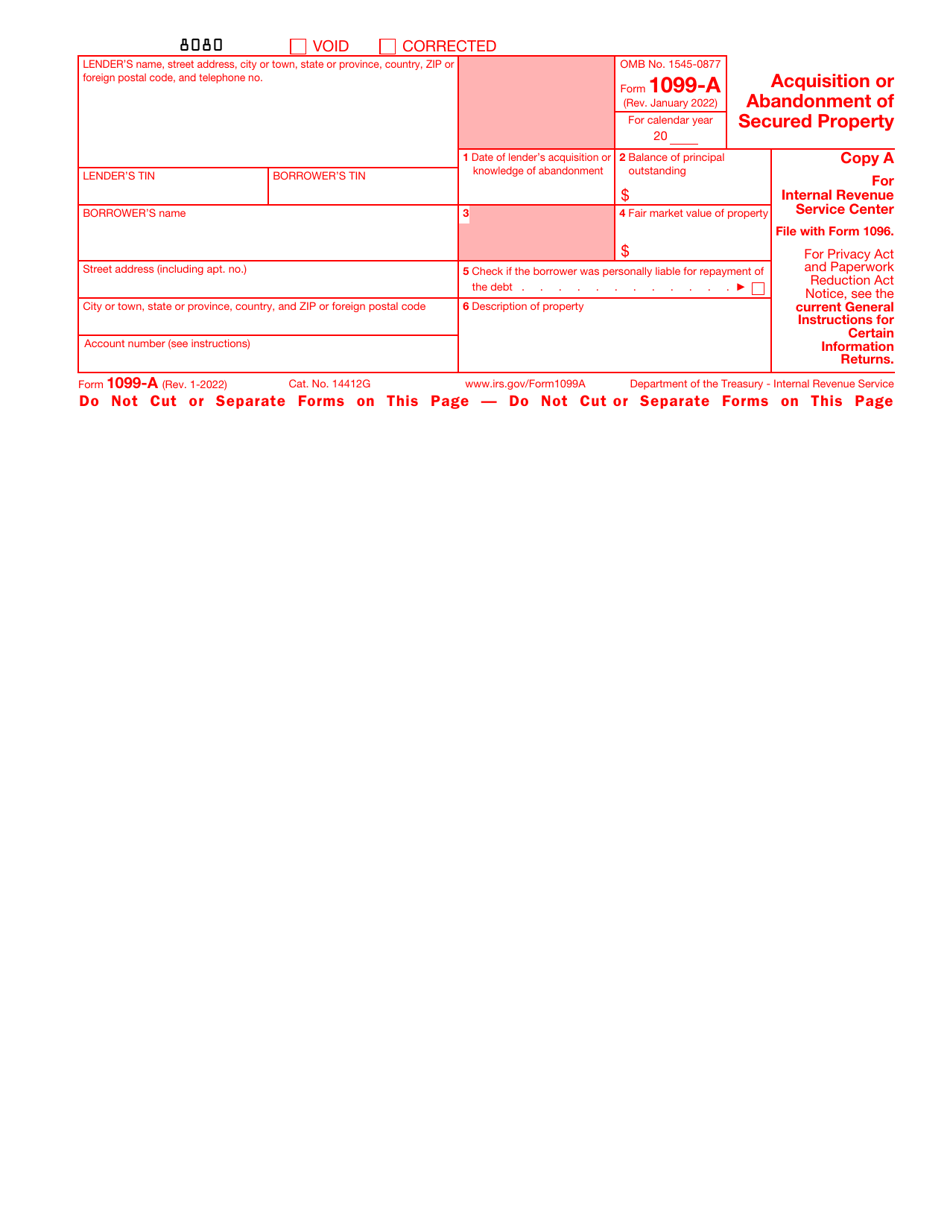

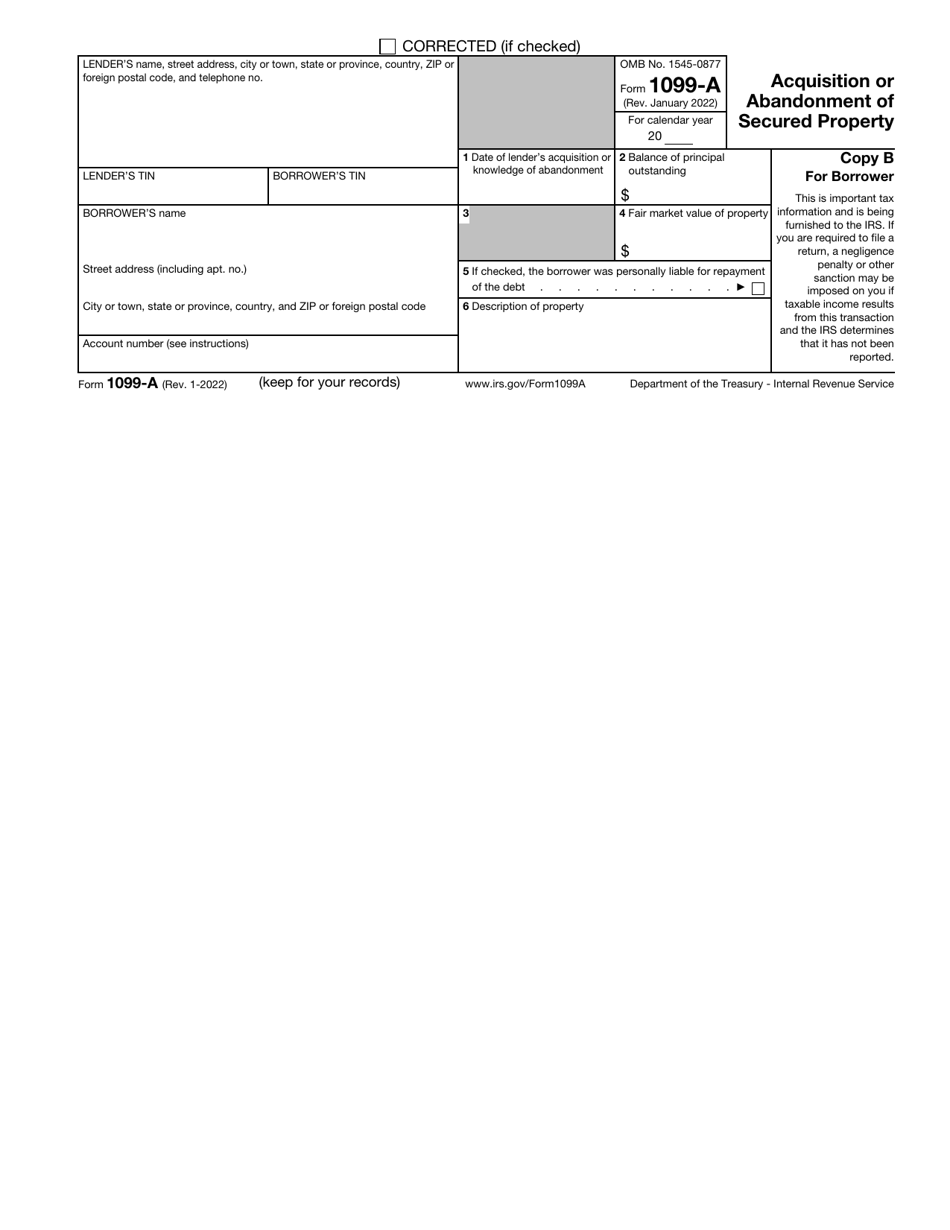

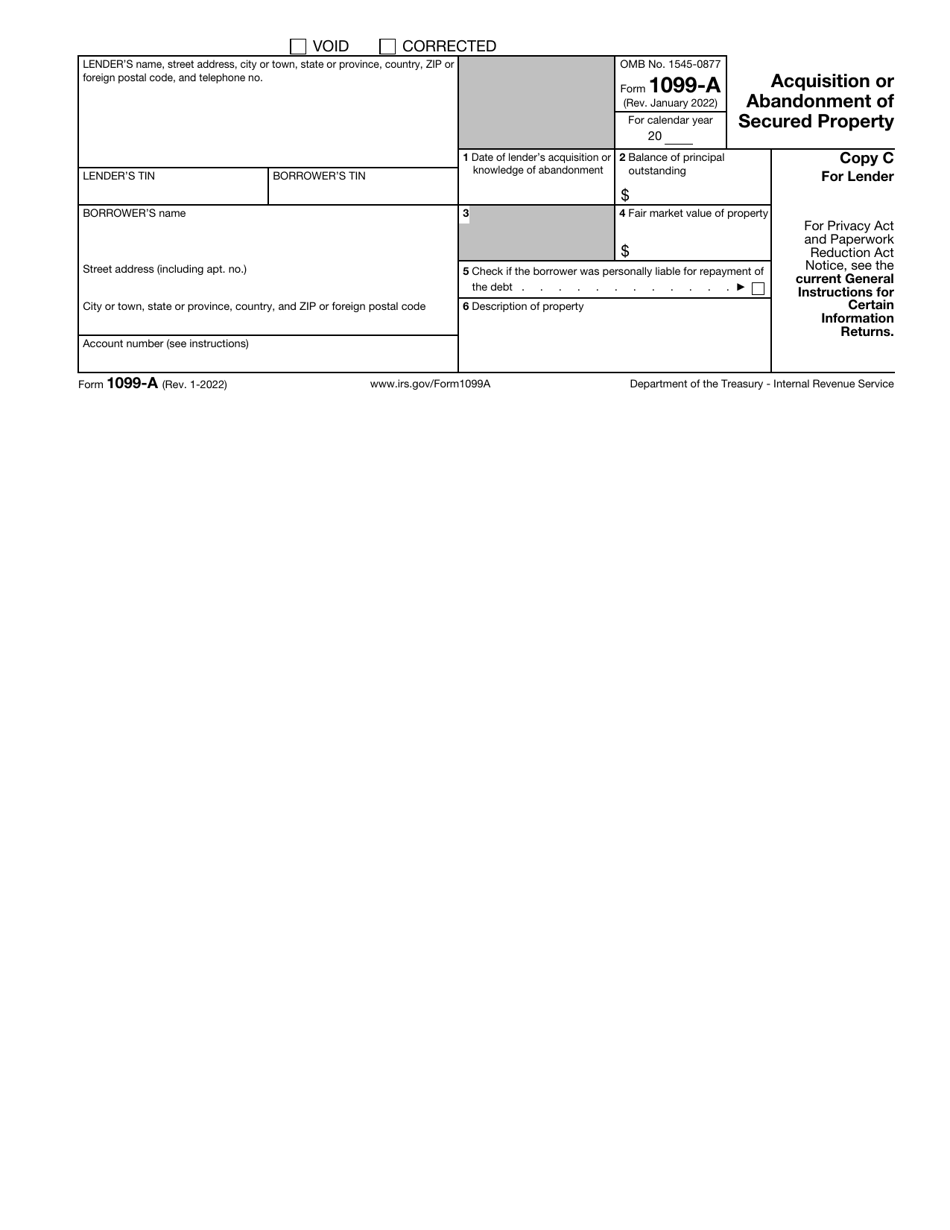

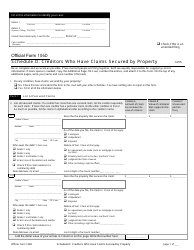

IRS Form 1099-A Acquisition or Abandonment of Secured Property

What Is IRS Form 1099-A?

IRS Form 1099-A, Acquisition or Abandonment of Secured Property , is a formal document that outlines the details of a property foreclosure.

Alternate Name:

- Tax Form 1099-A.

Many mortgage lenders are obliged to prepare this statement to inform taxpayers about the specifics of the transaction, annulment of the mortgage or a portion of it, or a sale of the real estate below the market value.

This instrument was issued by the Internal Revenue Service (IRS) on January 1, 2022 , rendering older editions obsolete. You can download an IRS Form 1099-A fillable version through the link below.

Check out the 1099 Series of forms to see more IRS documents in this series.

What Is a 1099-A Form Used For?

