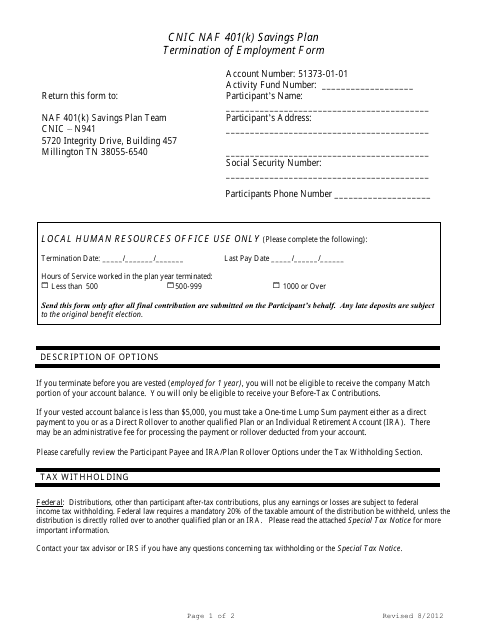

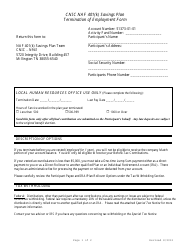

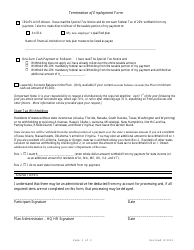

Cnic NAF 401(K) Savings Plan - Termination of Employment Form

Cnic NAF 401(K) Savings Plan - Termination of Employment Form is a 8-page legal document that was released by the U.S. Department of the Navy on August 1, 2012 and used nation-wide.

FAQ

Q: What is the CNIC NAF 401(K) Savings Plan?

A: The CNIC NAF 401(K) Savings Plan is a retirement savings plan for civilian employees of the Department of Defense.

