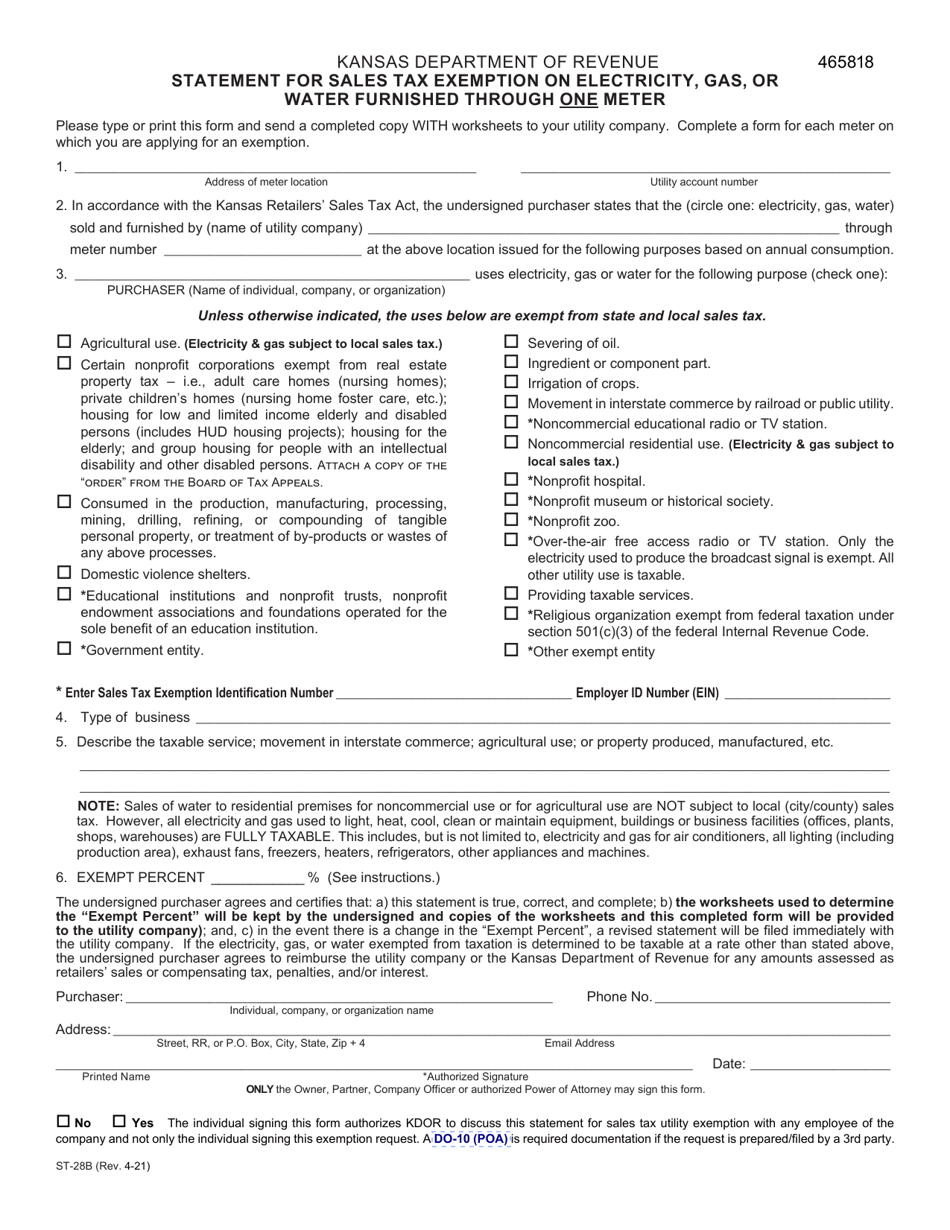

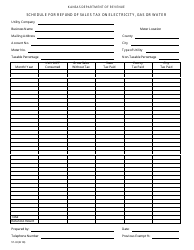

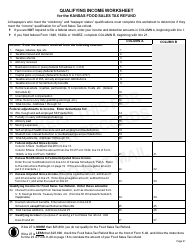

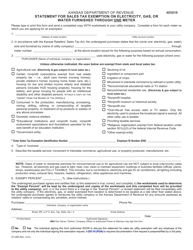

Form ST-28B Statement for Sales Tax Exemption on Electricity, Gas, or Water Furnished Through One Meter - Kansas

What Is Form ST-28B?

This is a legal form that was released by the Kansas Department of Revenue - a government authority operating within Kansas. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form ST-28B?

A: Form ST-28B is a statement used for sales tax exemption on electricity, gas, or water furnished through one meter in Kansas.

Q: Who uses Form ST-28B?

A: Form ST-28B is used by businesses or organizations that qualify for a sales tax exemption on electricity, gas, or water.

Q: What is the purpose of Form ST-28B?

A: The purpose of Form ST-28B is to document and claim the sales tax exemption on electricity, gas, or water furnished through one meter.

Q: How do I qualify for a sales tax exemption on electricity, gas, or water?

A: To qualify for a sales tax exemption, you must be a business or organization that meets specific criteria outlined by the Kansas Department of Revenue.

Q: What information do I need to provide on Form ST-28B?

A: You will need to provide your business or organization's information, account number, and details about the electricity, gas, or water usage.

Q: Are there any deadlines for submitting Form ST-28B?

A: The deadlines for submitting Form ST-28B may vary. It is recommended to check with the Kansas Department of Revenue for specific deadlines.

Q: What should I do with completed Form ST-28B?

A: You should keep a copy of the completed Form ST-28B for your records and submit it to the Kansas Department of Revenue as instructed.

Form Details:

- Released on April 1, 2021;

- The latest edition provided by the Kansas Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form ST-28B by clicking the link below or browse more documents and templates provided by the Kansas Department of Revenue.

Download Form ST-28B Statement for Sales Tax Exemption on Electricity, Gas, or Water Furnished Through One Meter - Kansas

1

2