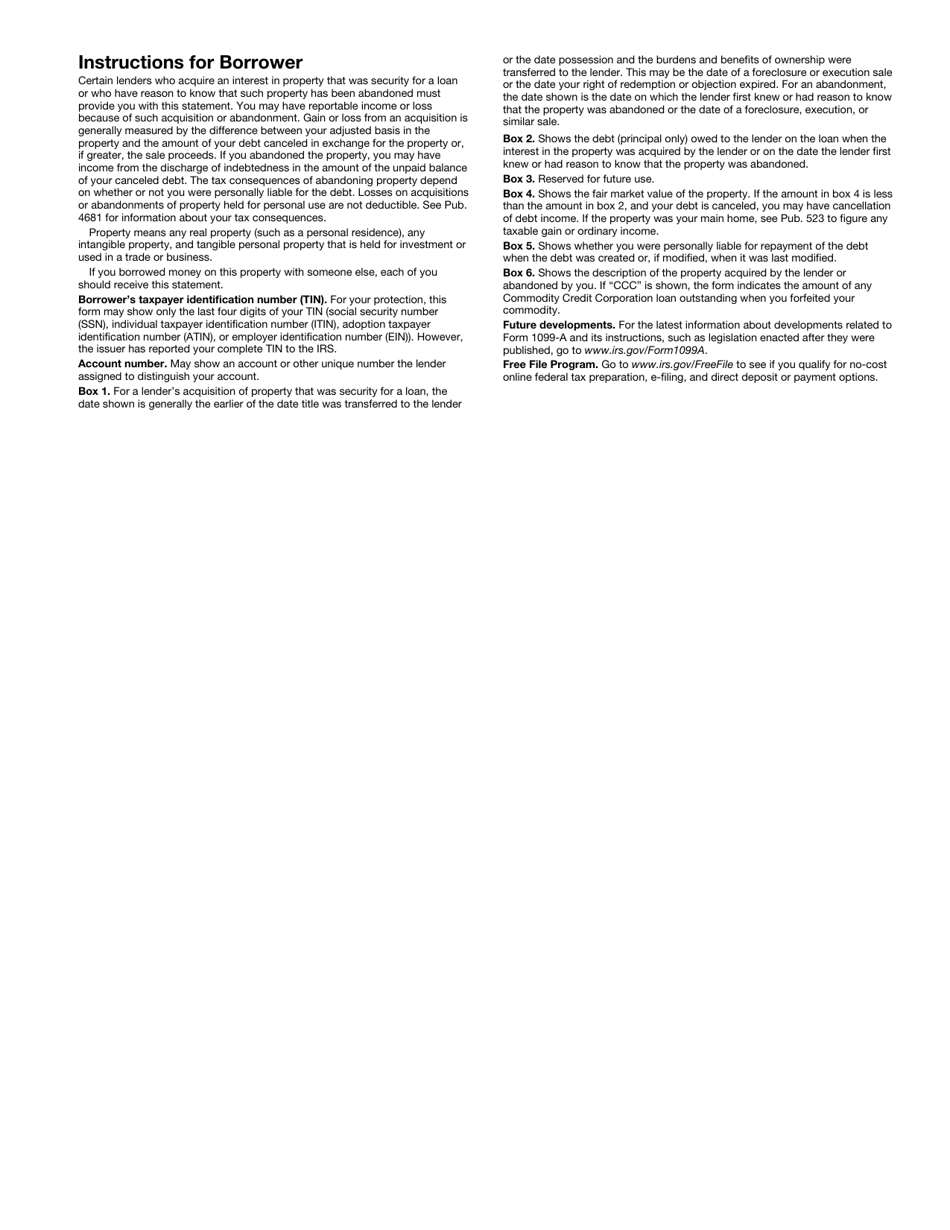

Lenders have to file a 1099-A Tax Form for every transfer that involves abandoned or foreclosed real estate. During the year after the year when you obtained an interest in the property or discovered that it was abandoned, you have to inform the tax authorities about the real estate being sold or transferred by February 28.

Note that if the borrower does not receive this form from their lender, bank, or another financial institution by January 31, they are strongly advised to request this form so that they have all the details about their tax activities. If you notice an error in the paperwork, contact the lender to get a modified statement and have the accurate figures for the IRS.

What Is the Difference Between a 1099-A and 1099-C?

IRS Form 1099-C, Cancellation of Debt, is prepared by financial entities and sent to taxpayers and the IRS in case the taxpayer's debt of $600 or more was forgiven or canceled. The taxpayer that receives this instrument from their creditor or lender has to replicate the details from the form on their main income statement to make sure the fiscal authorities are aware of all the taxable income they got during the year - the canceled debt reported may reduce the amount of the tax refund you are entitled to receive.

Many taxpayers receive both Form 1099-A and Form 1099-C - you will find them together in your mailbox if your lender made a decision to cancel the rest of the mortgage debt after the foreclosure occurred. For example, if the amount you borrowed was $90.000 and you were able to repay $60.000, there is a balance of $30.000 remaining - the latter number will be included on the 1099-C Form in case the lender comes to a conclusion that you cannot deal with the remaining debt. It is also likely you will receive a copy of the form if you reach a debt settlement with another lender.

Form 1099-A Instructions

Follow the Form 1099-A Instructions to elaborate on the acquisition of the secured property or to describe how the borrower discarded the real estate they previously used:

-

Specify the tax year described in the form . Write down the full name, correspondence address, telephone number, and taxpayer identification number of the lender. Identify the borrower by their name and mailing address. In many instances, the lender opens numerous accounts for the same borrower which is why it is crucial to point out the number of the particular account to prevent possible confusion.

-

Indicate the date the lender got the property in question . Usually, it is the date the title transfer is finalized or the date when all the ownership privileges and burdens are considered the responsibility of the lender. Alternatively, you need to state the date when you first knew the property had been abandoned.

-

Record the balance of the current debt - the number must reflect the situation at the moment when the interest was acquired or the day when you first learned the property was abandoned. You may not cover foreclosure expenses or accumulated interest when providing this number.

-

Enter the accurate market value of the property in case you are outlining an execution, foreclosure, or a sale of that sort . Customarily, the bid price of the foreclosure is regarded to be the right number; you may also state the estimated value of the real estate. Check the appropriate box if the borrower had personal liability with respect to the debt repayment when the debt was created or altered.

-

Describe the real estate. It is enough to give a brief summary - ensure you write down the legal address of the property that typically serves as a formal description. It is also permitted to include other specifics such as a block or lot that facilitate the identification of the real estate.

-

Make sure you prepare several copies of the form - one of them goes to the IRS, the other must be given to the borrower, and the third one is supposed to remain in your records so that you can always use it for reference.

Download IRS Form 1099-A Acquisition or Abandonment of Secured Property

1

2

3

4

5

6