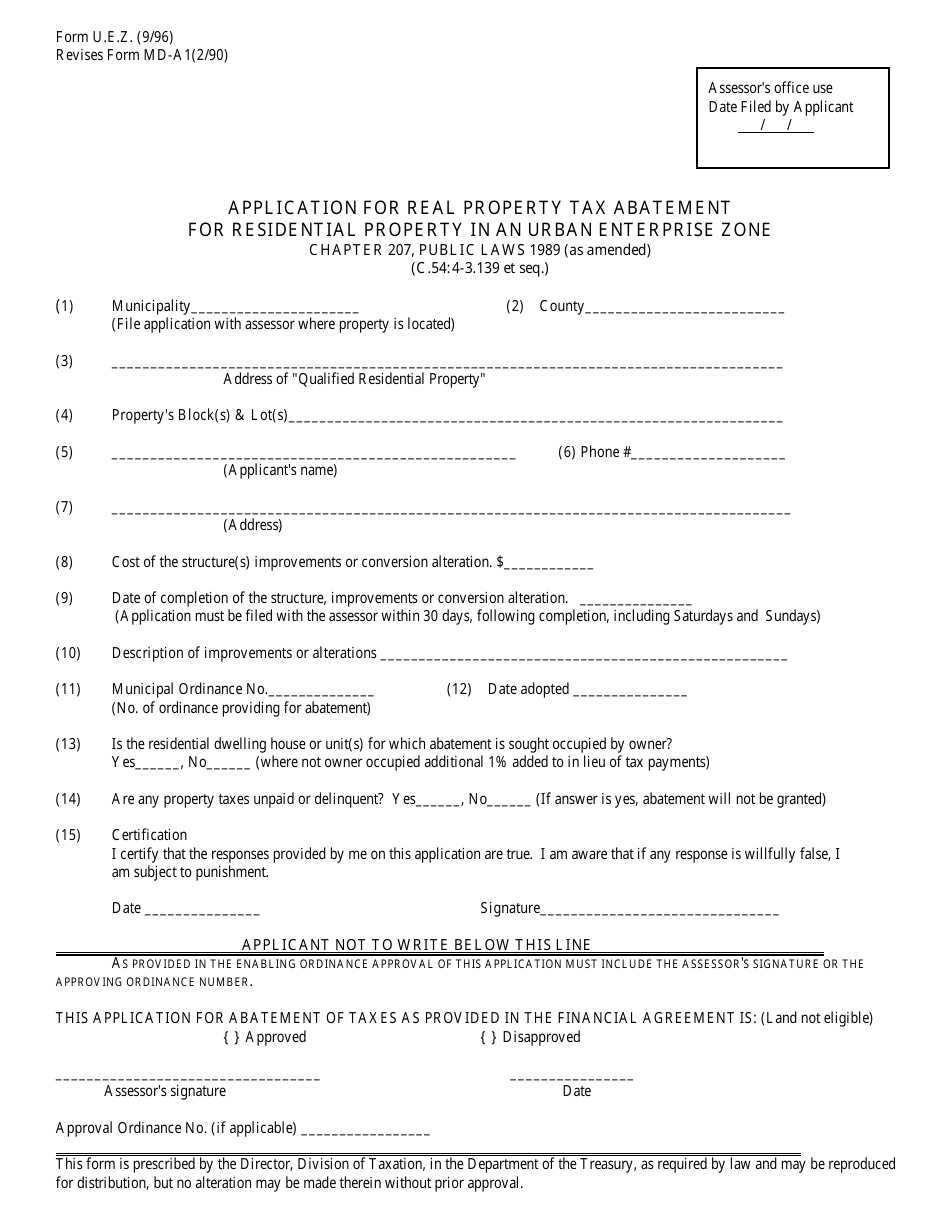

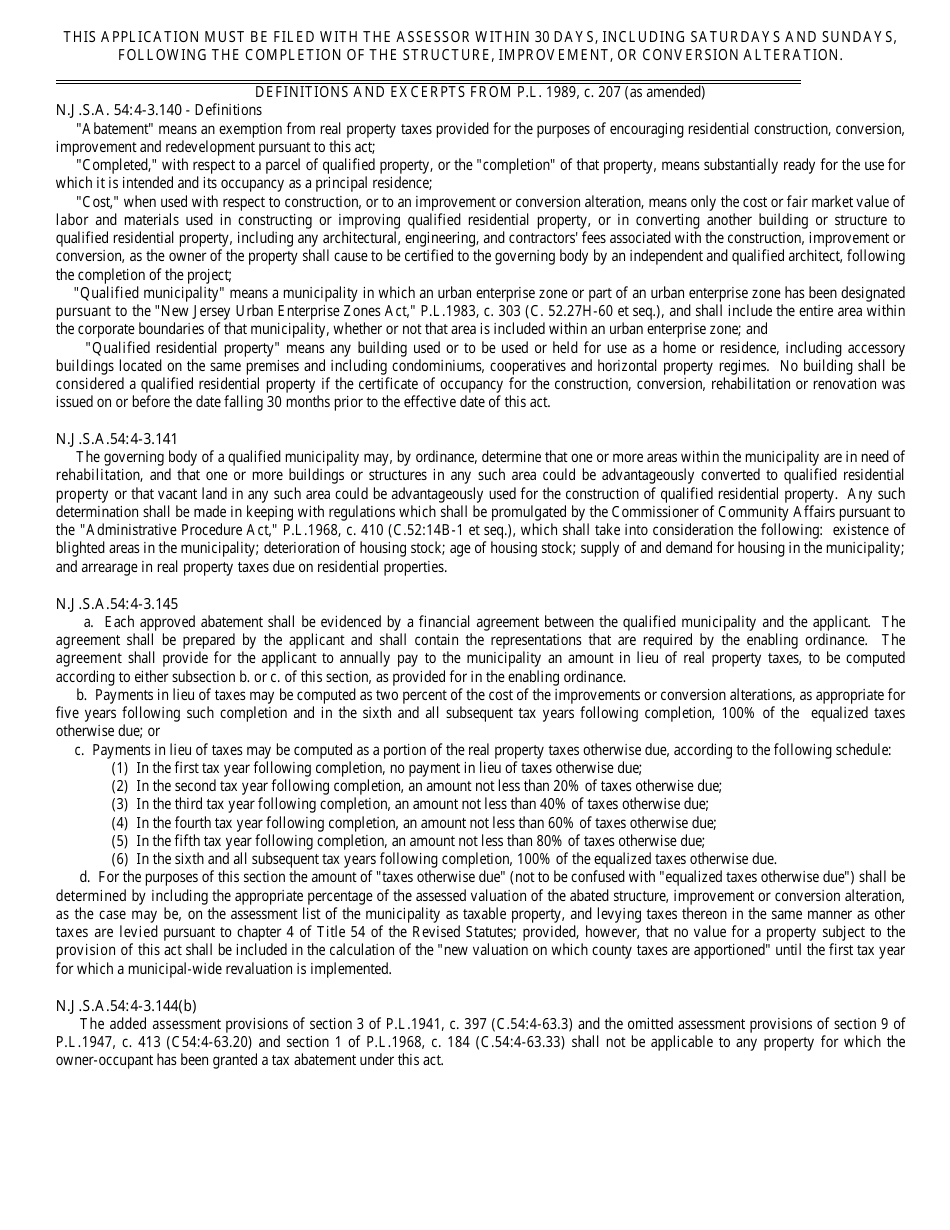

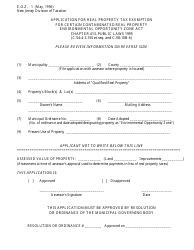

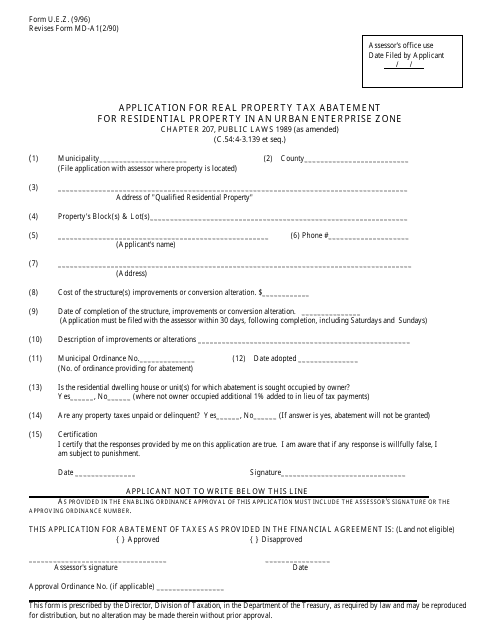

Form U.E.Z. Application for Real Property Tax Abatement for Residential Property in an Urban Enterprise Zone - New Jersey

What Is Form U.E.Z.?

This is a legal form that was released by the New Jersey Department of the Treasury - a government authority operating within New Jersey. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is an Urban Enterprise Zone (UEZ)?

A: An Urban Enterprise Zone is a designated area in New Jersey that promotes economic growth and job creation through tax incentives and other benefits.

Q: What is a Real Property Tax Abatement?

A: A Real Property Tax Abatement is a program that allows eligible property owners in an Urban Enterprise Zone to receive a reduction in property taxes for a specified period of time.

Q: Who is eligible to apply for the U.E.Z. Application for Real Property Tax Abatement?

A: Residential property owners located within an Urban Enterprise Zone in New Jersey are eligible to apply.

Q: What are the benefits of the U.E.Z. Real Property Tax Abatement?

A: The benefits of the U.E.Z. Real Property Tax Abatement include a reduction in property taxes for a specified period of time, which can help make homeownership more affordable.

Q: How do I apply for the U.E.Z. Real Property Tax Abatement?

A: To apply for the U.E.Z. Real Property Tax Abatement, you will need to fill out and submit the U.E.Z. Application for Real Property Tax Abatement form to the appropriate local authority within the designated Urban Enterprise Zone.

Q: Are there any restrictions or requirements for the U.E.Z. Real Property Tax Abatement?

A: Yes, there are certain restrictions and requirements for the U.E.Z. Real Property Tax Abatement, such as income limits, occupancy requirements, and compliance with property maintenance standards.

Form Details:

- Released on September 1, 1996;

- The latest edition provided by the New Jersey Department of the Treasury;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form U.E.Z. by clicking the link below or browse more documents and templates provided by the New Jersey Department of the Treasury.

Download Form U.E.Z. Application for Real Property Tax Abatement for Residential Property in an Urban Enterprise Zone - New Jersey

1

2