![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-4P

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-4P

for the current year.

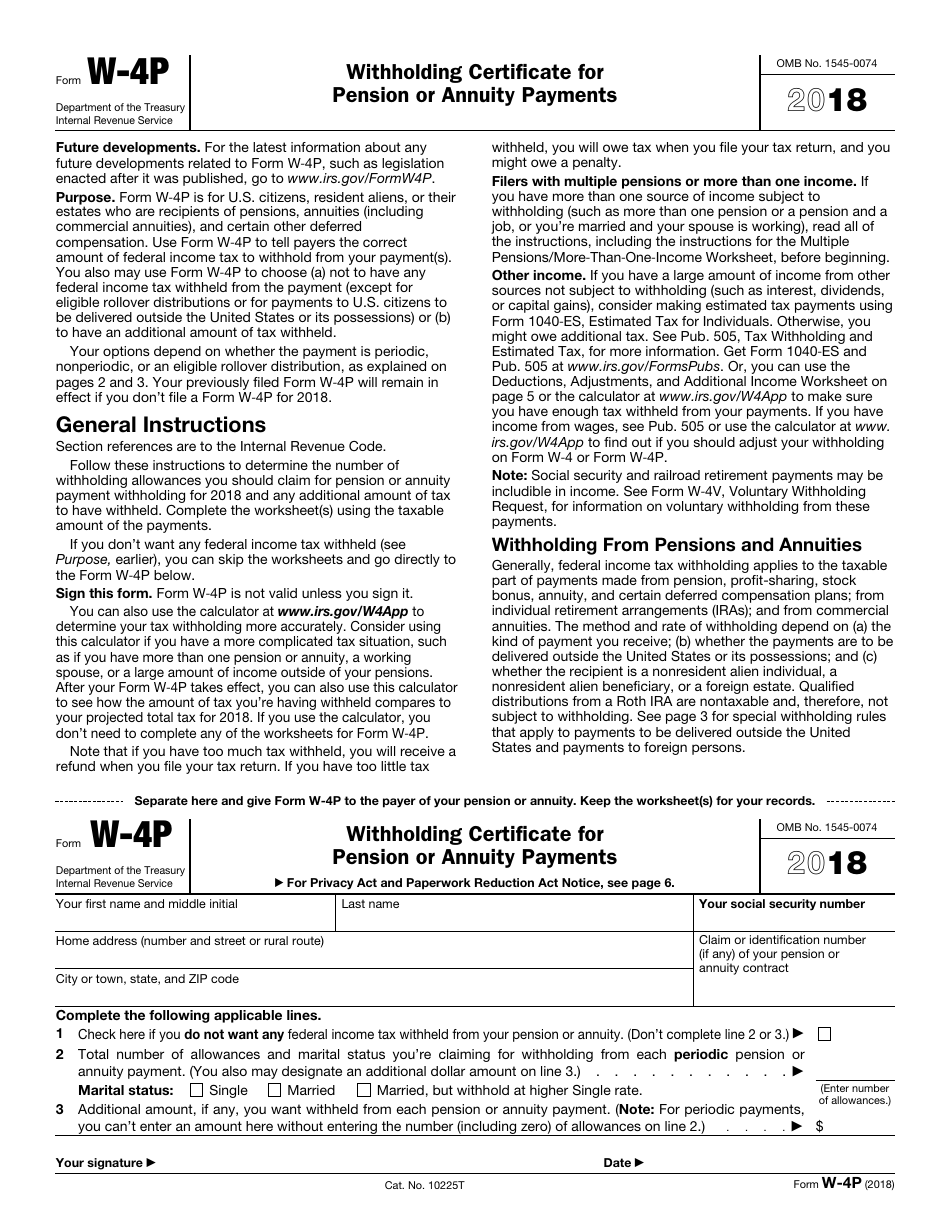

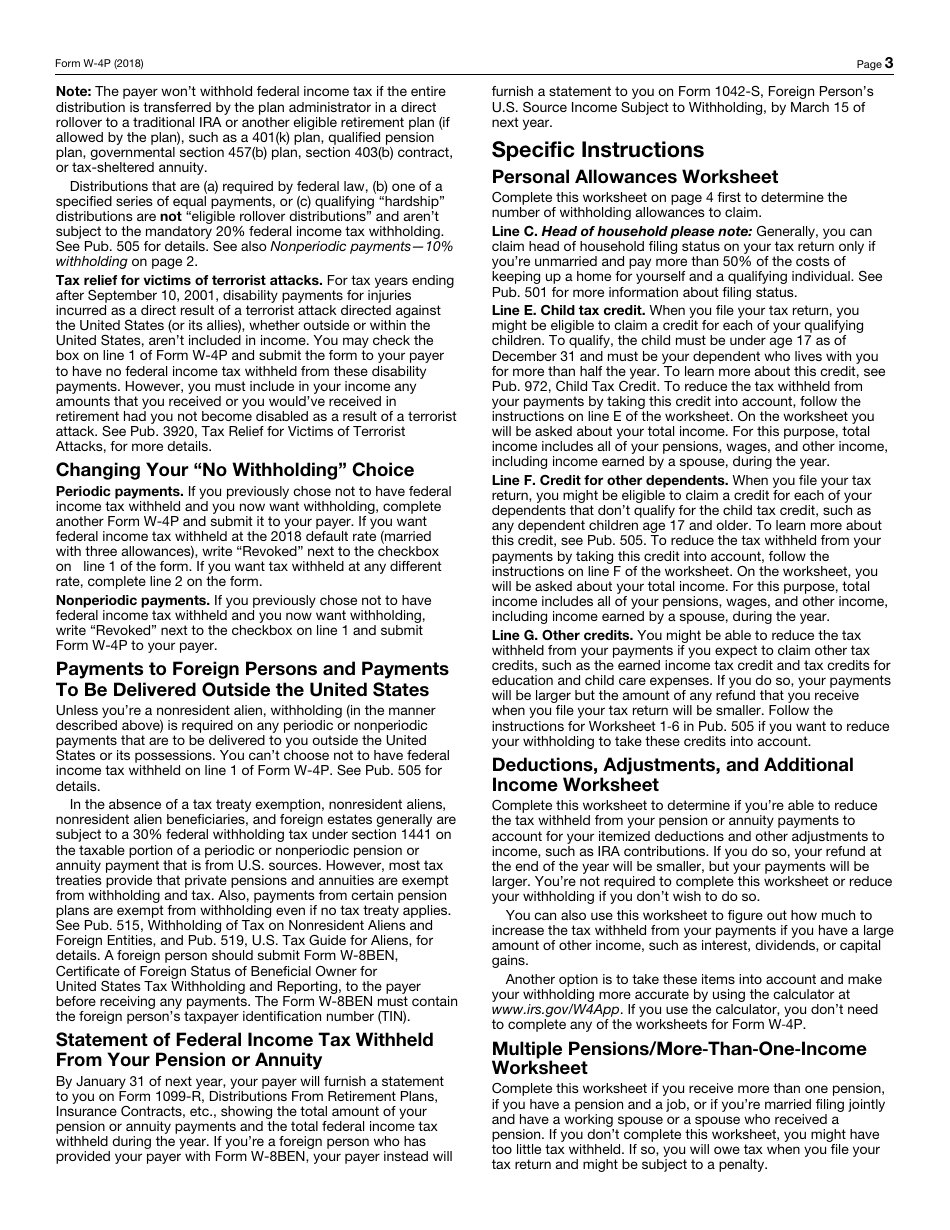

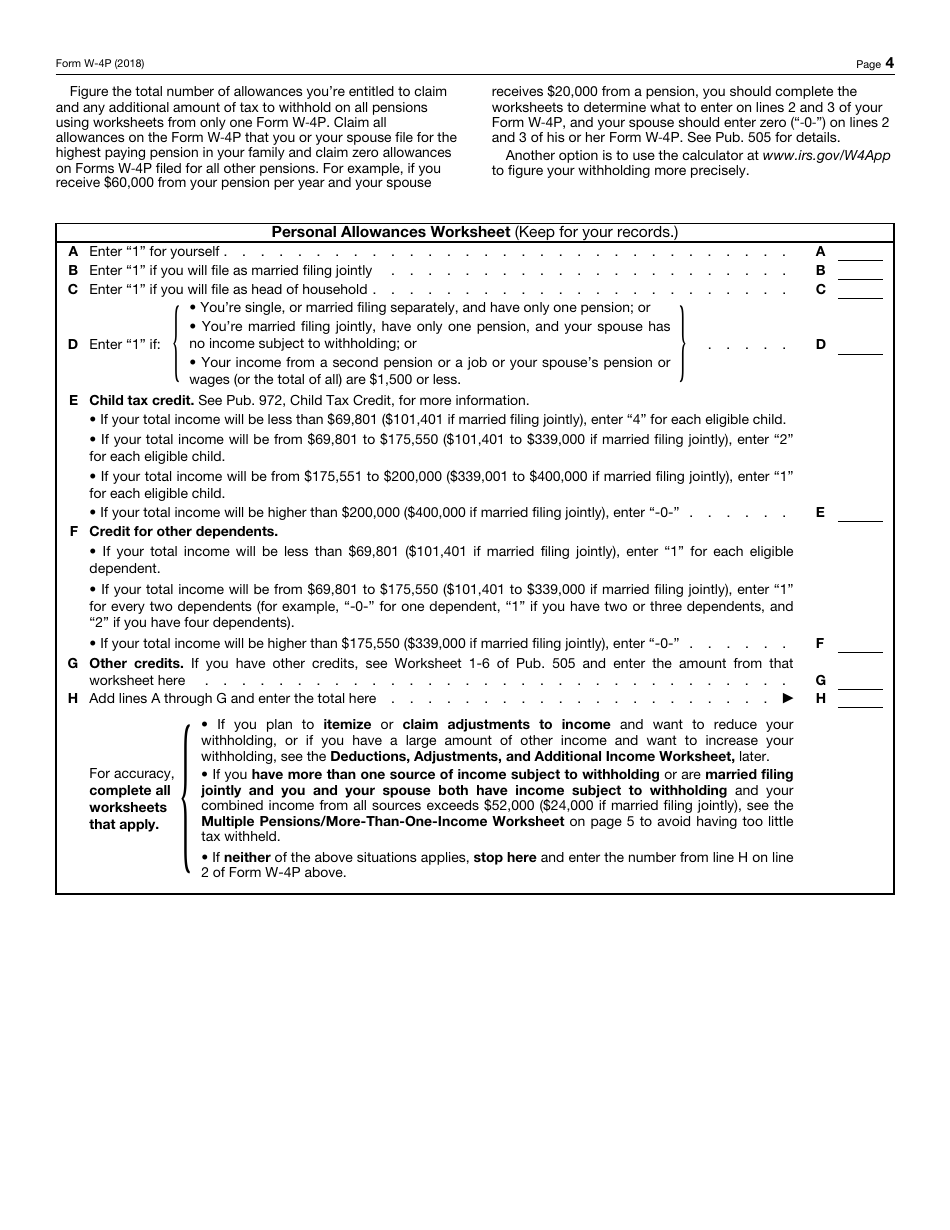

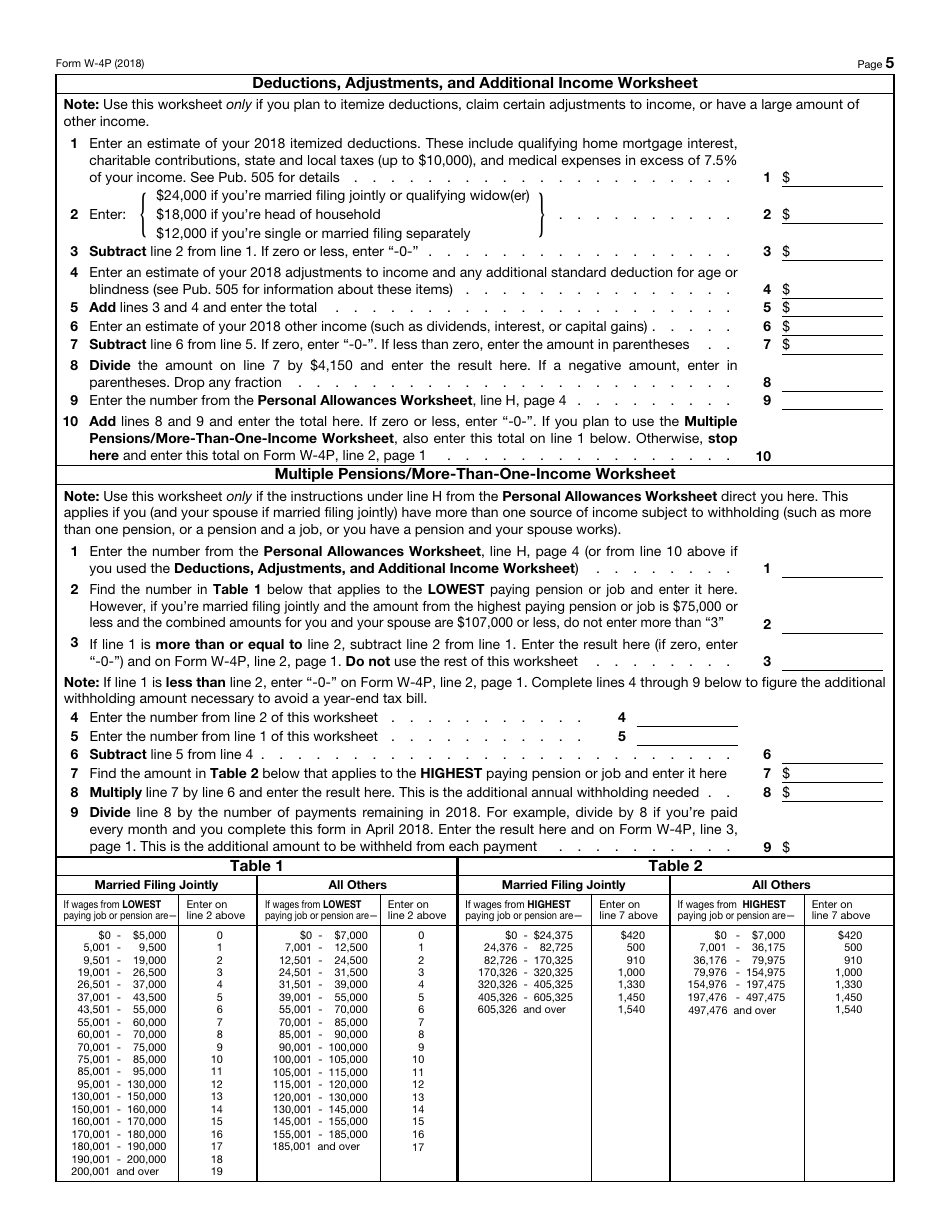

