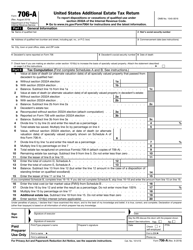

![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 706-A

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 706-A

for the current year.

Instructions for IRS Form 706-A United States Additional Estate Tax Return

This document contains official instructions for IRS Form 706-A , United States Additional Estate Tax Return - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury.

FAQ

Q: What is IRS Form 706-A?

A: IRS Form 706-A is the United States Additional Estate Tax Return.

Q: Who needs to file IRS Form 706-A?

A: Those who are required to pay additional estate tax in the United States may need to file Form 706-A.

Q: When should IRS Form 706-A be filed?

A: Form 706-A should be filed within 9 months after the decedent's date of death.

Q: What is the purpose of filing IRS Form 706-A?

A: The purpose of filing Form 706-A is to calculate and pay any additional estate tax owed to the United States government.

Q: What information is required on IRS Form 706-A?

A: Form 706-A requires information such as the decedent's personal and financial details, the value of the estate, and any other relevant information related to the additional estate tax.

Q: Are there any penalties for not filing IRS Form 706-A?

A: Yes, failure to file Form 706-A or pay the additional estate tax on time may result in penalties and interest being assessed by the IRS.

Q: Is professional assistance required to complete IRS Form 706-A?

A: While it is not required, seeking professional assistance from a tax advisor or estate planning attorney may be beneficial in ensuring accurate and timely completion of Form 706-A.

Instruction Details:

- This 5-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5