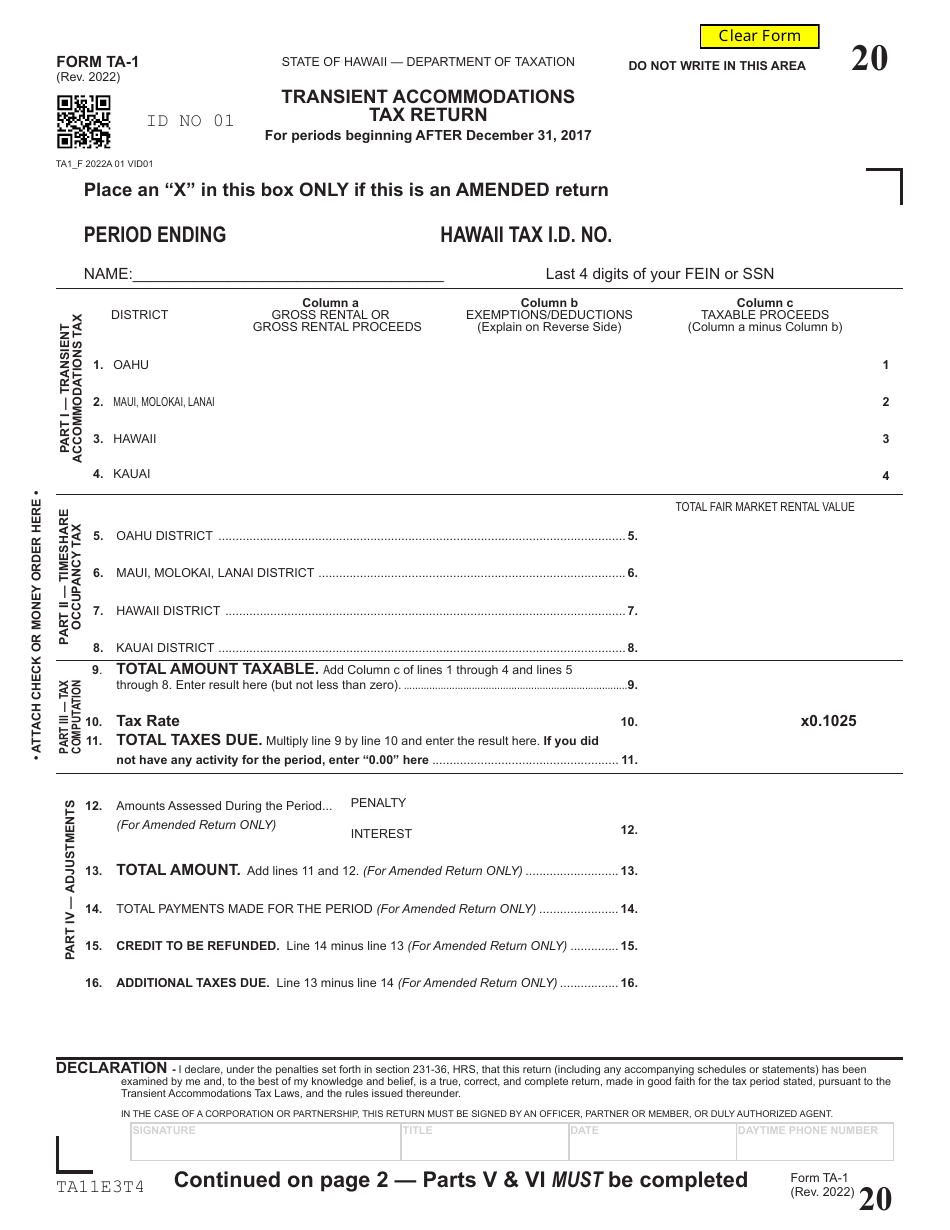

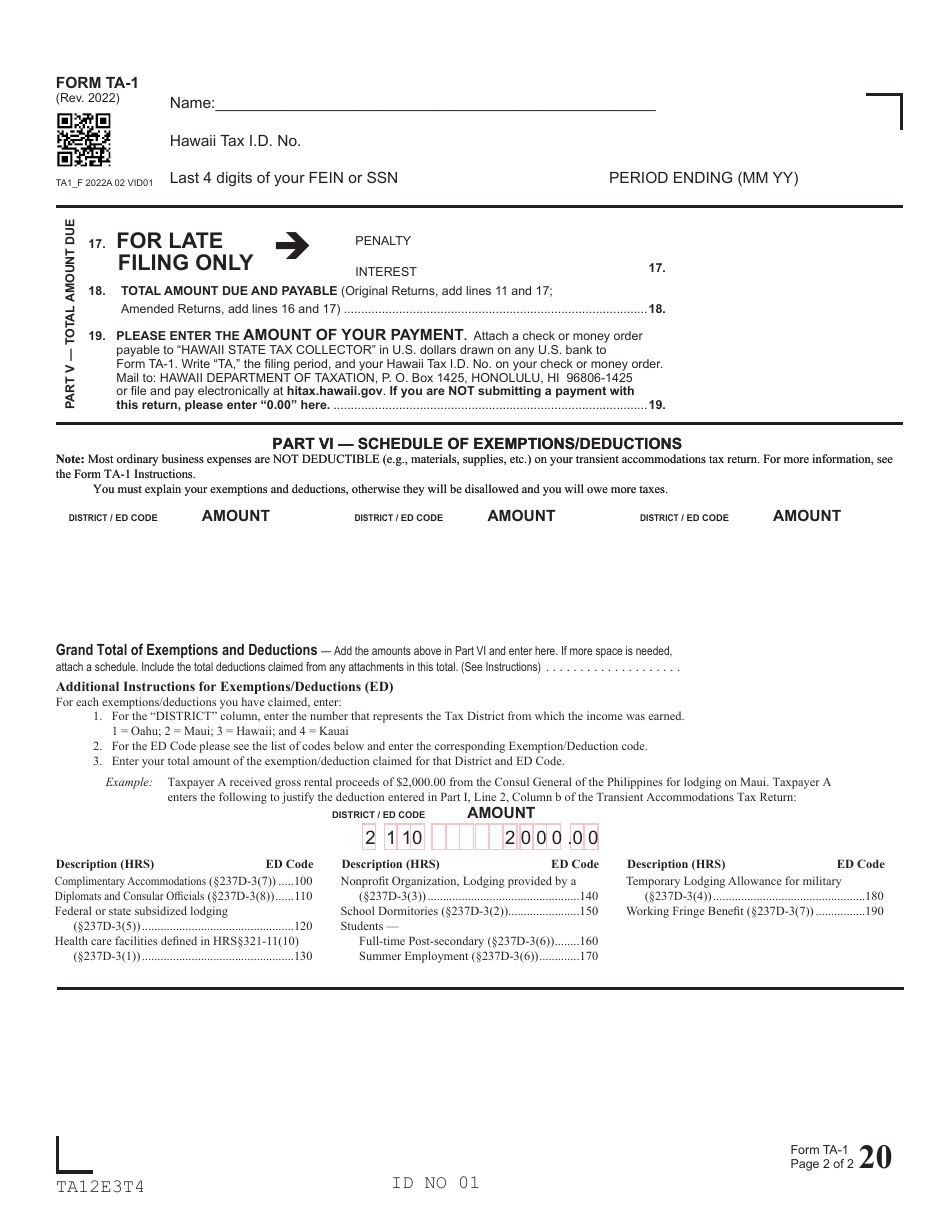

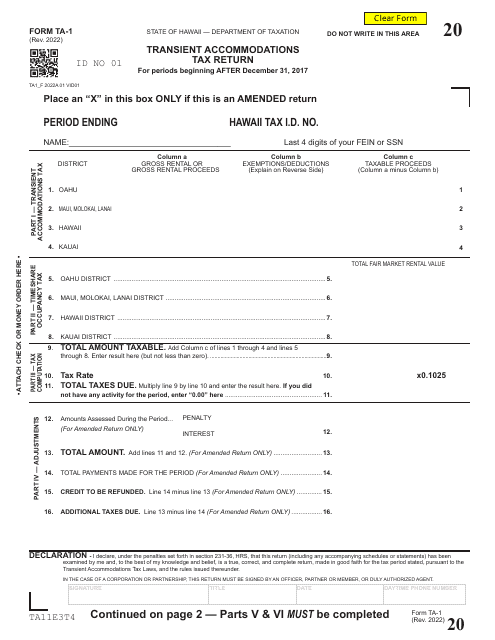

Form TA-1 Transient Accommodations Tax Return for Periods Beginning After December 31, 2017 - Hawaii

What Is Form TA-1?

This is a legal form that was released by the Hawaii Department of Taxation - a government authority operating within Hawaii. Check the official instructions before completing and submitting the form.

FAQ

Q: What is Form TA-1?

A: Form TA-1 is the Transient Accommodations Tax Return for periods beginning after December 31, 2017 in Hawaii.

Q: Who needs to file Form TA-1?

A: Businesses or individuals who provide transient accommodations in Hawaii need to file Form TA-1.

Q: What is Transient Accommodations Tax?

A: Transient Accommodations Tax is a tax imposed on the gross rental income from transient accommodations.

Q: When should Form TA-1 be filed?

A: Form TA-1 should be filed on a monthly basis, with the tax remitted by the 20th day of the following month.

Q: Are there any penalties for late filing or non-filing?

A: Yes, there are penalties for late filing or non-filing, including interest charges and possible criminal prosecution.

Q: What supporting documents should be included with Form TA-1?

A: Supporting documents such as rental receipts and a record of the number of rental days should be included with Form TA-1.

Q: Are there any exemptions or exclusions from Transient Accommodations Tax?

A: Yes, there are certain exemptions and exclusions from Transient Accommodations Tax, such as government-owned accommodations and certain rentals to federal employees.

Form Details:

- Released on January 1, 2022;

- The latest edition provided by the Hawaii Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form TA-1 by clicking the link below or browse more documents and templates provided by the Hawaii Department of Taxation.

Download Form TA-1 Transient Accommodations Tax Return for Periods Beginning After December 31, 2017 - Hawaii

1

2