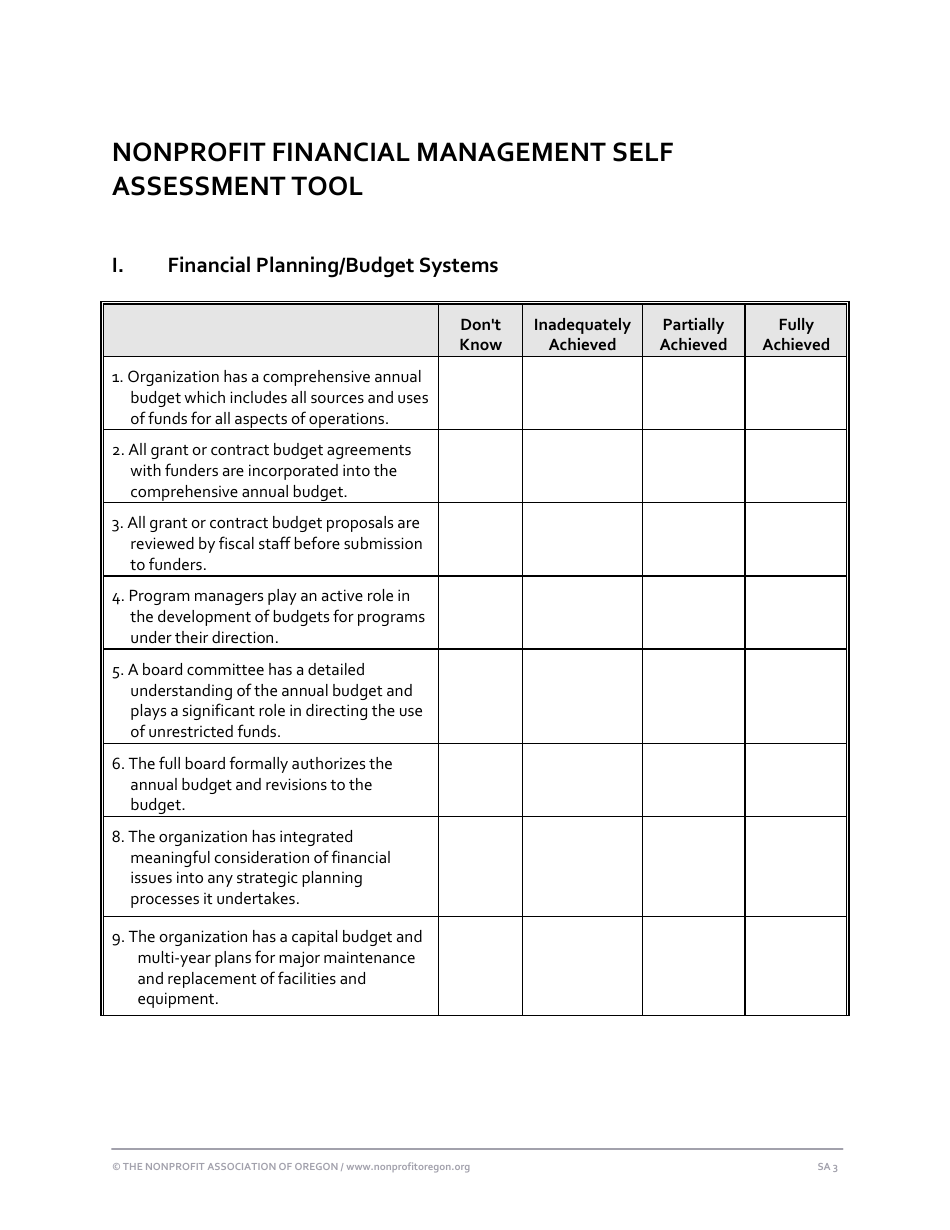

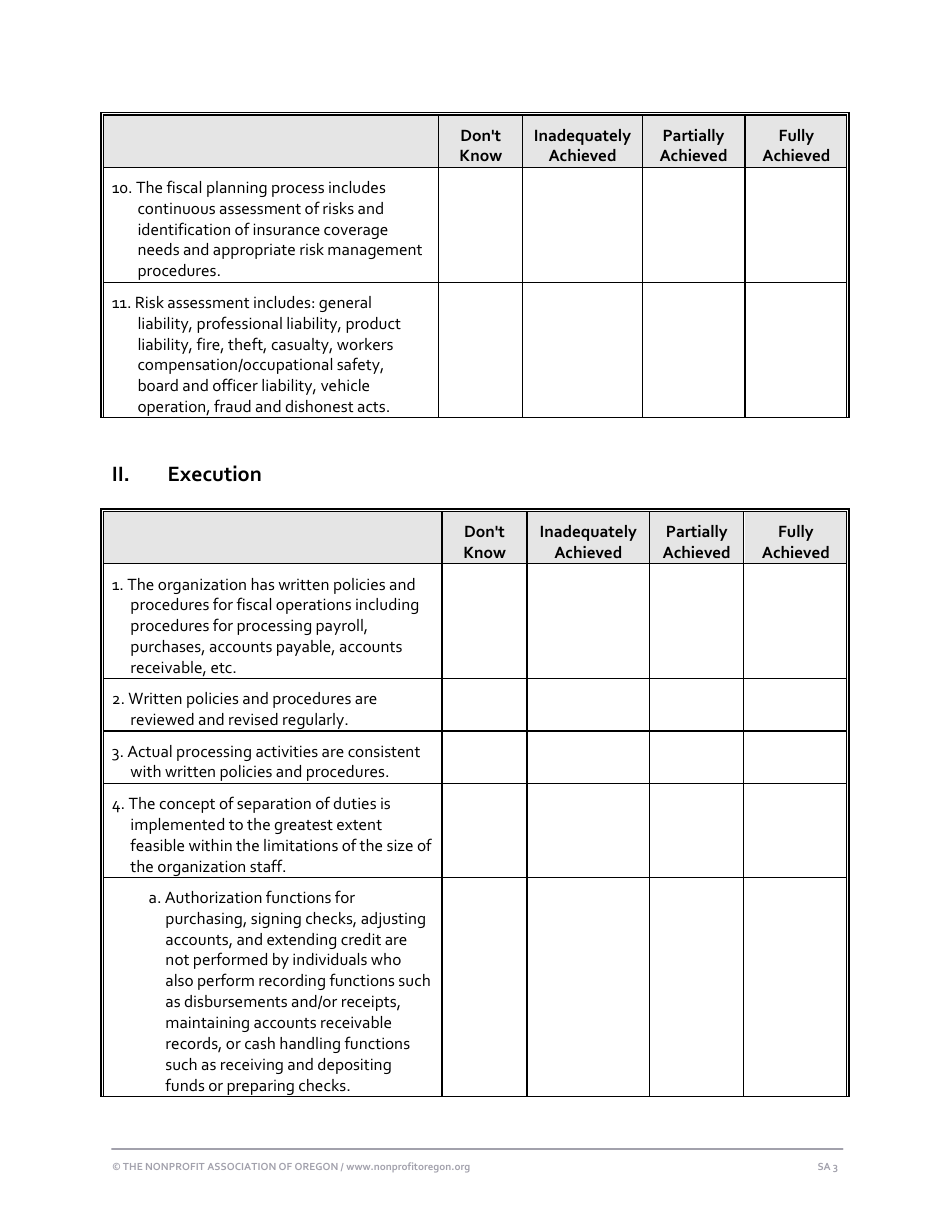

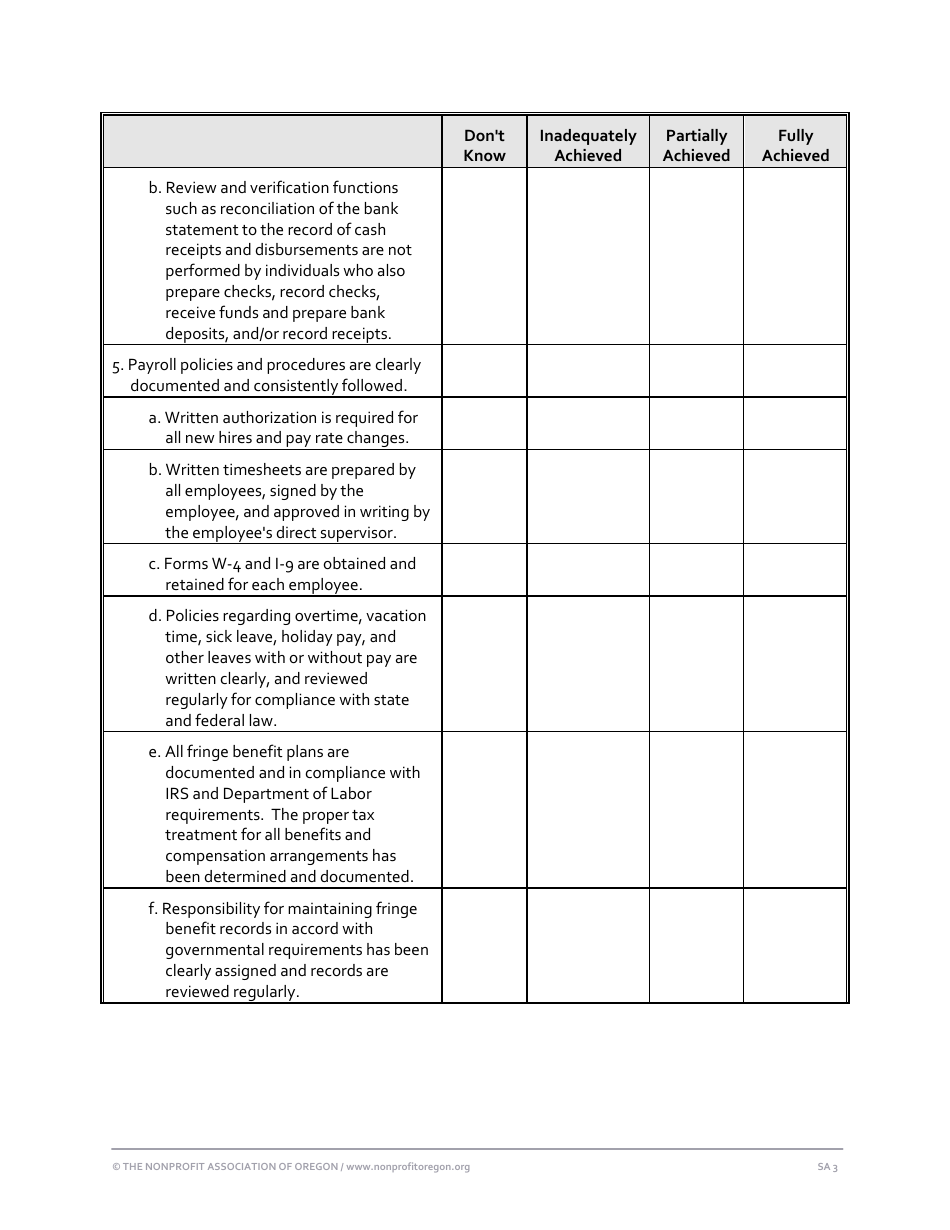

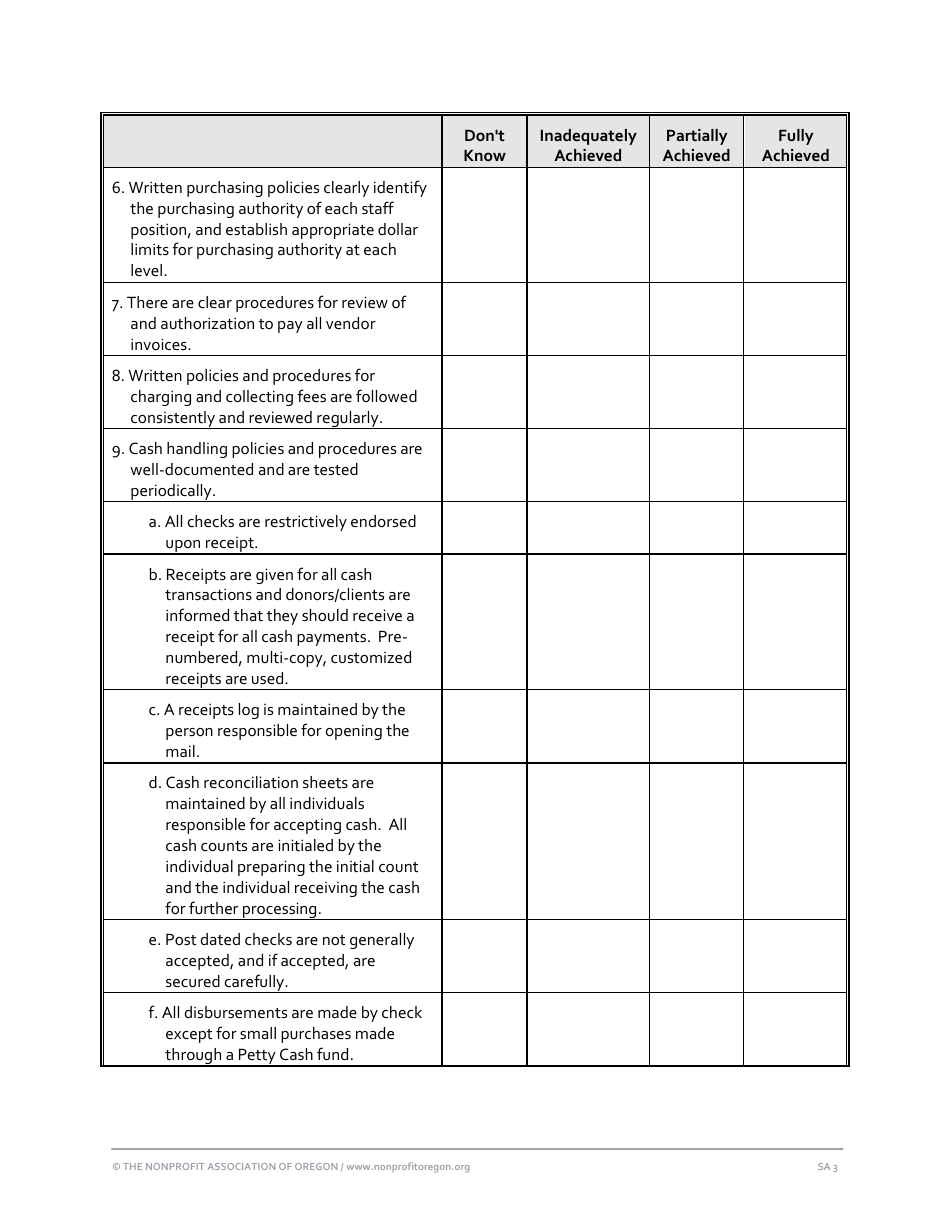

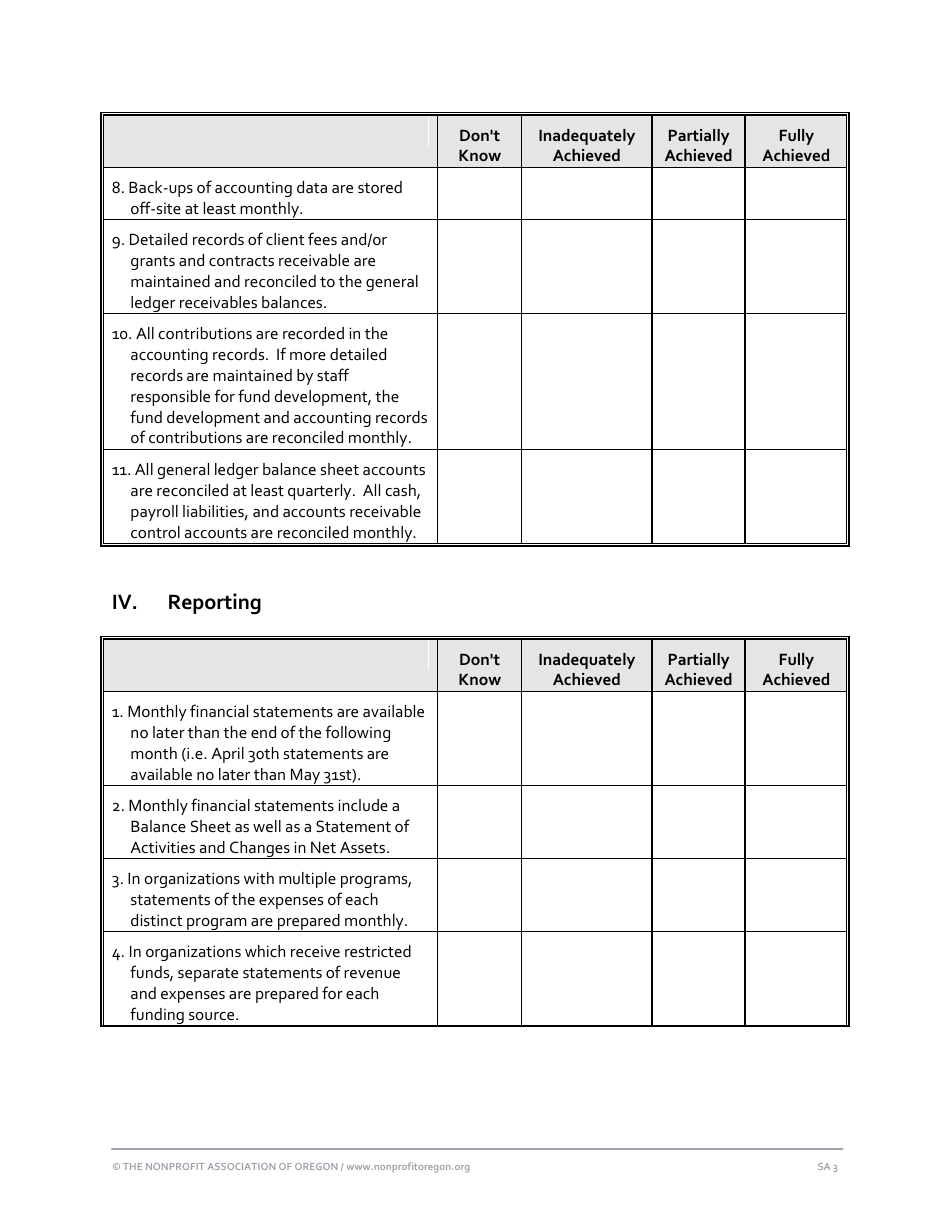

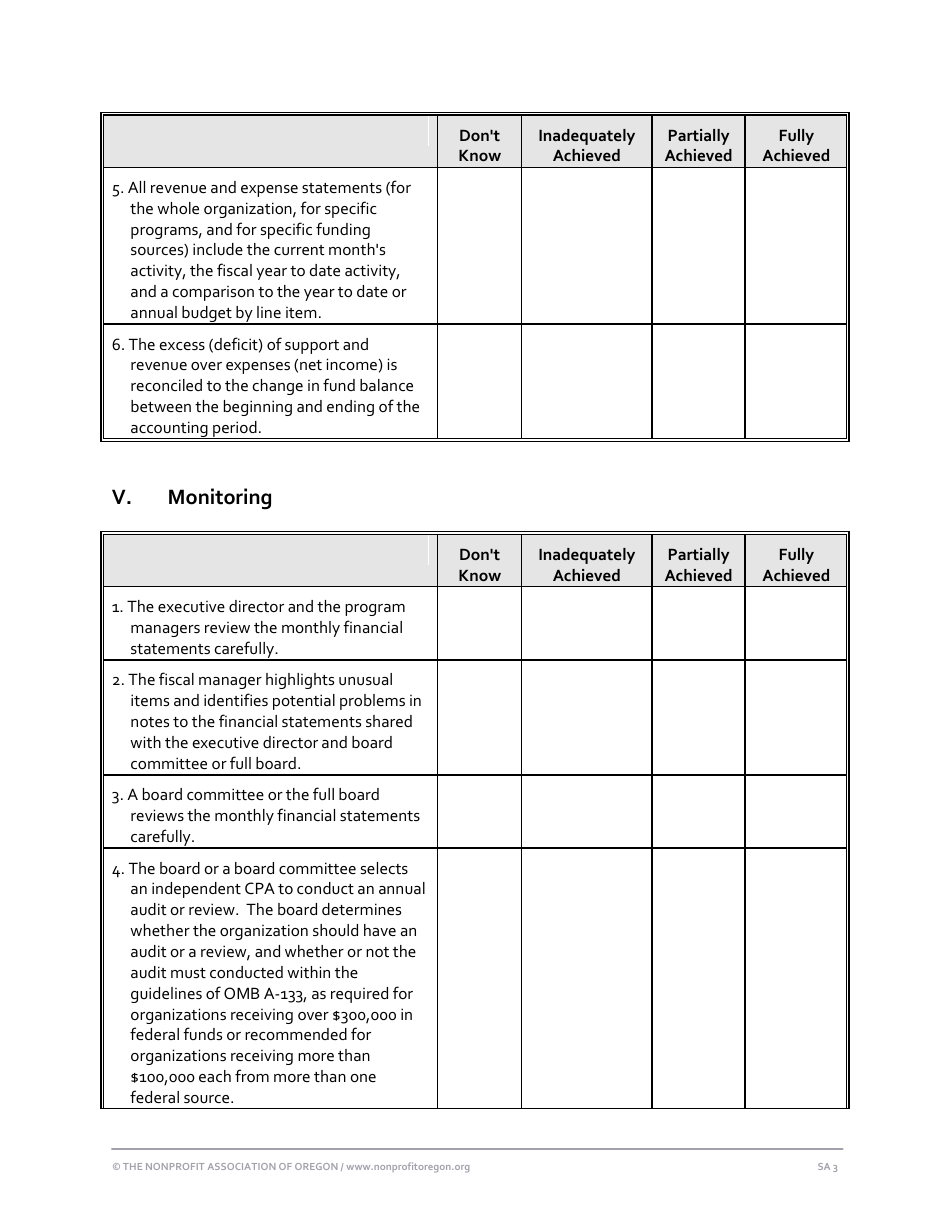

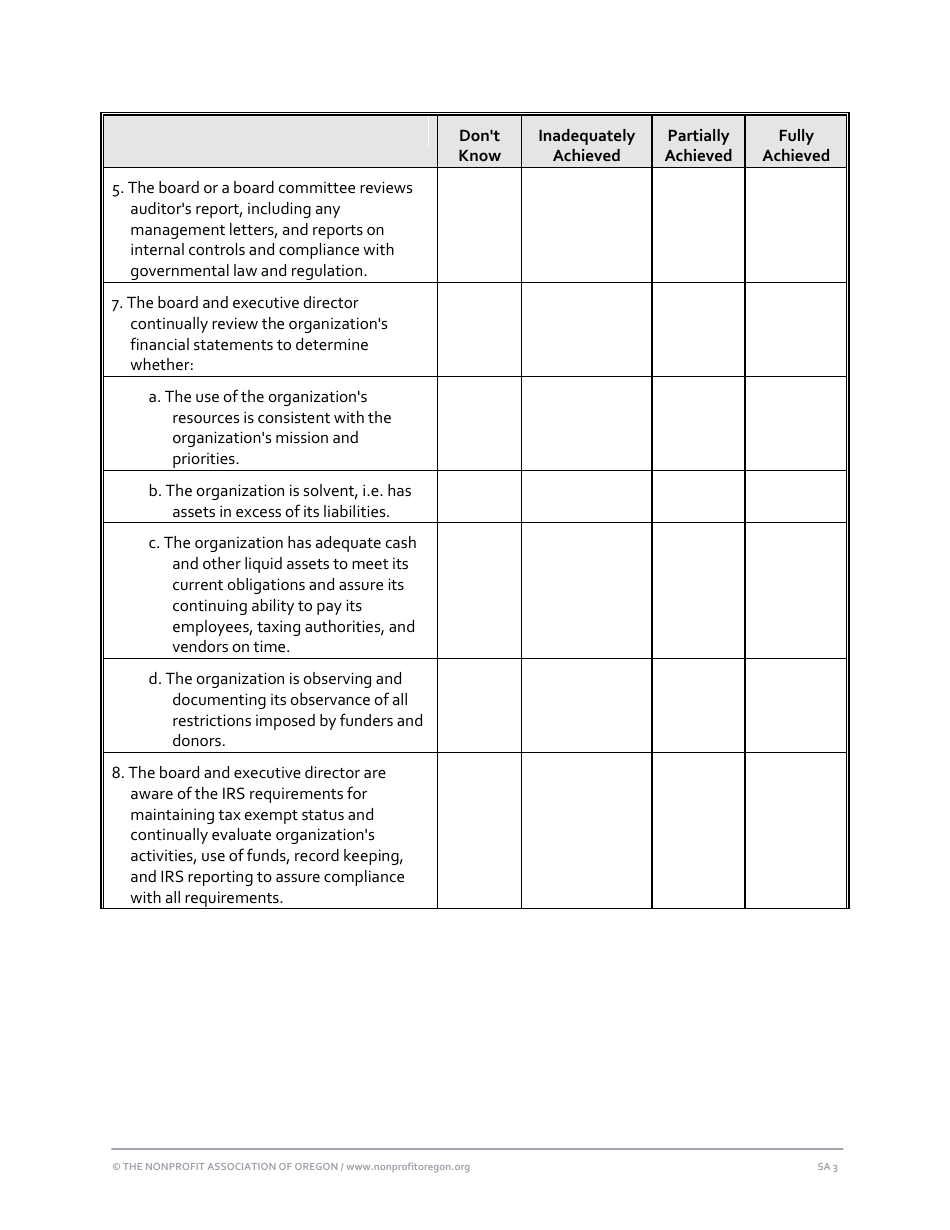

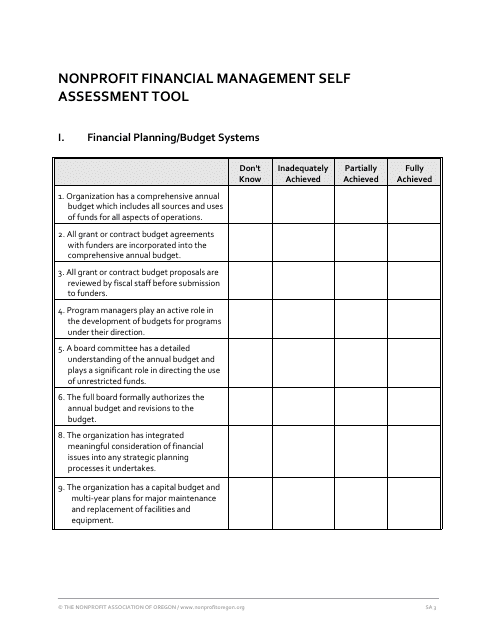

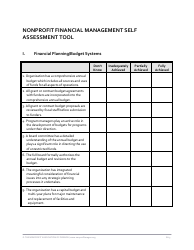

