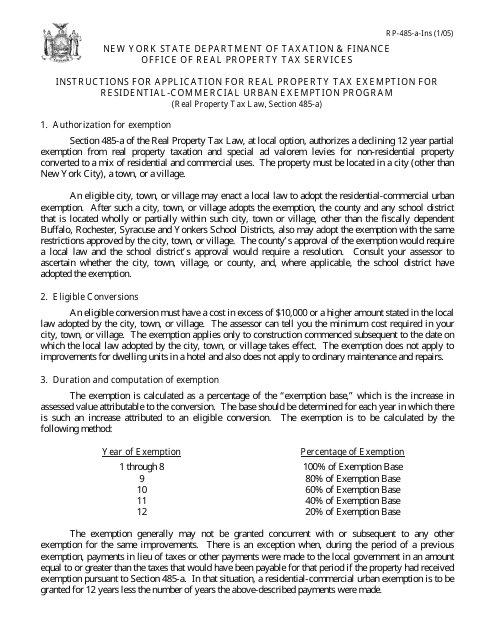

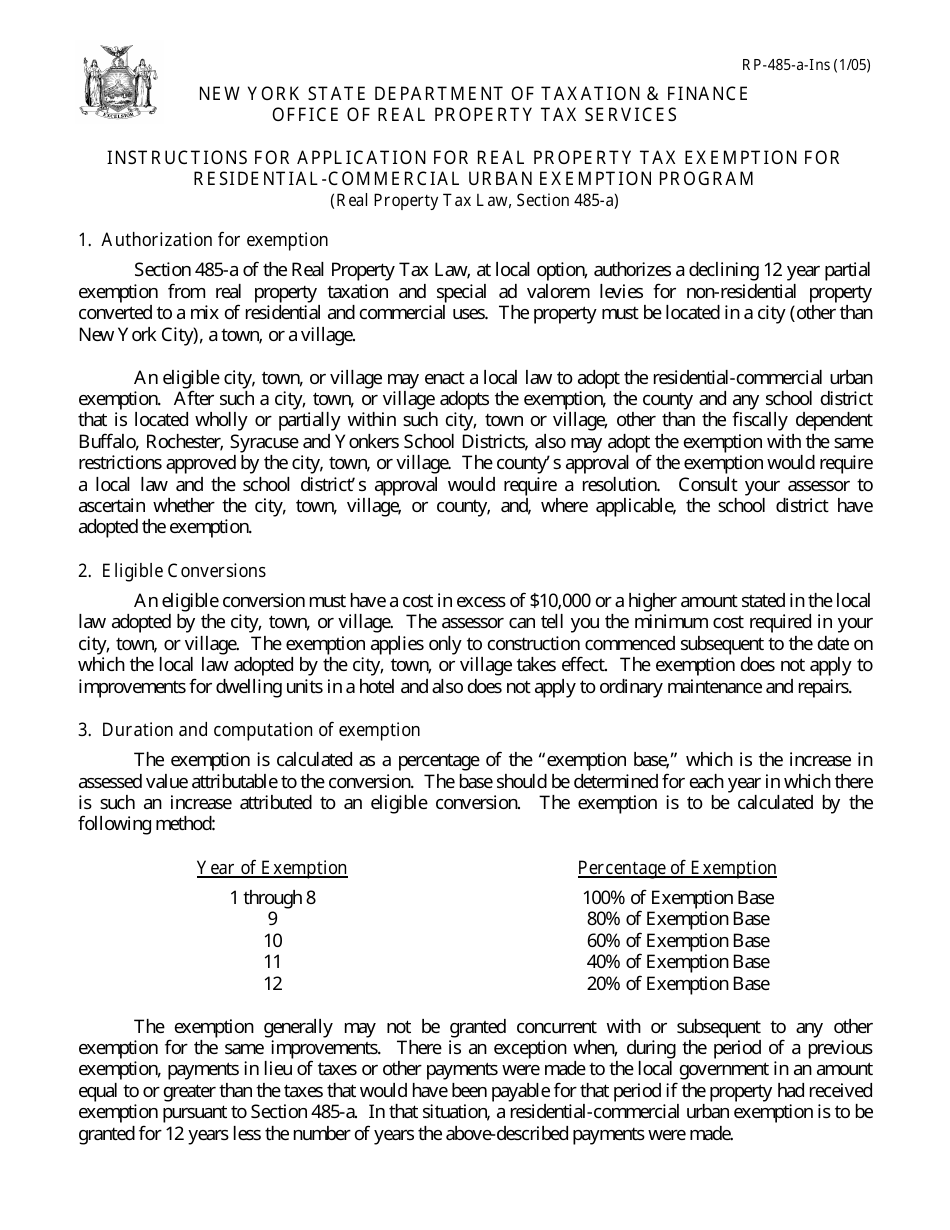

Instructions for Form RP-485-A Application for Real Property Tax Exemption for Residential-Commercial Urban Exemption Program - New York

This document contains official instructions for Form RP-485-A , Application for Real Property Tax Exemption for Residential-Commercial Urban Exemption Program - a form released and collected by the New York State Department of Taxation and Finance. An up-to-date fillable Form RP-485-A is available for download through this link.

FAQ

Q: What is Form RP-485-A?

A: Form RP-485-A is an application for real property tax exemption for the Residential-Commercial Urban Exemption Program in New York.

Q: What is the Residential-Commercial Urban Exemption Program?

A: The Residential-Commercial Urban Exemption Program is a program in New York that provides tax exemptions for qualifying residential-commercial properties.

Q: Who is eligible to apply for the tax exemption?

A: Property owners of qualifying residential-commercial properties in New York are eligible to apply for the tax exemption.

Q: What information do I need to provide on Form RP-485-A?

A: You need to provide information about the property, its use, income generated from it, and any financial documents requested in the form.

Q: What is the deadline for submitting the application?

A: The deadline for submitting the application is generally March 1st of the year in which you seek the exemption, but it is advised to check with your local tax assessor's office for any specific deadlines.

Q: Is there a fee for submitting the application?

A: No, there is no fee for submitting the application.

Q: How long does the tax exemption last?

A: The tax exemption typically lasts for a period of 10 years, but it is subject to renewal and compliance with program requirements.

Q: What should I do if my application is approved?

A: If your application is approved, you will receive a tax exemption certificate, and your property will be eligible for the tax exemption for the specified period.

Q: What should I do if my application is denied?

