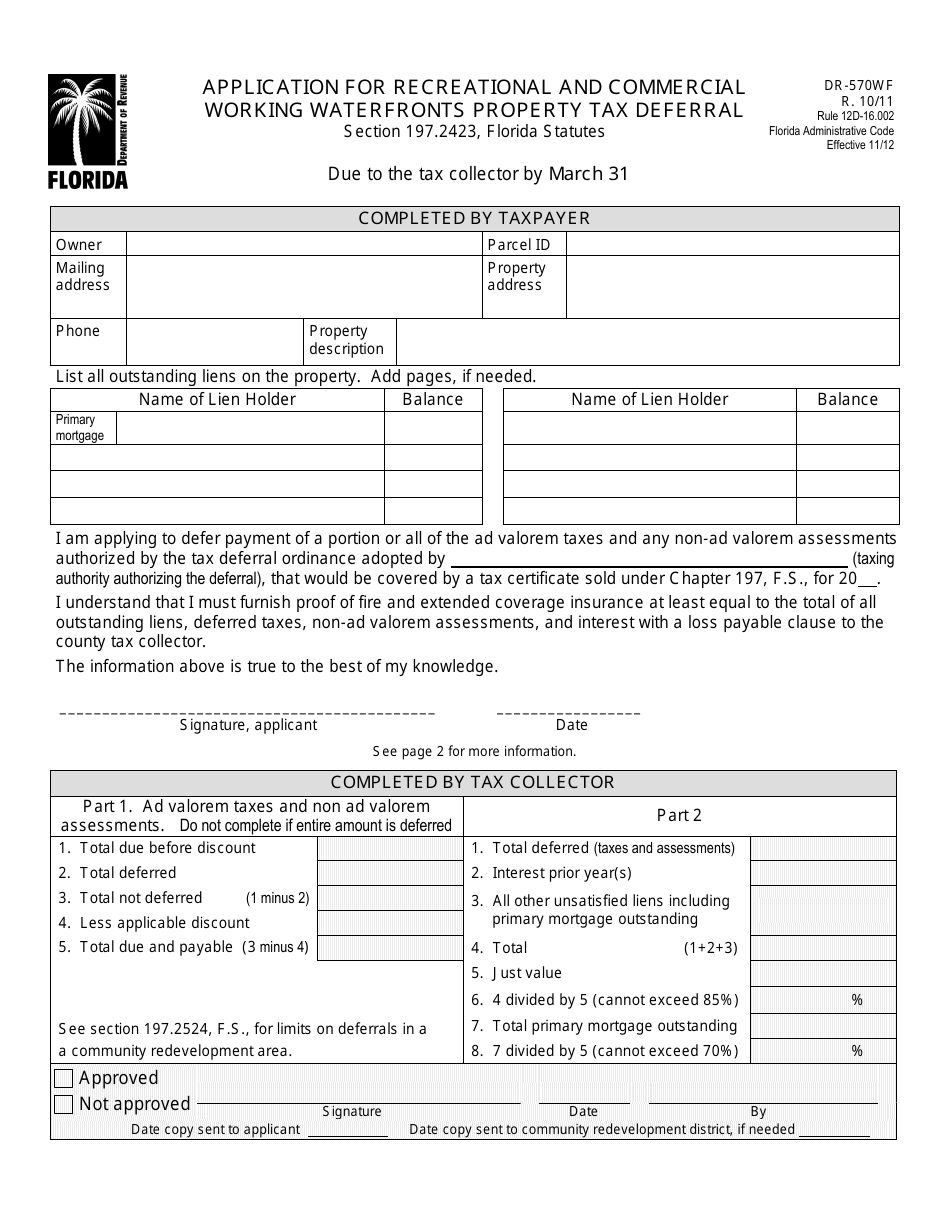

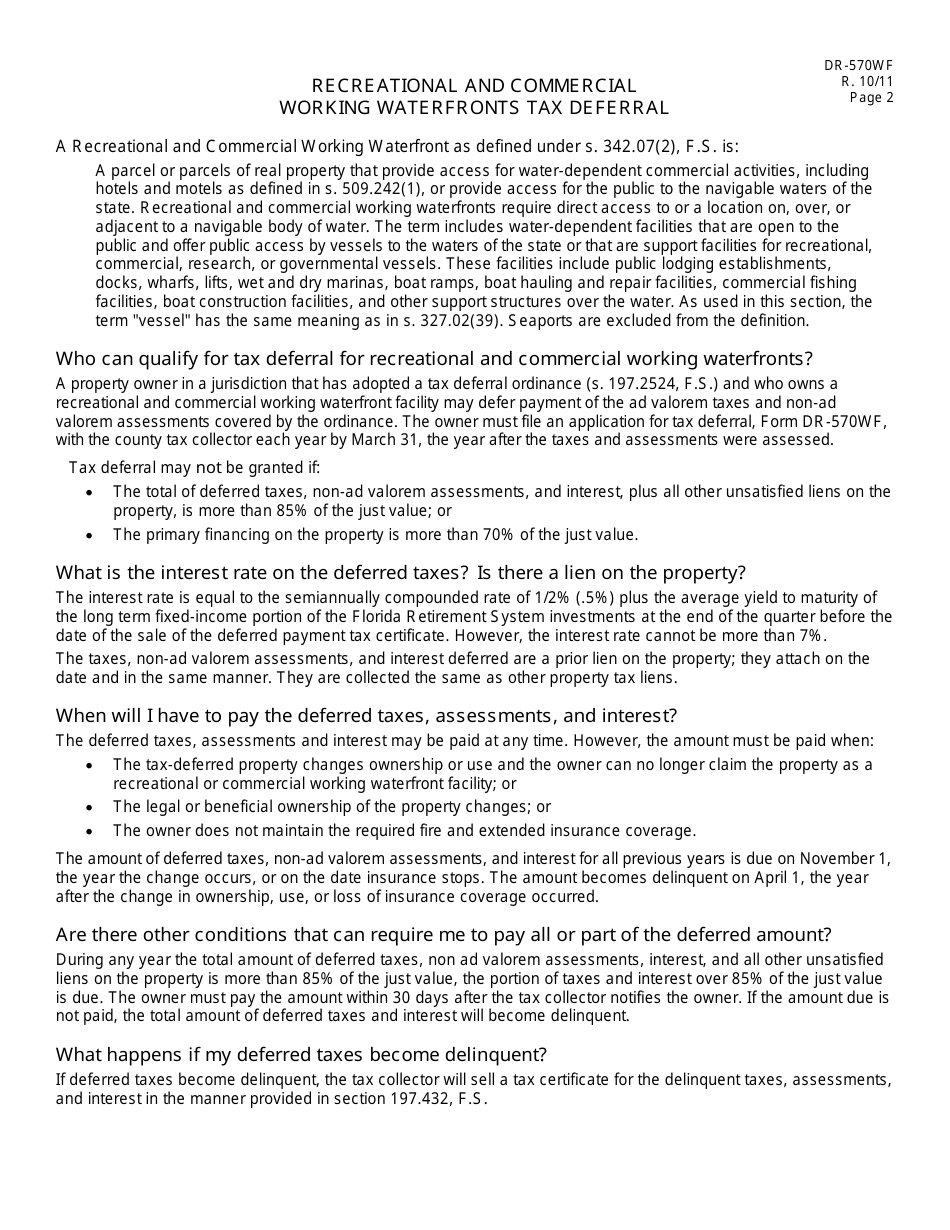

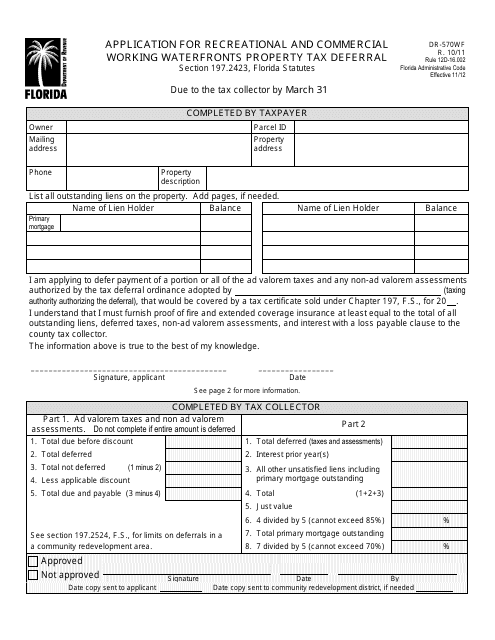

Form DR-570WF Application for Recreational and Commercial Working Waterfronts Property Tax Deferral - Florida

What Is Form DR-570WF?

This is a legal form that was released by the Florida Department of Revenue - a government authority operating within Florida. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form DR-570WF?

A: Form DR-570WF is an application for property tax deferral for recreational and commercial working waterfronts in Florida.

Q: Who can use Form DR-570WF?

A: Property owners who own recreational or commercial working waterfronts in Florida can use Form DR-570WF.

Q: What is the purpose of Form DR-570WF?

A: The purpose of Form DR-570WF is to apply for property tax deferral for recreational and commercial working waterfronts.

Q: Is there a deadline to submit Form DR-570WF?

A: Yes, Form DR-570WF must be submitted to the county property appraiser's office by March 1st of each year.

Q: What are the eligibility requirements for property tax deferral?

A: To be eligible for property tax deferral, the property must meet certain criteria, such as being used for certain commercial or recreational activities.

Q: Are there any limitations to property tax deferral?

A: Yes, there are limitations to property tax deferral, such as the deferral amount cannot exceed a certain percentage of the property's just value.

Q: What happens if my application for property tax deferral is approved?

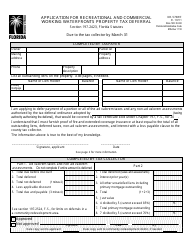

A: If your application is approved, you will be granted a deferral of property taxes for a specified period of time.

Q: What happens if my application for property tax deferral is denied?

A: If your application is denied, you will be responsible for paying your property taxes as usual.

Q: Can I appeal if my application for property tax deferral is denied?

A: Yes, you have the right to appeal the denial of your application for property tax deferral.

Form Details:

- Released on October 1, 2011;

- The latest edition provided by the Florida Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form DR-570WF by clicking the link below or browse more documents and templates provided by the Florida Department of Revenue.

Download Form DR-570WF Application for Recreational and Commercial Working Waterfronts Property Tax Deferral - Florida

1

2