![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2 Schedule 8

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2 Schedule 8

for the current year.

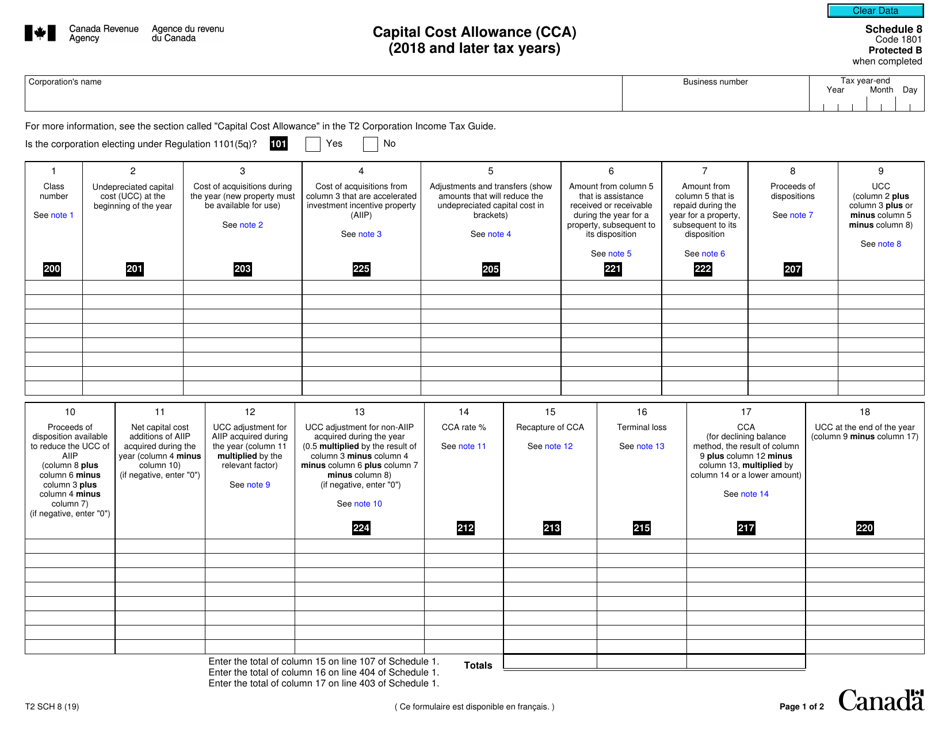

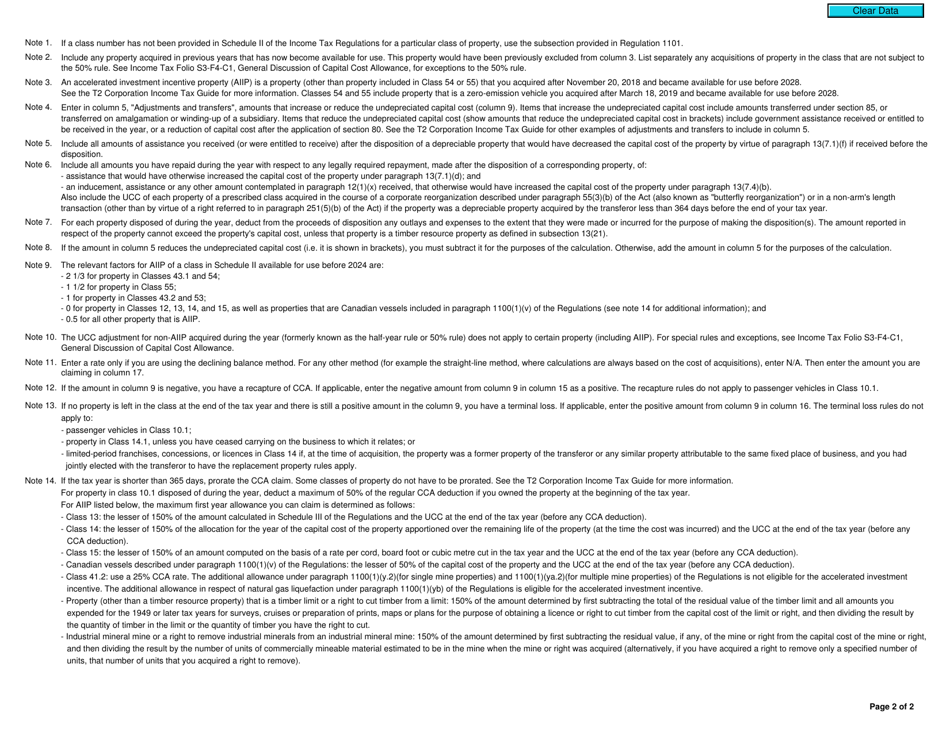

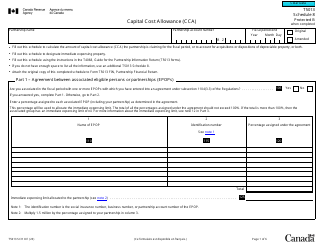

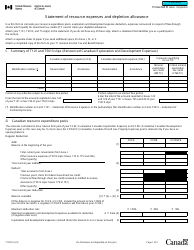

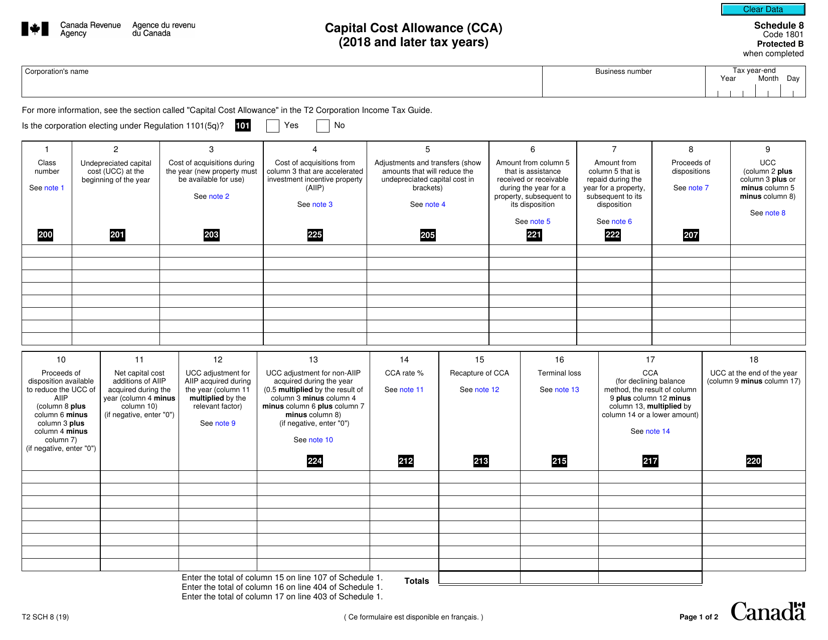

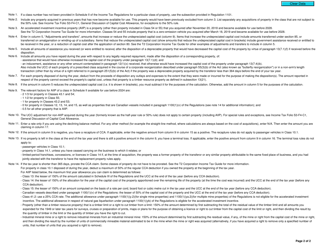

Form T2 Schedule 8 Capital Cost Allowance (Cca) (2018 and Later Tax Years) - Canada

Form T2 Schedule 8 Capital Cost Allowance (CCA) in Canada is used to calculate the tax deductions for capital assets acquired by a business. It helps determine the yearly depreciation amount that can be claimed to reduce the taxable income.

The Form T2 Schedule 8 Capital Cost Allowance (CCA) in Canada is filed by corporations when calculating their capital cost allowance for tax years starting in 2018 and onwards.

FAQ

Q: What is Form T2 Schedule 8?

A: Form T2 Schedule 8 is a tax form used in Canada to calculate Capital Cost Allowance (CCA) for assets.

Q: What is Capital Cost Allowance (CCA)?

A: Capital Cost Allowance (CCA) is a tax deduction that businesses in Canada can claim for the depreciation of their capital assets.

Q: When should Form T2 Schedule 8 be used?

A: Form T2 Schedule 8 should be used for tax years starting in 2018 and onwards.

Q: What information is required to complete Form T2 Schedule 8?

