![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2220

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2220

for the current year.

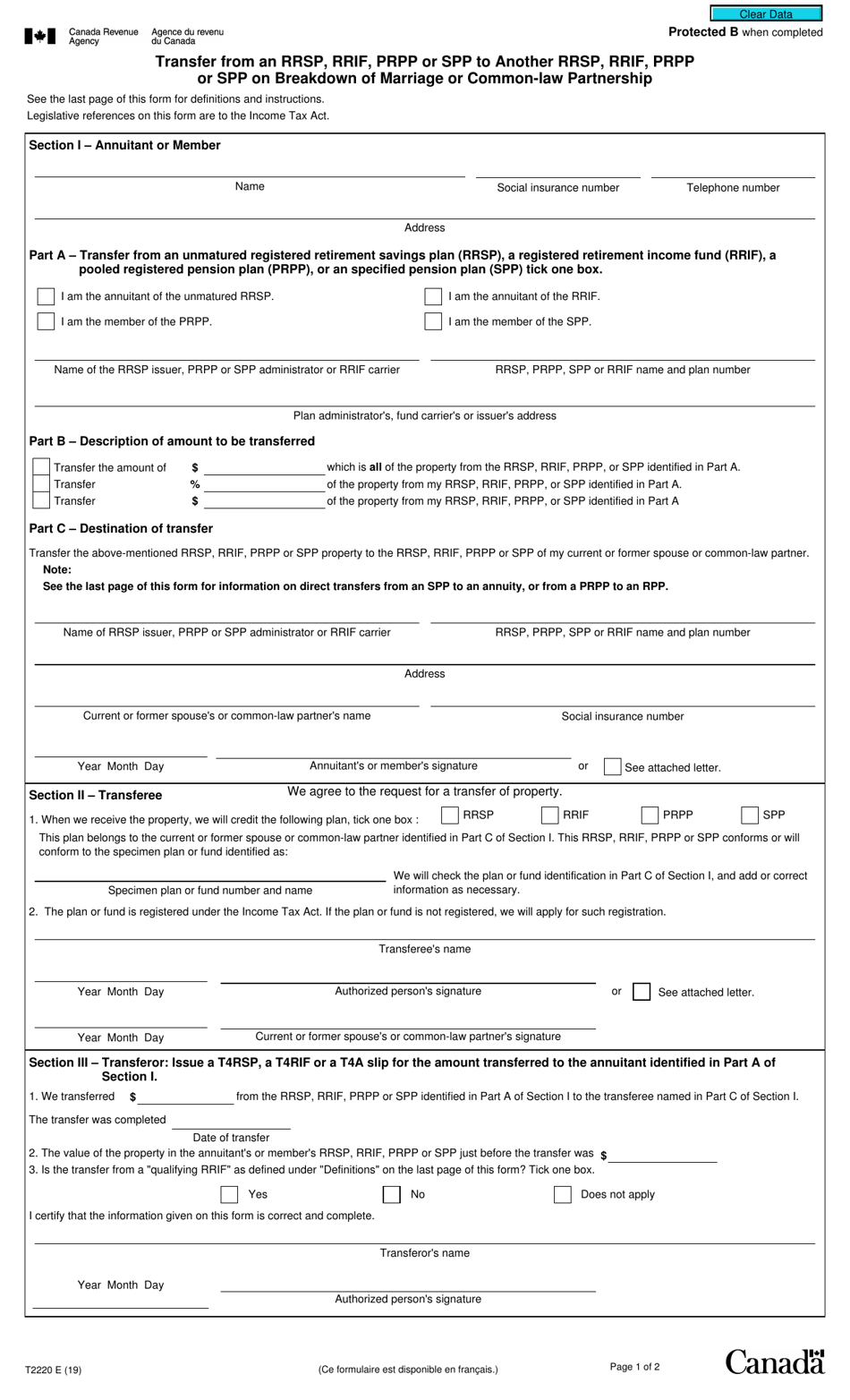

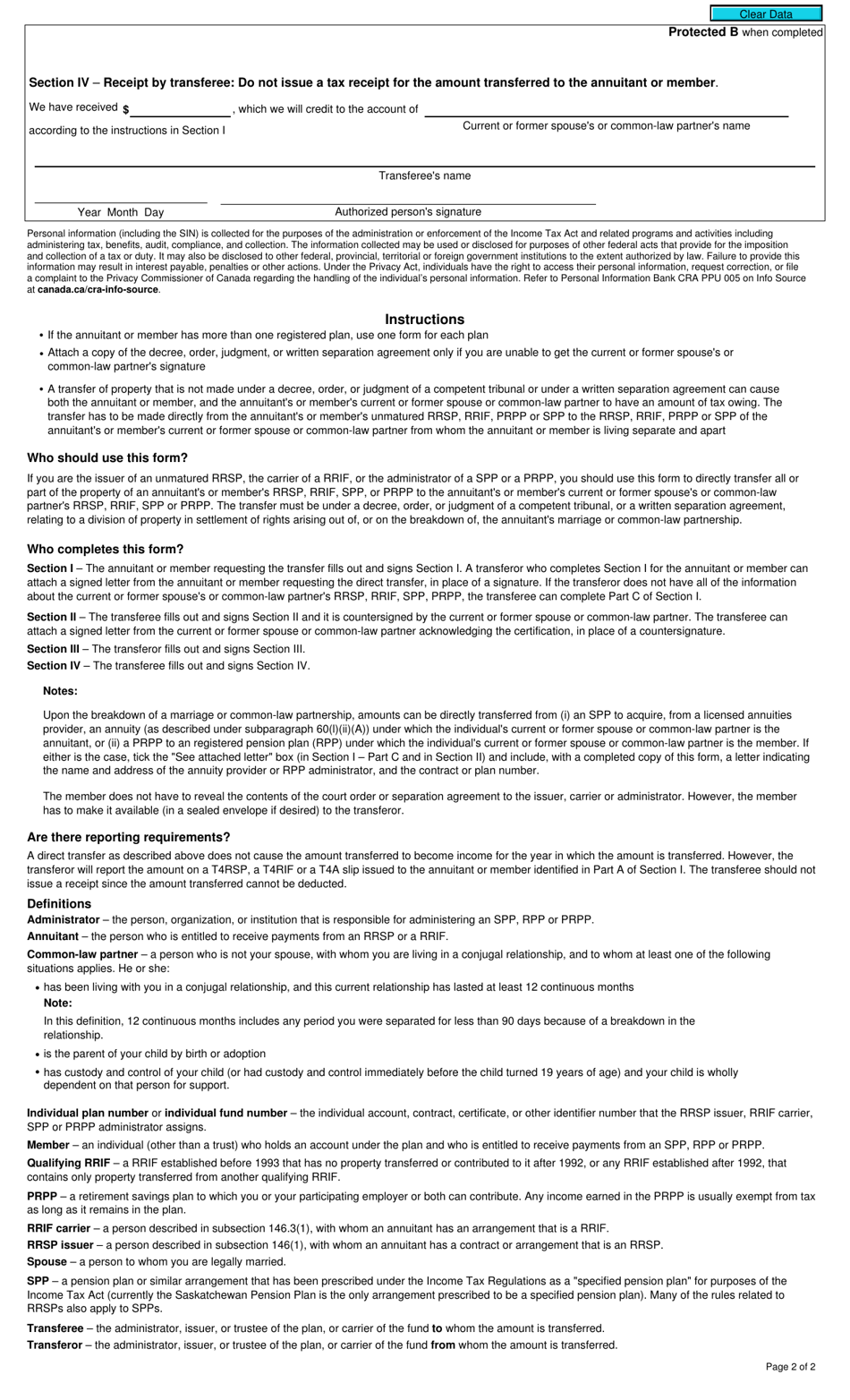

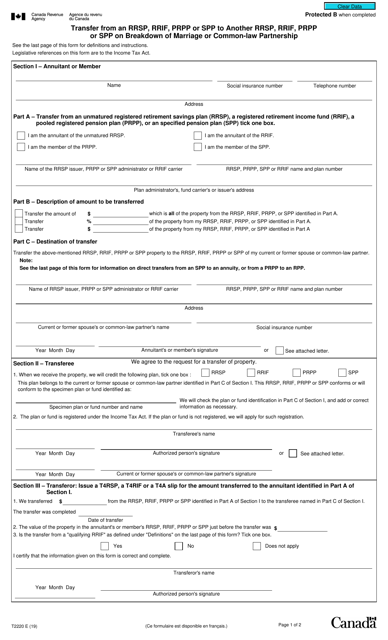

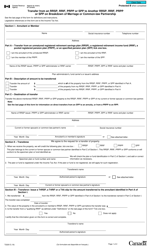

Form T2220 Transfer From an Rrsp, Rrif, Prpp or Spp to Another Rrsp, Rrif, Prpp or Spp on Breakdown of Marriage or Common-Law Partnership - Canada

What Is Form T2220?

Form T2220, Transfer From an RRSP, RRIF, PRPP or SPP to Another RRSP, RRIF, PRPP or SPP on Breakdown of Marriage or Common-Law Partnership , is completed to directly transfer property upon the breakdown of a marriage or common-law partnership from the following plans:

- Registered Retirement Savings Plan (RRSP);

- Registered Retirement Income Fund (RRIF);

- Pooled Registered Pension Plan (PRPP);

- Specified Pension Plan (SPP).

This form was issued by the Canadian Revenue Agency (CRA) on January 1, 2019 , with all previous editions obsolete. You can download a T2220 fillable form through the link below.

Who Needs to File Form T2220?

The T2220 Form must be completed by these individuals or organizations:

- Annuitant or member - the person who is entitled to receive RRSP or RRIF payments. Enter your name, social insurance number, telephone number, and address. Select the plan you are the annuitant or member of, indicate the amount to be transferred, and state the destination of the transfer. Include the names of the plan issuer and the plan itself, its number, your current or former spouse's or partner's name, address, and social insurance number. Sign and date the form.

- Transferee to whom the amount is transferred. Agree to the request for a transfer, select the plan, add the plan or fund number, and name. Confirm you have received the transfer that you will credit to the account of the spouse or partner. Write down your name, date, and sign the form. A spouse or partner must also sign the form.

- Transferor from whom the amount is transferred. Enter the transferred amount, the date of transfer, the value of the property, and state if the transfer was from a qualifying RRIF (see the instructions on the back of the form). Record your name, sign, and date the form.

Download Form T2220 Transfer From an Rrsp, Rrif, Prpp or Spp to Another Rrsp, Rrif, Prpp or Spp on Breakdown of Marriage or Common-Law Partnership - Canada

1

2