![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 709

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 709

for the current year.

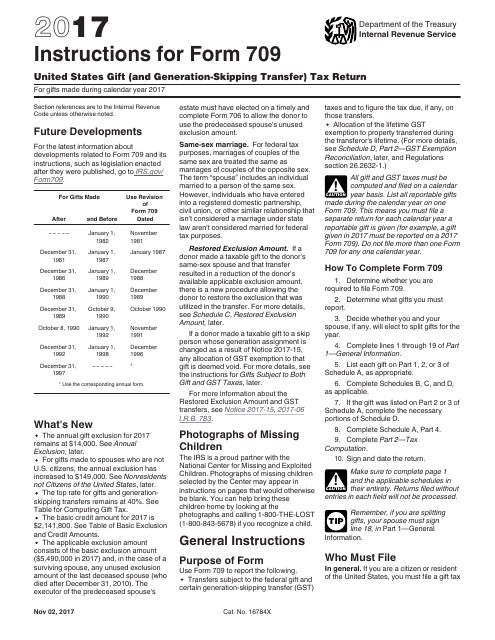

Instructions for IRS Form 709 United States Gift (And Generation-Skipping Transfer) Tax Return

This document contains official instructions for IRS Form 709 , United States Gift (And Generation-Skipping Transfer) Tax Return - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury.

FAQ

Q: What is IRS Form 709?

A: IRS Form 709 is the United States Gift (And Generation-Skipping Transfer) Tax Return.

Q: Who needs to file IRS Form 709?

A: You need to file IRS Form 709 if you made gifts exceeding the annual exclusion amount or if you're subject to the generation-skipping transfer (GST) tax.

Q: What is the purpose of IRS Form 709?

A: The purpose of IRS Form 709 is to report and calculate any gift taxes or generation-skipping transfer taxes that may be due.

Q: What gifts need to be reported on IRS Form 709?

A: Gifts that need to be reported on IRS Form 709 include cash, property, or any transfer of assets, made during the year.

Q: Is there a deadline for filing IRS Form 709?

A: Yes, the deadline for filing IRS Form 709 is April 15th of the year following the year in which the gift was made.

Q: What happens if I don't file IRS Form 709?

A: If you're required to file IRS Form 709 and fail to do so, you may face penalties and interest on any unpaid gift or generation-skipping transfer taxes.

Q: Are there any exemptions or exclusions for gifts on IRS Form 709?

A: Yes, there are annual exclusion amounts and various exemptions that may apply to reduce or eliminate gift taxes.

Q: Can I file IRS Form 709 electronically?

A: Yes, you can file IRS Form 709 electronically using the e-file system provided by the IRS.

Q: Do I need to keep a copy of IRS Form 709 for my records?

A: Yes, it's recommended to keep a copy of IRS Form 709 and any supporting documentation for at least three years after the filing date.

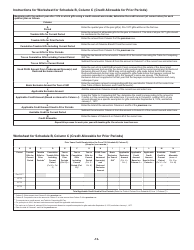

Instruction Details:

- This 20-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 709 United States Gift (And Generation-Skipping Transfer) Tax Return

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20