A: To complete Form T2 Schedule 8, you will need to know the details of your capital assets, such as their purchase cost, class, and the year they were acquired.

Q: Can I claim Capital Cost Allowance (CCA) for all types of assets?

A: No, not all types of assets are eligible for Capital Cost Allowance (CCA). The eligibility depends on the class of the asset and the Canadian tax regulations.

Q: How does Capital Cost Allowance (CCA) affect my taxes?

A: Claiming Capital Cost Allowance (CCA) reduces your taxable income, which can lower your overall tax liability.

Q: Is there a deadline to file Form T2 Schedule 8?

A: The deadline to file Form T2 Schedule 8 is generally within six months of the end of your corporation's tax year, but it may vary depending on your specific situation. It is recommended to consult the CRA or a tax professional for accurate filing deadlines.

Q: Are there any penalties for not filing Form T2 Schedule 8?

A: Yes, there may be penalties for not filing Form T2 Schedule 8 or for filing it late. It is important to meet the deadlines and fulfill your tax obligations to avoid penalties.

Q: Can I make changes to Form T2 Schedule 8 after filing it?

A: If you need to make changes to Form T2 Schedule 8 after filing it, you will need to file an adjustment request with the CRA. It is recommended to consult a tax professional for assistance with filing adjustments.

Download Form T2 Schedule 8 Capital Cost Allowance (Cca) (2018 and Later Tax Years) - Canada

1

2