.

FAQ

Q: What is GST532 agreement?

A: GST532 agreement is a document that formalizes the relationship between a supplier and a constructive importer in Canada.

Q: What is a constructive importer?

A: A constructive importer is someone who is not the legal importer of goods, but who assumes the responsibilities of an importer for customs purposes.

Q: Why would a supplier and constructive importer enter into an agreement?

A: They would enter into an agreement to clarify each party's responsibilities and obligations regarding the importation of goods.

Q: What does the GST532 agreement cover?

A: The GST532 agreement covers various aspects such as the importation process, payment of duties and taxes, record-keeping requirements, and compliance with customs regulations.

Q: Can an agreement between a supplier and constructive importer be revoked?

A: Yes, the GST532 agreement can be revoked by either party with written notice to the other party.

Q: What happens if the GST532 agreement is revoked?

A: If the agreement is revoked, the supplier will resume their responsibilities as the legal importer of goods for customs purposes.

Download Form GST532 Agreement and Revocation of an Agreement Between Supplier and Constructive Importer - Canada

1

2

3

4