Instructions for Form DR-309634 Local Government User of Diesel Fuel Tax Return - Florida

This document contains official instructions for Form DR-309634 , Local Government User of Diesel Fuel Tax Return - a form released and collected by the Florida Department of Revenue. An up-to-date fillable Form DR-309634 is available for download through this link.

Instruction Details:

- This 4-page document is available for download in PDF;

- Might not be applicable for the current year. Choose an older version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Florida Department of Revenue.

Download Instructions for Form DR-309634 Local Government User of Diesel Fuel Tax Return - Florida

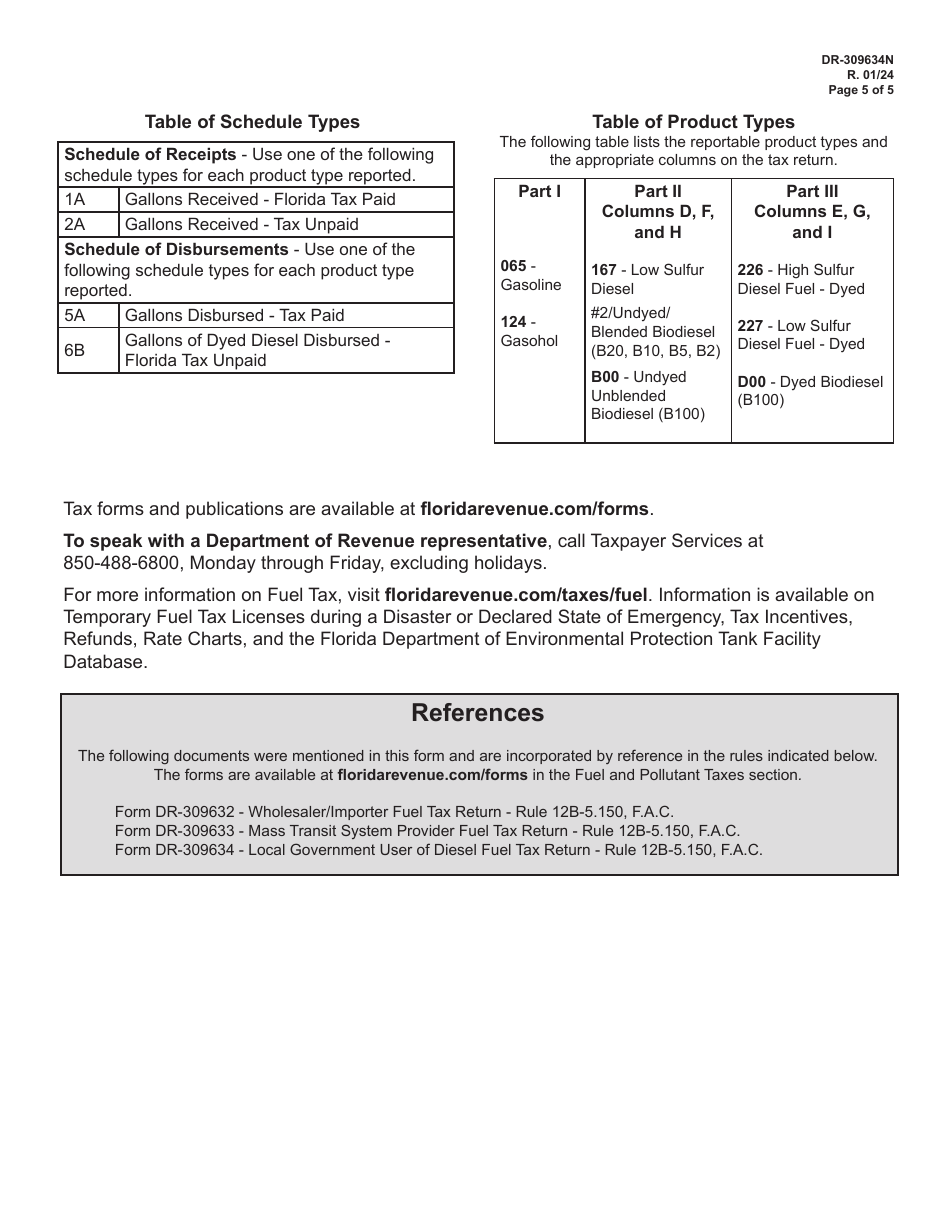

1

2

3

4

5