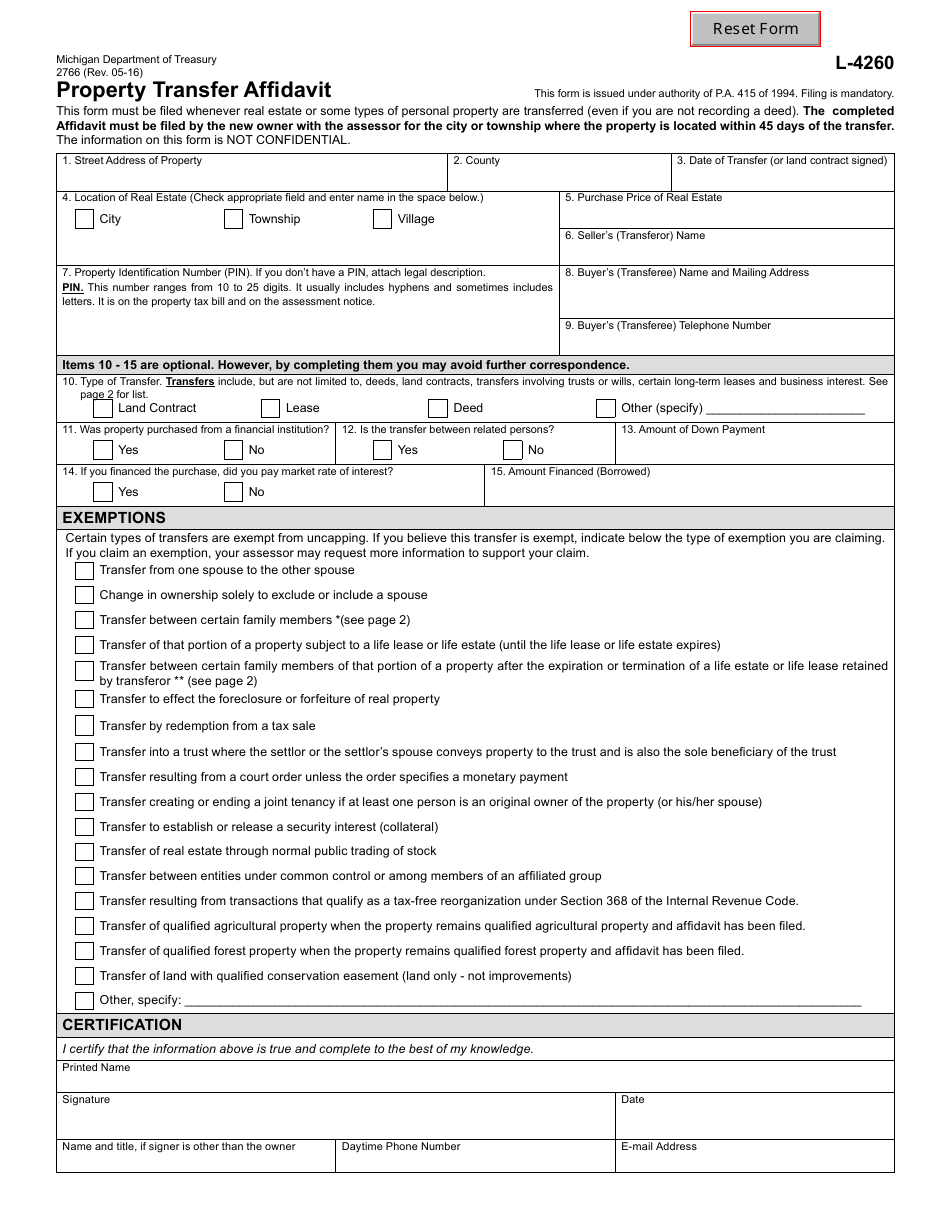

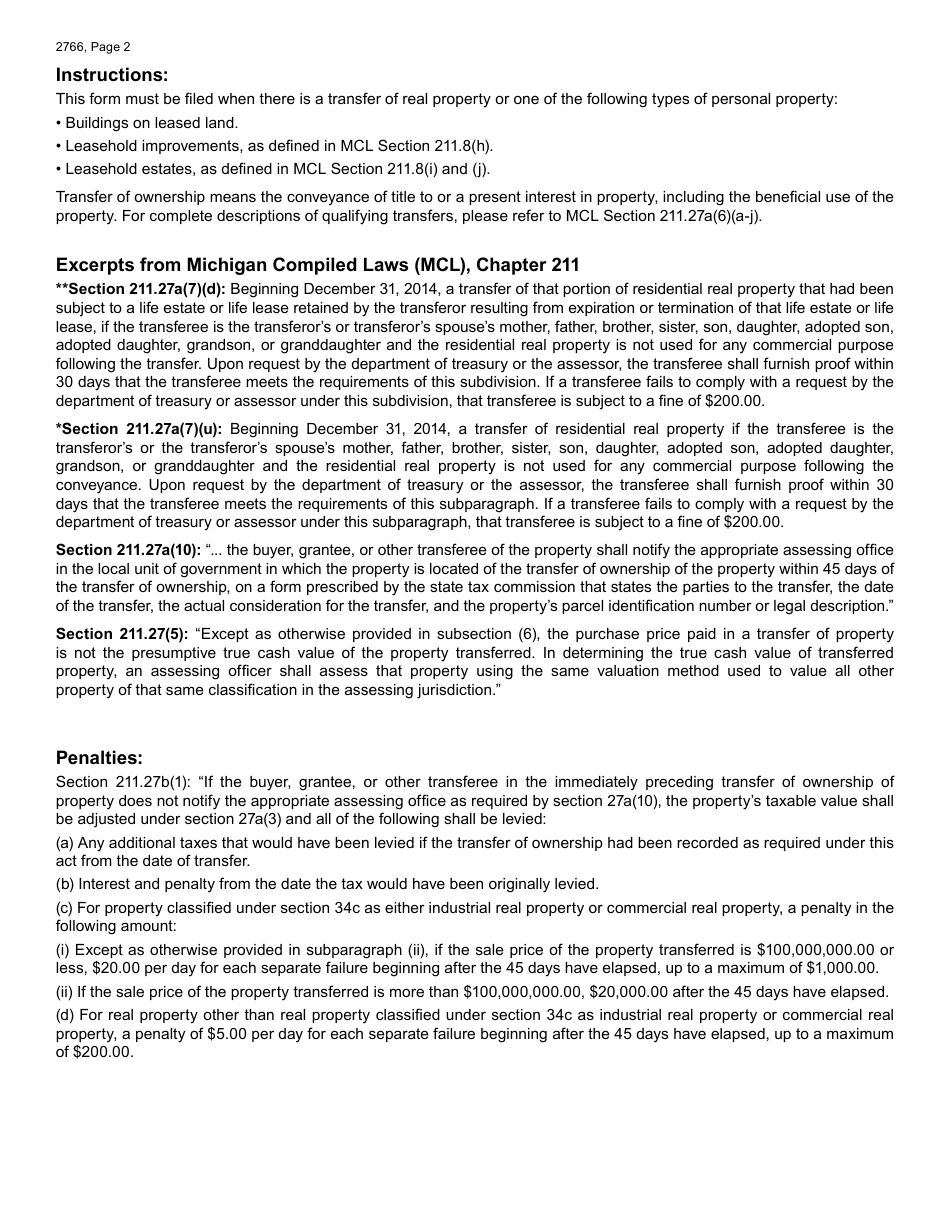

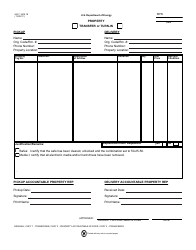

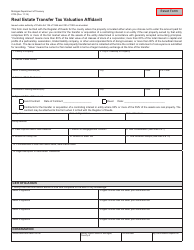

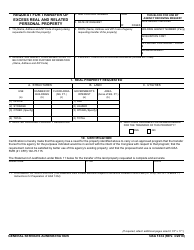

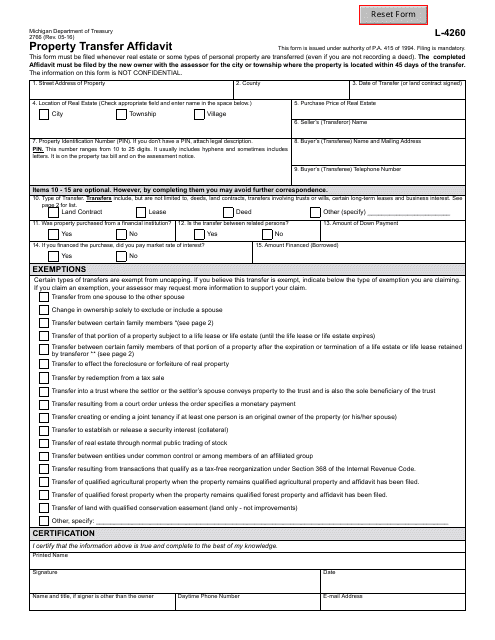

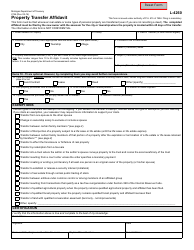

Form 2766 (L-4260) Property Transfer Affidavit - Michigan

What Is Form 2766 (L-4260)?

This is a legal form that was released by the Michigan Department of Treasury - a government authority operating within Michigan. Check the official instructions before completing and submitting the form.

FAQ

Q: What is Form 2766 (L-4260) Property Transfer Affidavit?

A: Form 2766 (L-4260) Property Transfer Affidavit is a legal document used in Michigan to report information about a property transfer.

Q: Who needs to fill out Form 2766 (L-4260) Property Transfer Affidavit?

A: The seller or transferor of a property in Michigan needs to fill out Form 2766 (L-4260) Property Transfer Affidavit.

Q: What information is required on Form 2766 (L-4260) Property Transfer Affidavit?

A: Form 2766 (L-4260) Property Transfer Affidavit requires information about the property, the seller, the buyer, the transfer date, and other details related to the transfer.

Q: Are there any fees associated with filing Form 2766 (L-4260) Property Transfer Affidavit?

A: Yes, there may be a fee associated with filing Form 2766 (L-4260) Property Transfer Affidavit. The fee varies depending on the local government jurisdiction.

Q: When should Form 2766 (L-4260) Property Transfer Affidavit be filed?

A: Form 2766 (L-4260) Property Transfer Affidavit should be filed within 45 days of the property transfer.

Form Details:

- Released on May 1, 2016;

- The latest edition provided by the Michigan Department of Treasury;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 2766 (L-4260) by clicking the link below or browse more documents and templates provided by the Michigan Department of Treasury.

Download Form 2766 (L-4260) Property Transfer Affidavit - Michigan

1

2