A: If your application is denied, you have the right to appeal the decision by filing a complaint with the New York State Board of Real Property Tax Services within 30 days of the denial.

Instruction Details:

- This 2-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the New York State Department of Taxation and Finance.

Download Instructions for Form RP-485-A Application for Real Property Tax Exemption for Residential-Commercial Urban Exemption Program - New York

1

2

![Document preview: Form RP-485-J [UTICA] Application for Residential Investment Real Property Tax Exemption - City of Utica, New York](https://data.templateroller.com/pdf_docs_html/578/5786/578659/form-rp-485-j-utica-application-for-residential-investment-real-property-tax-exemption-city-of-utica-new-york.png)

![Document preview: Form RP-485-J [SYRACUSE] Application for Residential Investment Real Property Tax Exemption - City of Syracuse, New York](https://data.templateroller.com/pdf_docs_html/578/5786/578658/form-rp-485-j-syracuse-application-for-residential-investment-real-property-tax-exemption-city-of-syracuse-new-york.png)

![Document preview: Form RP-485-K [UTICA SD] Application for Residential Investment Real Property Tax Exemption; Certain School Districts - City of Utica, New York](https://data.templateroller.com/pdf_docs_html/1349/13498/1349829/form-rp-485-k-utica-sd-application-for-residential-investment-real-property-tax-exemption-certain-school-districts-city-of-utica-new-york.png)

![Document preview: Form RP-485-J [AMSTERDAM] Application for Residential Investment Real Property Tax Exemption - City of Amsterdam, New York](https://data.templateroller.com/pdf_docs_html/578/5786/578657/form-rp-485-j-amsterdam-application-for-residential-investment-real-property-tax-exemption-city-of-amsterdam-new-york.png)

![Document preview: Form RP-485-I [JAMESTOWN SD] Application for Residential Investment Real Property Tax Exemption; Certain School Districts - New York](https://data.templateroller.com/pdf_docs_html/578/5786/578655/form-rp-485-i-jamestown-sd-application-residential-investment-real-property-tax-exemption-certain-school-districts-new-york.png)