![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form N-210

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form N-210

for the current year.

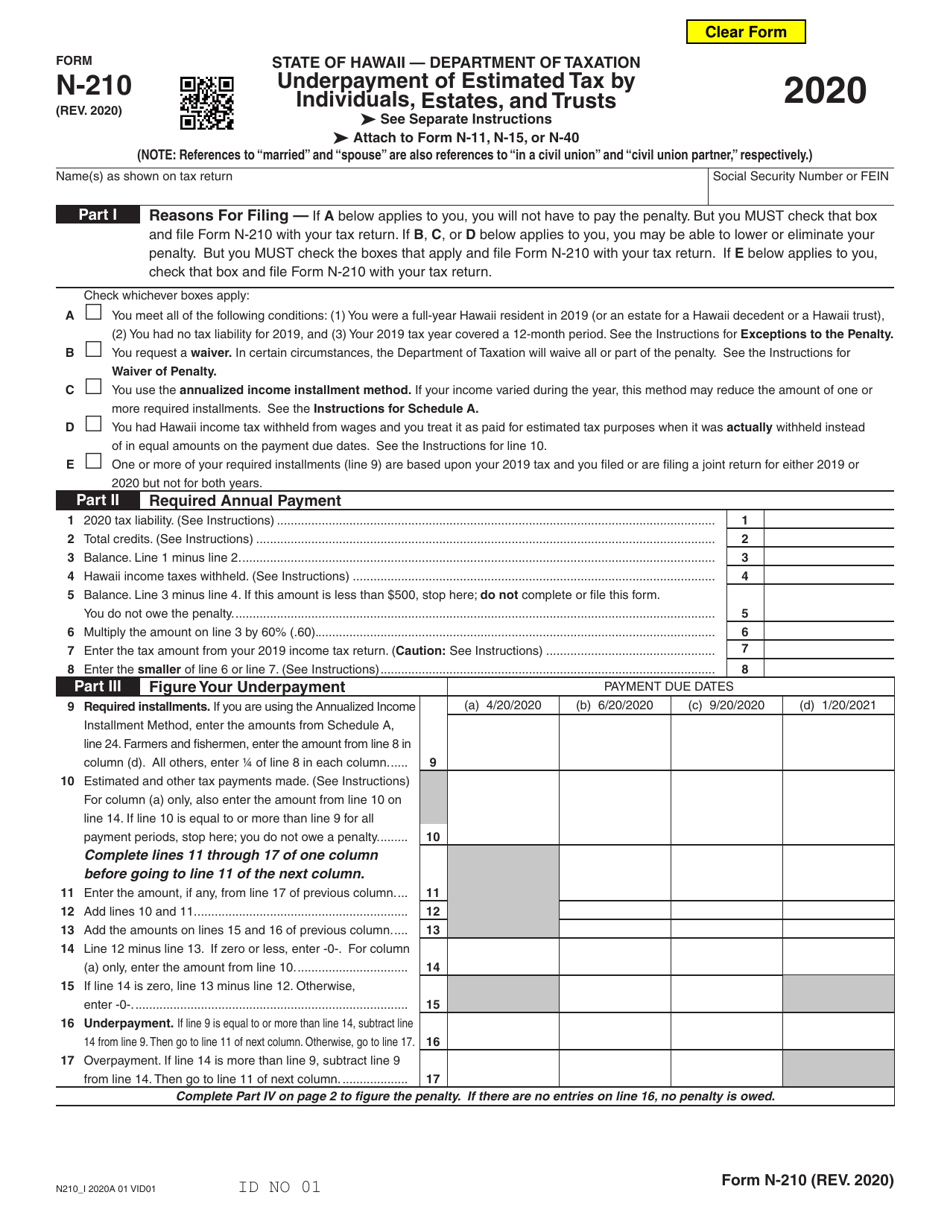

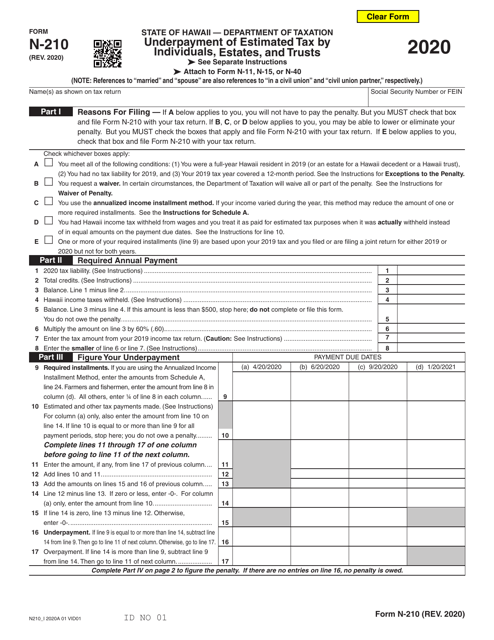

Form N-210 Underpayment of Estimated Tax by Individuals, Estates, and Trusts - Hawaii

What Is Form N-210?

This is a legal form that was released by the Hawaii Department of Taxation - a government authority operating within Hawaii. Check the official instructions before completing and submitting the form.

FAQ

Q: What is Form N-210?

A: Form N-210 is a tax form used in Hawaii to calculate and pay any underpayment of estimated tax by individuals, estates, and trusts.

Q: Who needs to file Form N-210?

A: Individuals, estates, and trusts in Hawaii who have underpaid their estimated tax during the tax year need to file Form N-210.

Q: When is Form N-210 due?

A: Form N-210 is due on or before the 20th day of the fourth month following the close of the tax year.

Q: How do I calculate the underpayment of estimated tax?

A: You can use the instructions provided with Form N-210 to calculate the underpayment of estimated tax.

Q: Are there any penalties for underpayment of estimated tax?

A: Yes, there may be penalties for underpayment of estimated tax. You should refer to the instructions for Form N-210 to understand the penalties and how to avoid them.

Form Details:

- Released on January 1, 2020;

- The latest edition provided by the Hawaii Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form N-210 by clicking the link below or browse more documents and templates provided by the Hawaii Department of Taxation.

Download Form N-210 Underpayment of Estimated Tax by Individuals, Estates, and Trusts - Hawaii

1

2