![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form T3 Schedule 1A

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form T3 Schedule 1A

for the current year.

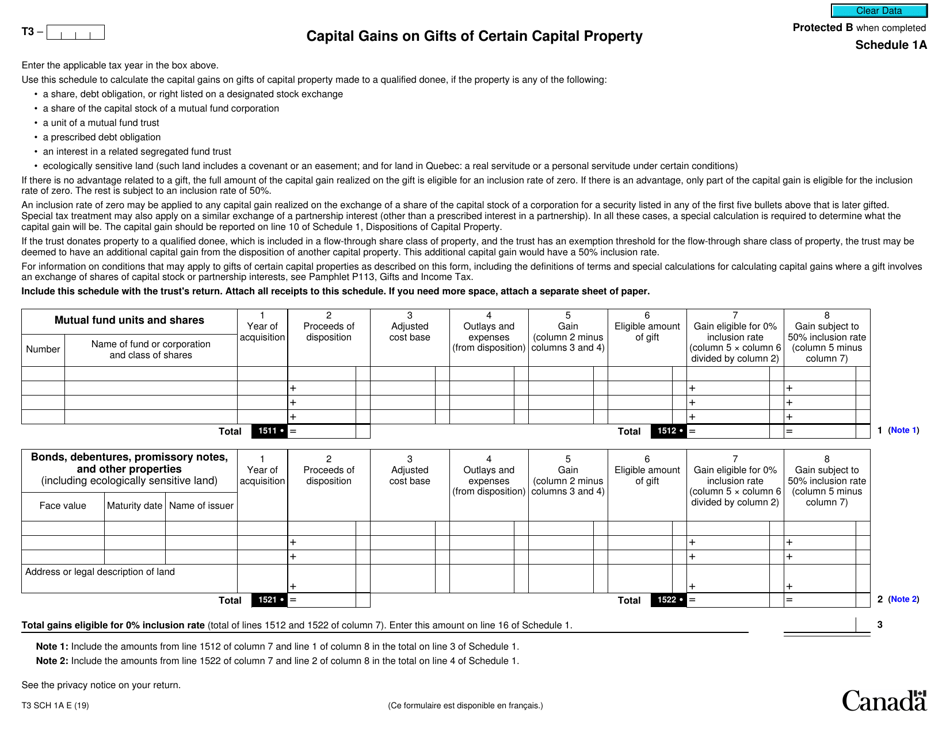

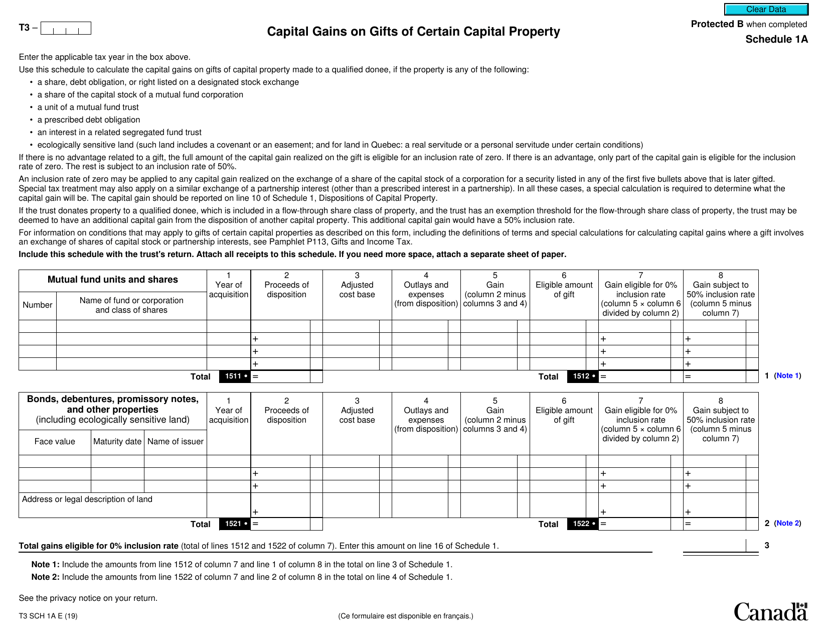

Form T3 Schedule 1A Capital Gains on Gifts of Certain Capital Property - Canada

Form T3 Schedule 1A in Canada is used to report any capital gains or losses on gifts of certain capital property that were made during the taxation year. It is specifically meant for the taxation of trusts.

The Form T3 Schedule 1A Capital Gains on Gifts of Certain Capital Property in Canada is filed by the estate or trust that received a gift of certain capital property.

FAQ

Q: What is Form T3 Schedule 1A?

A: Form T3 Schedule 1A is a form used in Canada to report capital gains on gifts of certain capital property.

Q: What is capital gains?

A: Capital gains are profits made from the sale or disposition of a capital asset.

Q: What is considered certain capital property?

A: Certain capital property refers to specific types of assets, such as real estate, stocks, or bonds.

Q: Do I need to file Form T3 Schedule 1A?

A: You need to file Form T3 Schedule 1A if you have capital gains from gifting certain capital property.

Q: What is the purpose of filing Form T3 Schedule 1A?

A: The purpose of filing Form T3 Schedule 1A is to report and calculate any capital gains tax owed on gifts of certain capital property.

Q: When is the deadline to file Form T3 Schedule 1A?

A: The deadline to file Form T3 Schedule 1A is typically the same as the deadline for filing your income tax return, which is April 30th for most individuals.

Q: Are there any penalties for not filing Form T3 Schedule 1A?

A: Yes, there can be penalties for not filing Form T3 Schedule 1A, such as late filing penalties or interest charges on any tax owed.

Q: Do I need to include supporting documentation with Form T3 Schedule 1A?

A: Yes, you may need to include supporting documentation, such as receipts or documents related to the gift of capital property.

Q: Who should I contact if I need help with Form T3 Schedule 1A?

A: If you need help with Form T3 Schedule 1A, you can contact the Canada Revenue Agency (CRA) or seek assistance from a tax professional.