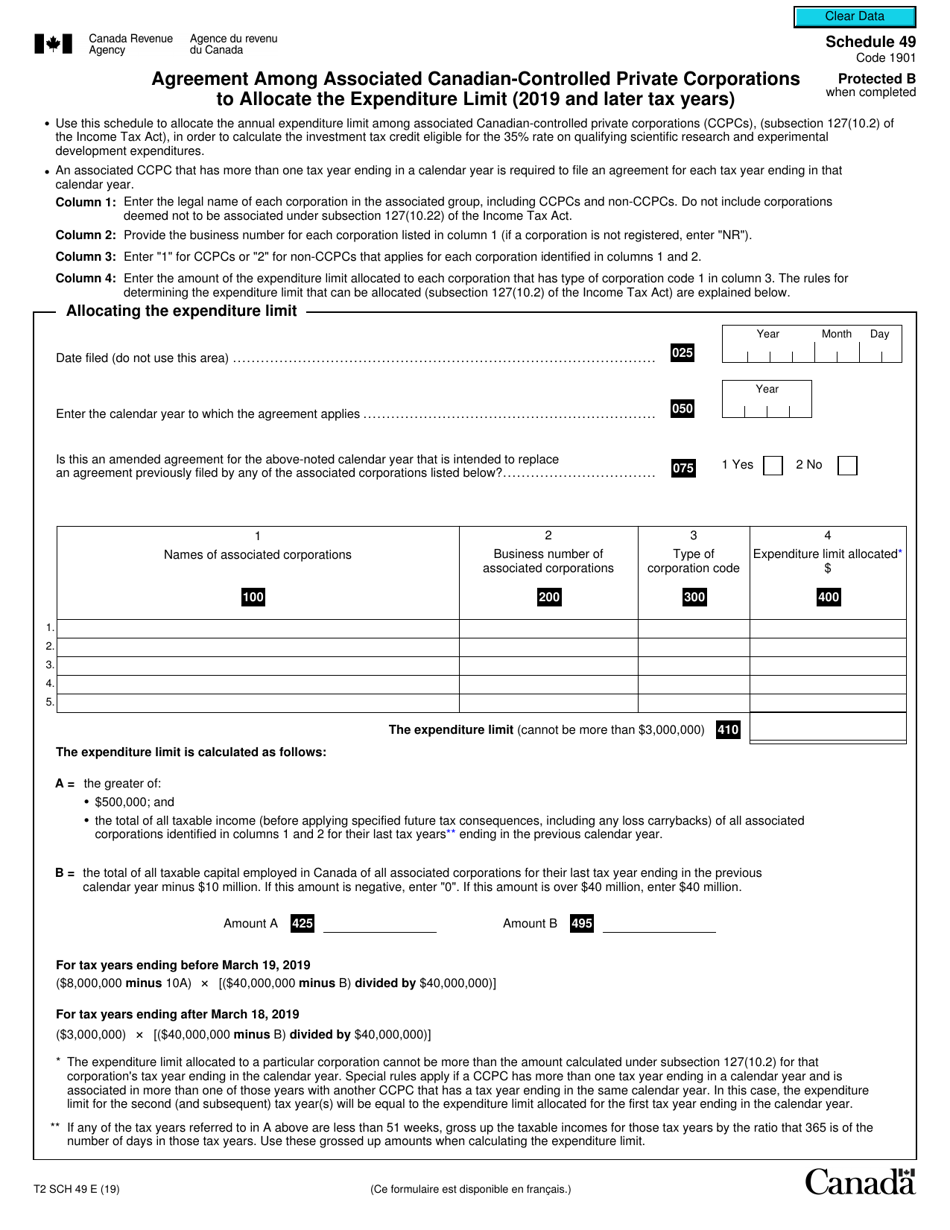

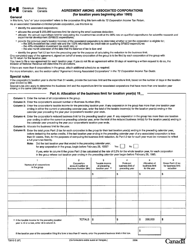

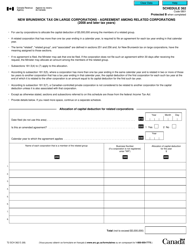

Form T2 Schedule 49 Agreement Among Associated Canadian-Controlled Private Corporations to Allocate the Expenditure Limit (2019 and Later Tax Years) - Canada

Form T2 Schedule 49 is a tax form used in Canada for associated Canadian-controlled private corporations (CCPCs) to allocate the expenditure limit. The expenditure limit refers to the maximum amount of qualifying scientific research and experimental development (SR&ED) expenses that a group of associated CCPCs can claim for tax credit purposes. This form is used to determine how the expenditure limit is to be divided among the associated CCPCs within a group. Basically, it helps allocate and maximize the tax benefits for research and development activities among multiple Canadian-controlled private corporations.

The Form T2 Schedule 49 Agreement Among Associated Canadian-Controlled Private Corporations to Allocate the Expenditure Limit is to be filed by Canadian-controlled private corporations in Canada. The purpose of this form is to allocate the expenditure limit among corporations that have entered into an agreement to share the limit.

FAQ

Q: What is Form T2 Schedule 49?

A: Form T2 Schedule 49 is a tax form in Canada that is used by associated Canadian-controlled private corporations (CCPCs) to allocate the expenditure limit for tax years starting in 2019 and later.

Q: What are associated Canadian-controlled private corporations (CCPCs)?

A: Associated Canadian-controlled private corporations (CCPCs) are corporations that are connected by share ownership or control. CCPCs are Canadian resident corporations that are not controlled by non-residents or public corporations.

Q: What is the expenditure limit for associated CCPCs?

A: The expenditure limit for associated CCPCs is the maximum amount of qualified expenditures that can be eligible for the enhanced tax deduction under the Scientific Research and Experimental Development (SR&ED) program.

Q: Why do associated CCPCs need to allocate the expenditure limit?

A: Associated CCPCs need to allocate the expenditure limit to ensure that each corporation's qualified expenditures are properly accounted for and do not exceed the maximum limit.

Q: Can associated CCPCs allocate the expenditure limit in any way they want?

A: No, the allocation of the expenditure limit among associated CCPCs must be done in accordance with certain conditions and restrictions as outlined by the Canadian Revenue Agency (CRA).

Q: Are there any specific rules or guidelines for completing Form T2 Schedule 49?

A: Yes, the CRA provides instructions and guidelines on how to complete Form T2 Schedule 49. It is important to carefully follow these instructions to ensure accurate reporting of the expenditure limit allocation.

Q: Is Form T2 Schedule 49 required for all associated CCPCs?

A: Form T2 Schedule 49 is only required for associated CCPCs that are eligible for the enhanced SR&ED tax deduction and have agreed to allocate the expenditure limit among themselves.

Q: When is the deadline for filing Form T2 Schedule 49?

A: The deadline for filing Form T2 Schedule 49 is the same as the deadline for filing the corporate tax return, which is generally within 6 months after the end of the corporation's tax year.

Q: What happens if Form T2 Schedule 49 is not filed or filed incorrectly?

A: Failure to file Form T2 Schedule 49 or filing it incorrectly may result in penalties or delays in processing the corporation's tax return. It is important to ensure that the form is completed accurately and submitted on time.