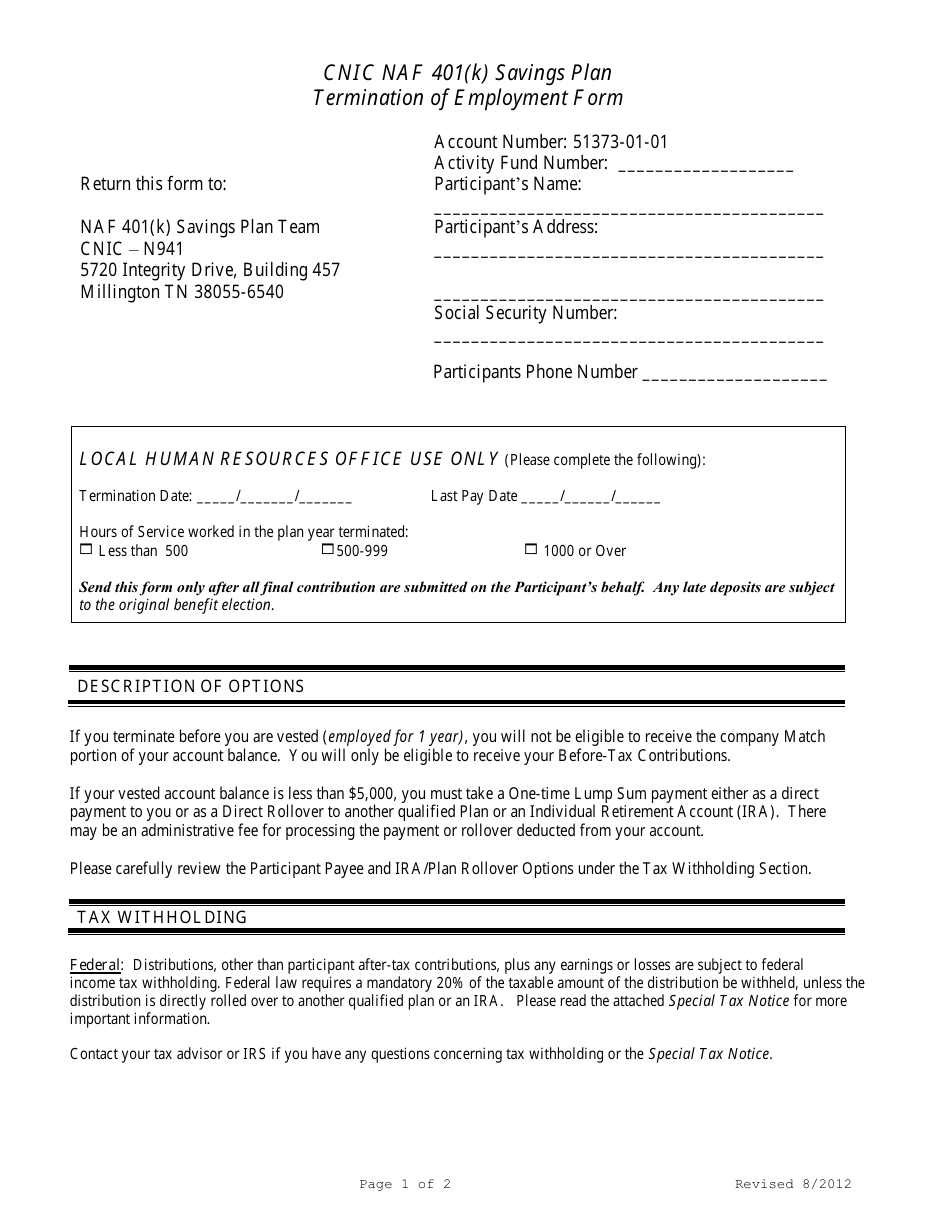

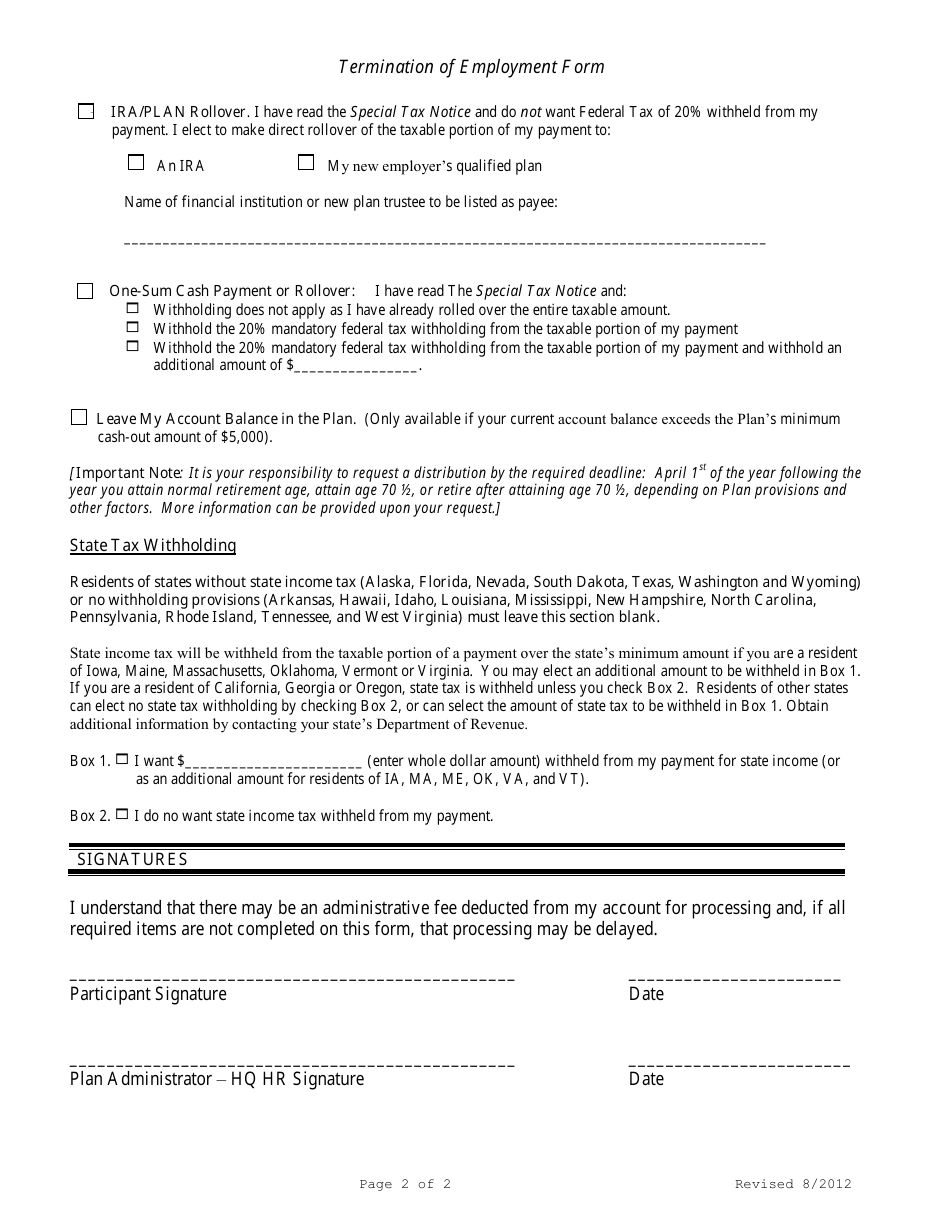

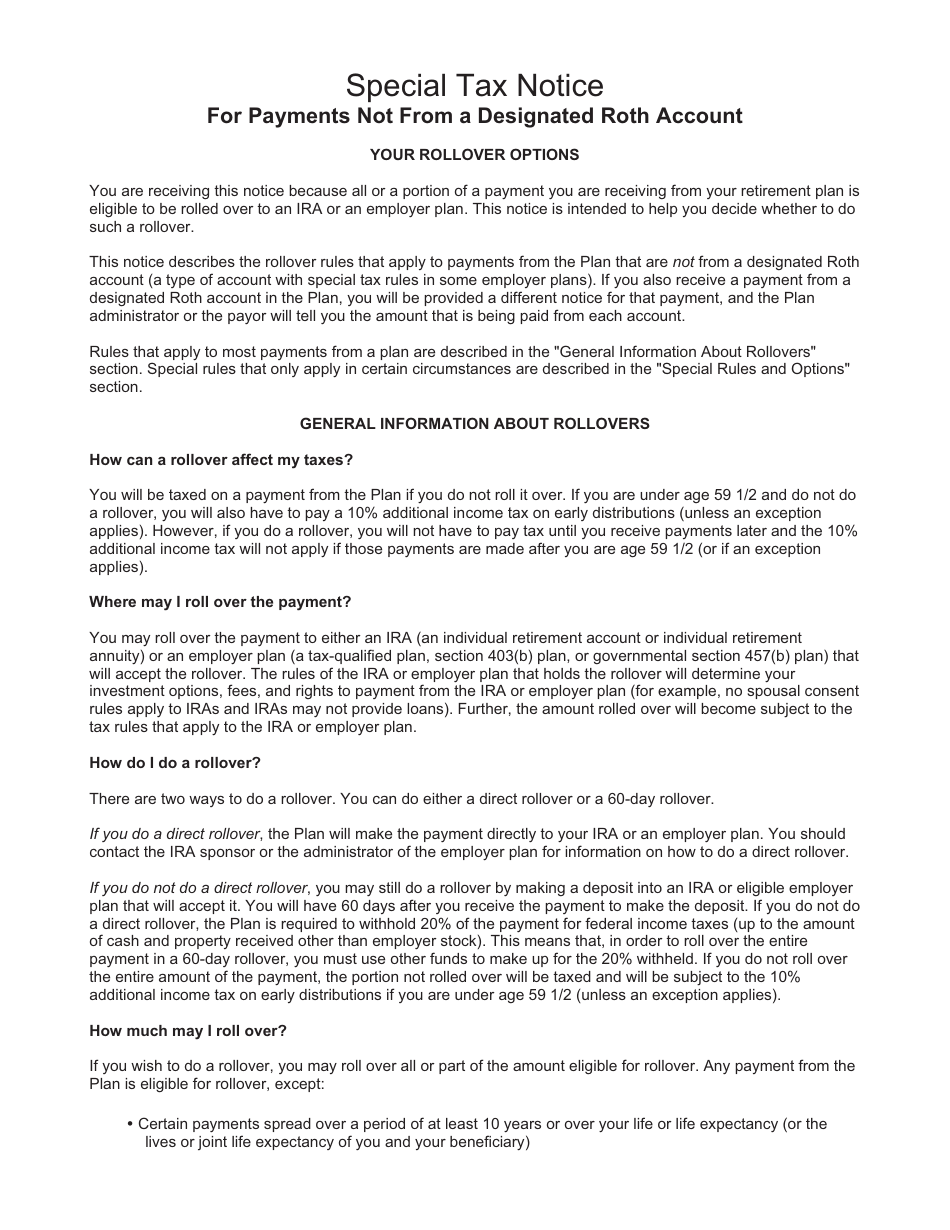

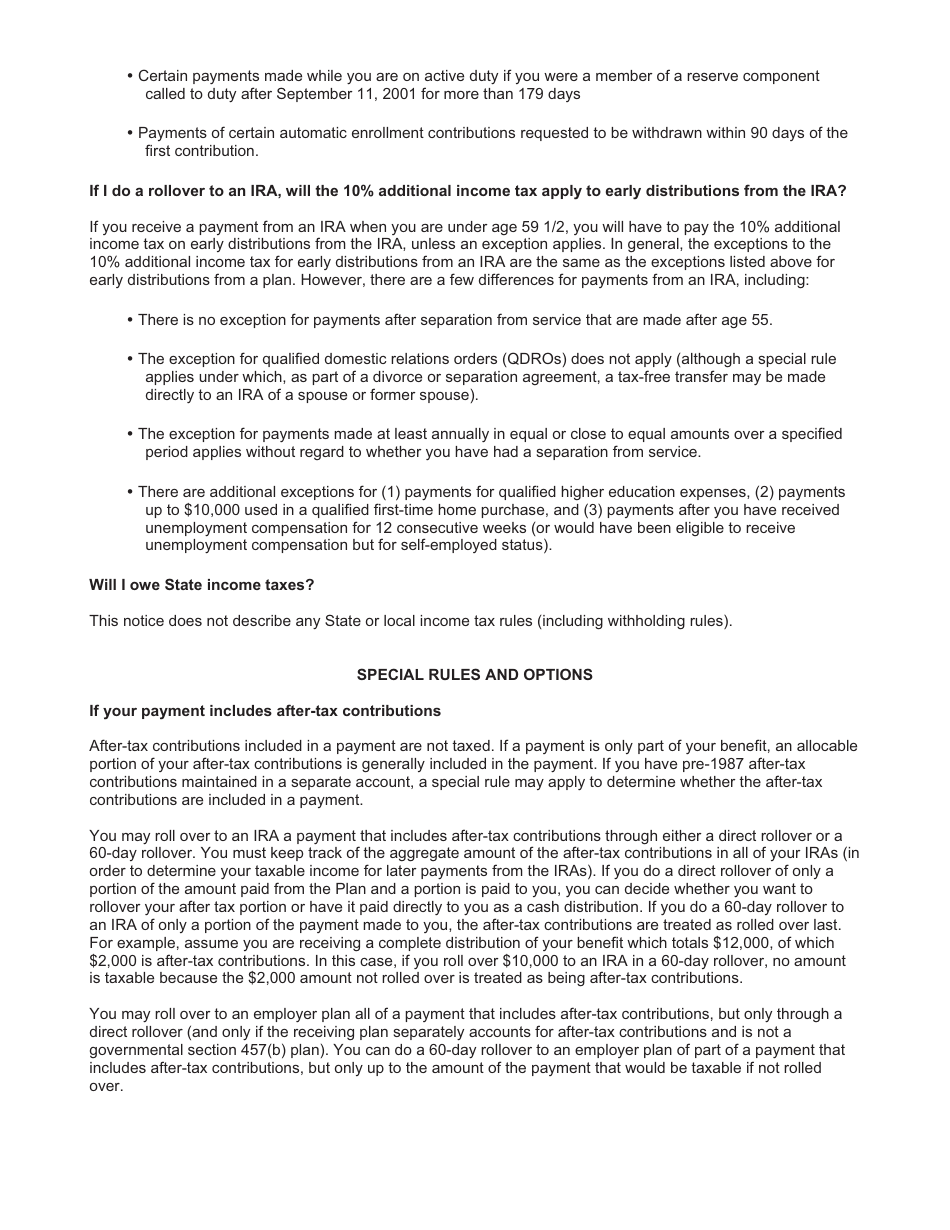

Q: What is the Termination of Employment Form?

A: The Termination of Employment Form is a form used to notify the plan administrator when an employee is leaving their job.

Q: Why do I need to fill out the Termination of Employment Form?

A: Filling out the Termination of Employment Form ensures that your retirement savings are properly handled when you leave your job.

Q: What information do I need to provide on the Termination of Employment Form?

A: You will need to provide personal information, such as your name, social security number, and contact information, as well as details about your employment termination.

Form Details:

- The latest edition currently provided by the U.S. Department of the Navy;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of the form by clicking the link below or browse more legal forms and templates provided by the issuing department.

Download Cnic NAF 401(K) Savings Plan - Termination of Employment Form

1

2

3

4

5

6

7

8