Nonprofit Financial Management Self Assessment Form

The Nonprofit Financial Management Self Assessment Form is used to evaluate and assess the financial management practices and performance of a nonprofit organization. It helps identify areas for improvement and develop strategies to enhance financial stability and effectiveness.

The Nonprofit Financial Management Self Assessment Form is typically filed by nonprofit organizations themselves. It is a tool for these organizations to evaluate and assess their financial management practices.

FAQ

Q: What is a nonprofit?

A: A nonprofit is an organization that operates for a social, educational, or charitable purpose, rather than for profit.

Q: What is financial management?

A: Financial management refers to the processes and strategies used by an organization to manage its financial resources effectively.

Q: Why is financial management important for nonprofits?

A: Financial management is important for nonprofits to ensure financial stability, make informed decisions, and fulfill their mission.

Q: What is a self-assessment form?

A: A self-assessment form is a tool that allows individuals or organizations to evaluate their own performance or capabilities.

Q: Why should nonprofits conduct self-assessments?

A: Nonprofits should conduct self-assessments to identify strengths, weaknesses, and areas for improvement in their financial management practices.

Q: What are some areas covered in a nonprofit financial management self-assessment form?

A: A nonprofit financial management self-assessment form may cover areas such as budgeting, financial reporting, internal controls, and risk management.

Q: How can nonprofits use the self-assessment form results?

A: Nonprofits can use the self-assessment form results to develop action plans, prioritize improvements, and enhance their financial management practices.

Q: Are self-assessment results confidential?

A: The confidentiality of self-assessment results may vary depending on the organization's policies and the purpose of the assessment.

Download Nonprofit Financial Management Self Assessment Form

1

2

3

4

5

6

7

8