![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 80-315

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form 80-315

for the current year.

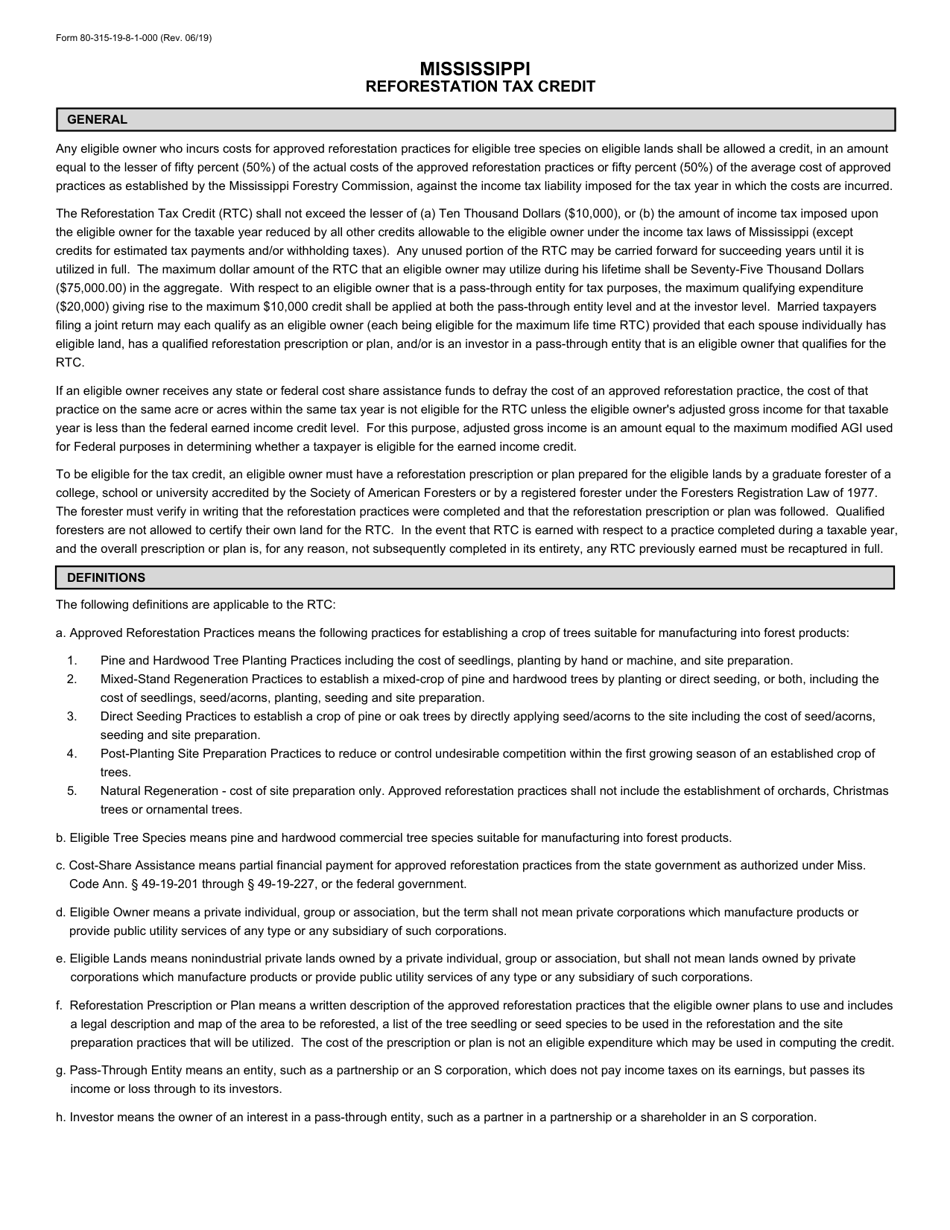

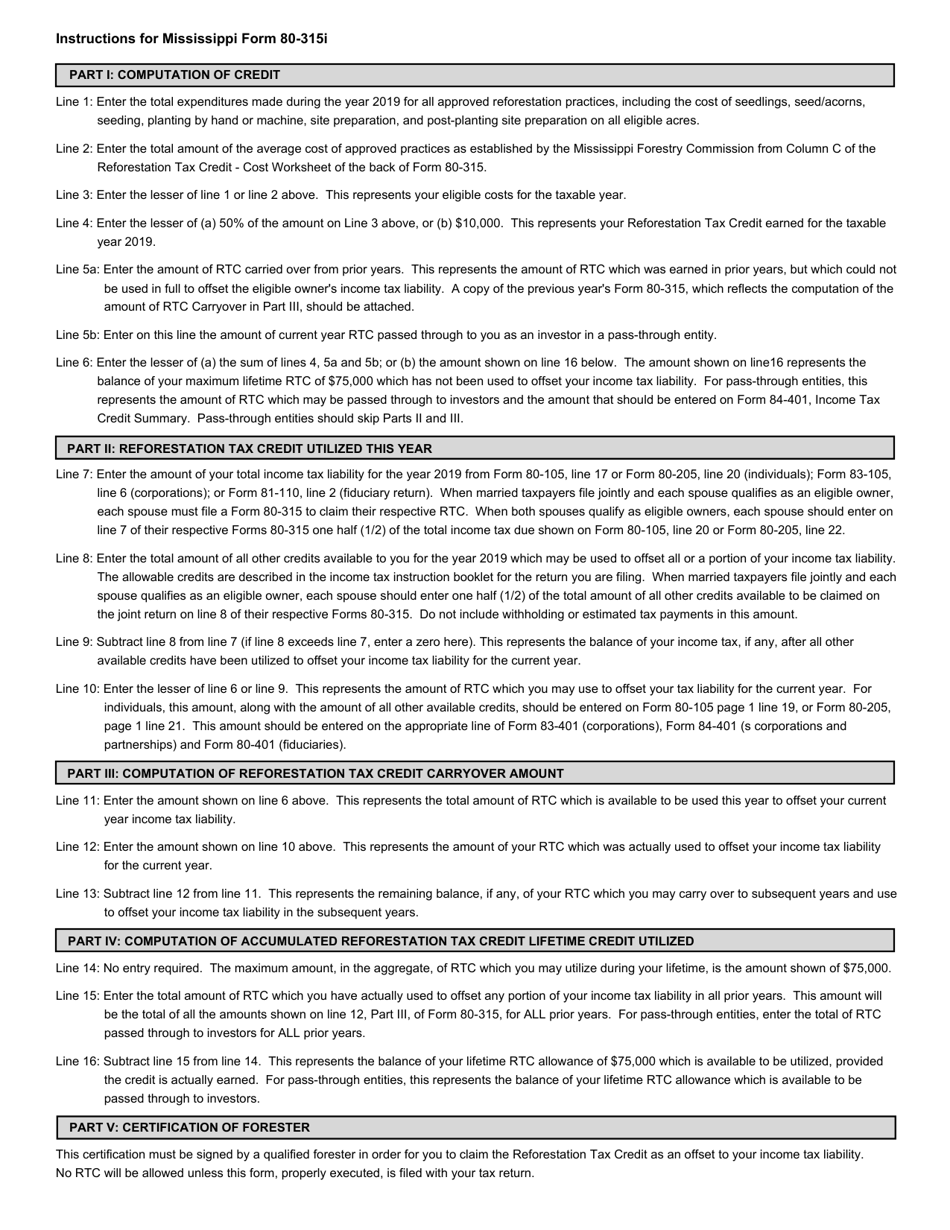

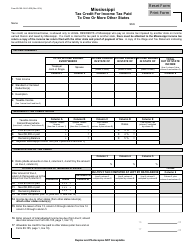

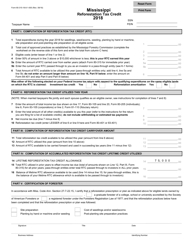

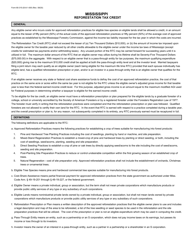

Instructions for Form 80-315 Mississippi Reforestation Tax Credit - Mississippi

This document contains official instructions for Form 80-315 , Mississippi Reforestation Tax Credit - a form released and collected by the Mississippi Department of Revenue.

FAQ

Q: What is Form 80-315?

A: Form 80-315 is the Mississippi Reforestation Tax Credit form.

Q: What is the purpose of Form 80-315?

A: The purpose of Form 80-315 is to claim the Mississippi Reforestation Tax Credit.

Q: Who is eligible to use Form 80-315?

A: Any individual or entity engaged in reforestation activities in Mississippi may be eligible to use Form 80-315.

Q: What is the Mississippi Reforestation Tax Credit?

A: The Mississippi Reforestation Tax Credit is a credit provided to individuals or entities engaged in reforestation activities in Mississippi.

Q: What expenses are eligible for the tax credit?

A: Expenses related to the establishment and maintenance of a reforestation site are generally eligible for the tax credit.

Q: How much is the tax credit?

A: The tax credit amount varies and is determined based on the number of acres reforested and other factors. It is best to refer to the Form 80-315 instructions for specific information.

Q: What documents should be attached to Form 80-315?

A: The specific documents required to be attached to Form 80-315 are listed in the form's instructions. Generally, documentation related to reforestation expenses should be included.

Q: When is the deadline to file Form 80-315?

A: The deadline to file Form 80-315 is generally the same as the deadline for filing your Mississippi income tax return, which is April 15th.

Q: Can the tax credit be carried forward or refunded?

A: Yes, any unused portion of the tax credit can be carried forward for up to 5 years, and in some cases, may be refundable.

Instruction Details:

- This 2-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Mississippi Department of Revenue.

1

2