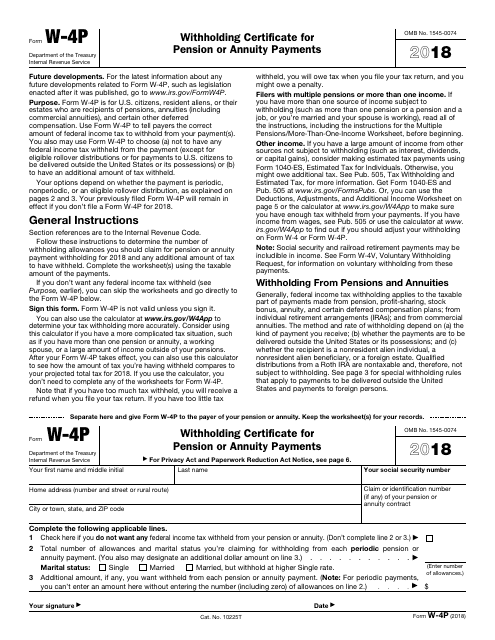

IRS Form W-4P Withholding Certificate for Pension or Annuity Payments

Fill PDF Online

Fill out online for free

without registration or credit card

What Is IRS Form W-4P?

This is a tax form that was released by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury on January 1, 2018. As of today, no separate filing guidelines for the form are provided by the IRS.

Form Details:

- A 6-page form available for download in PDF;

- This form cannot be used to file taxes for the current year. Choose a more recent version to file for the current tax year;

- Additional instructions and information can be found on page 1 of the document;

- Editable, printable, and free;

- Fill out the form in our online filing application.

Download a fillable version of IRS Form W-4P through the link below or browse more documents in our library of IRS Forms.

Download IRS Form W-4P Withholding Certificate for Pension or Annuity Payments

1

2

3

4

5

6