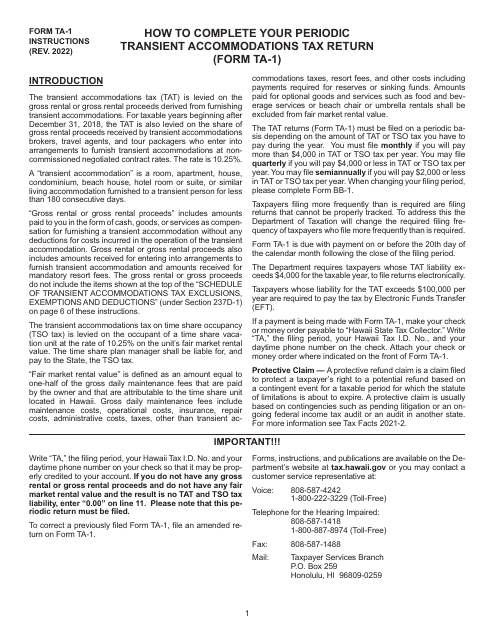

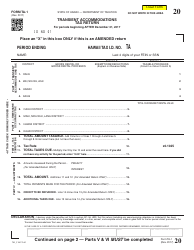

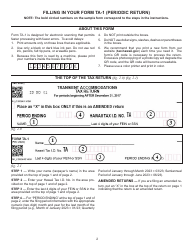

Instructions for Form TA-1 Transient Accommodations Tax Return for Periods Beginning After December 31, 2017 - Hawaii

This document contains official instructions for Form TA-1 , Transient Accommodations Tax Return for Periods Beginning After December 31, 2017 - a form released and collected by the Hawaii Department of Taxation. An up-to-date fillable Form TA-1 is available for download through this link.

FAQ

Q: What is Form TA-1?

A: Form TA-1 is the Transient Accommodations Tax Return for periods beginning after December 31, 2017 in Hawaii.

Q: Who needs to file Form TA-1?

A: Any individual or business that operates transient accommodations in Hawaii needs to file Form TA-1.

Q: What is Transient Accommodations Tax?

A: Transient Accommodations Tax is a tax imposed on the gross rental income derived from transient accommodations in Hawaii.

Q: When is the deadline for filing Form TA-1?

A: The deadline for filing Form TA-1 is the last day of the month following the end of the reporting period.

Q: Are there any penalties for late filing or non-filing?

A: Yes, there are penalties for late filing or non-filing of Form TA-1. The penalties can range from late filing penalties to substantial understatement penalties.

Q: What should be included in the gross rental income reported on Form TA-1?

A: The gross rental income reported on Form TA-1 should include all fees, charges, or other consideration received for the right to use or occupy the transient accommodation.

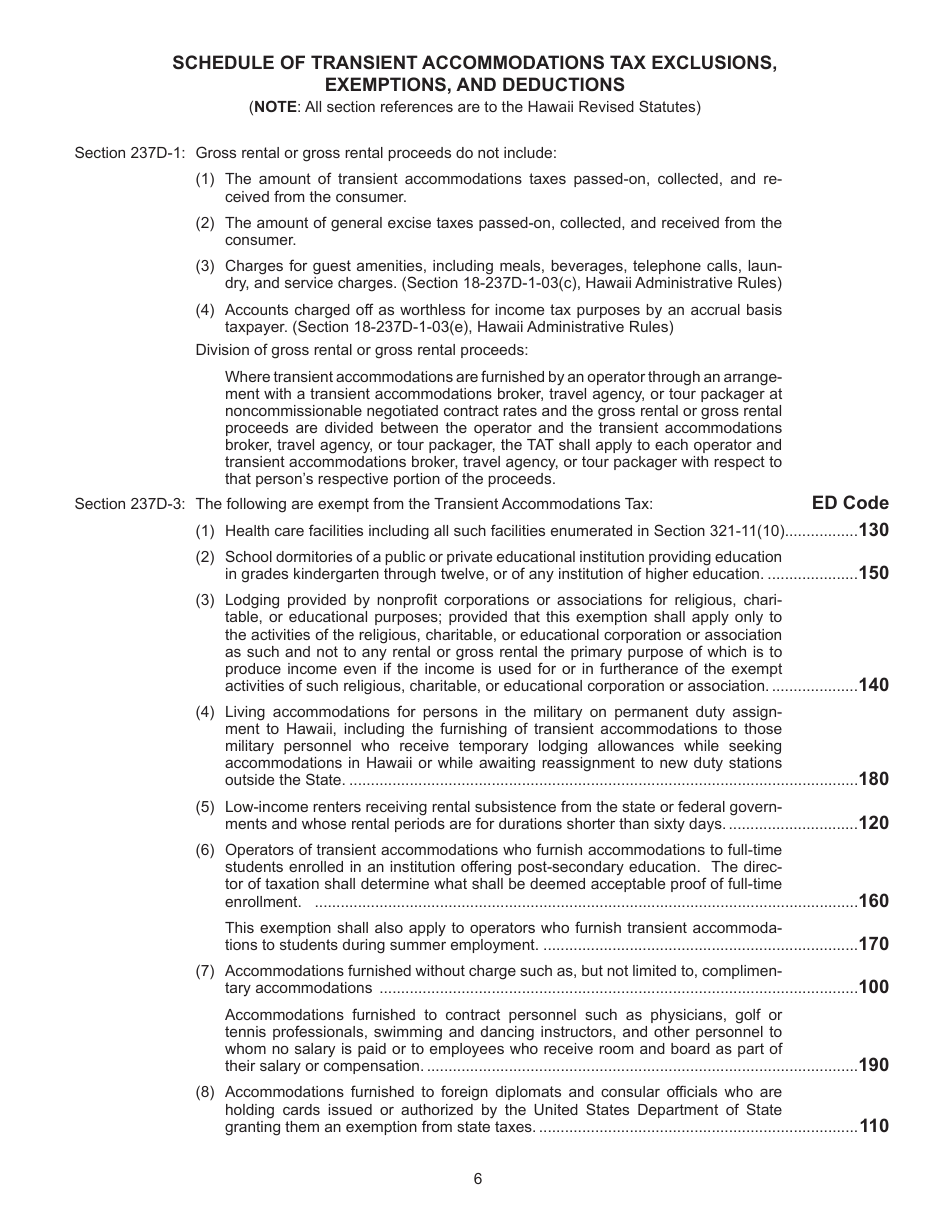

Q: Are there any exemptions or exclusions from the Transient Accommodations Tax?

A: Yes, there are certain exemptions and exclusions from the Transient Accommodations Tax. These include rentals to federal employees, certain schools or nonprofit organizations, and certain long-term rentals.

Instruction Details:

- This 6-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Hawaii Department of Taxation.

Download Instructions for Form TA-1 Transient Accommodations Tax Return for Periods Beginning After December 31, 2017 - Hawaii

1

2

3

4

5

6