Form B2400A / B ALT Reaffirmation Agreement

What Is a Reaffirmation Agreement?

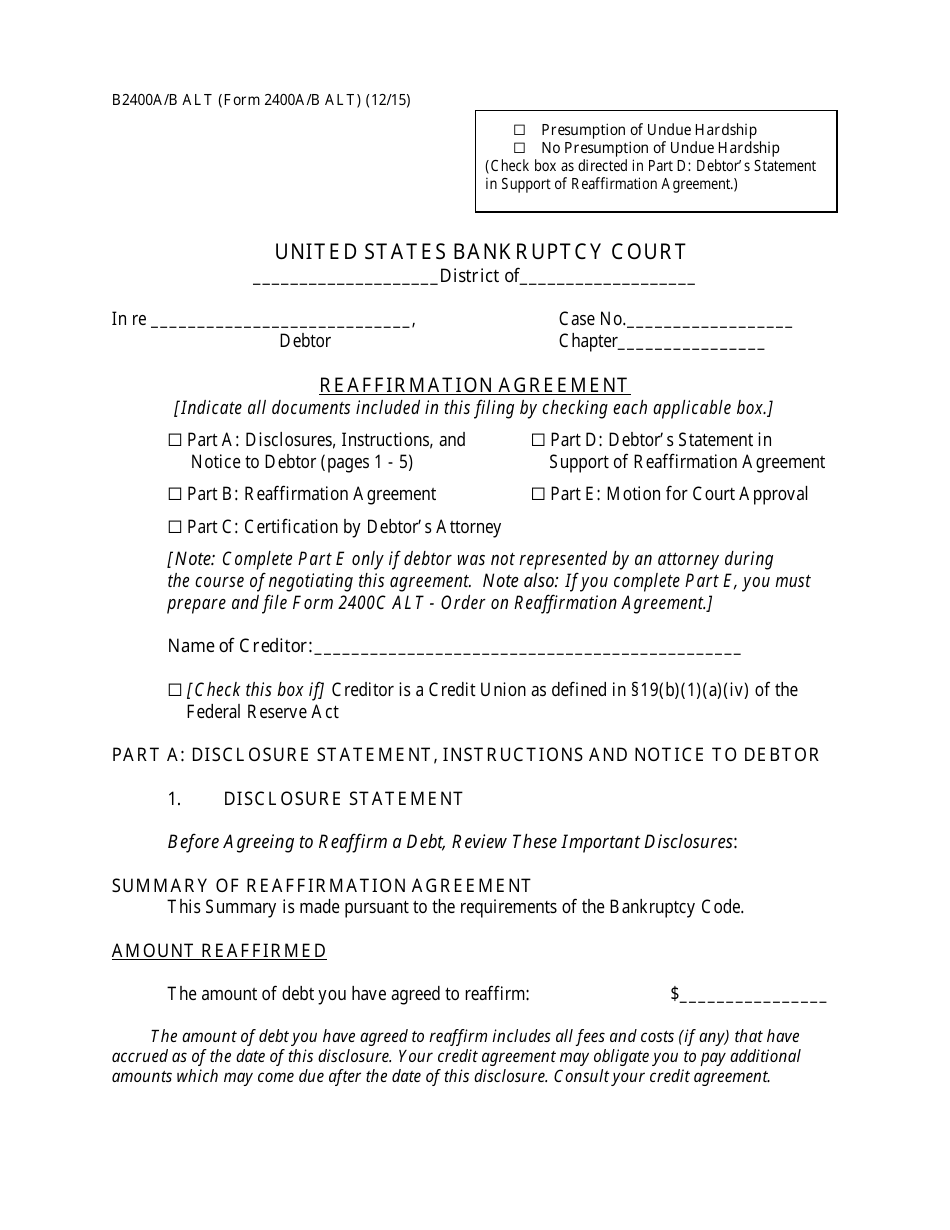

A Reaffirmation Agreement is a document signed by two parties, the lender and the debtor, to outline the repayment of the debt that will remain the liability of the debtor despite the ongoing bankruptcy process. Even if the borrower filed documentation for bankruptcy and cannot pay back all their debts, it is allowed to sign an agreement with the party they owe money to in order to keep their possessions - for instance, the debtor might want to keep their apartment or vehicle and they are able to do so via a repayment agreement.

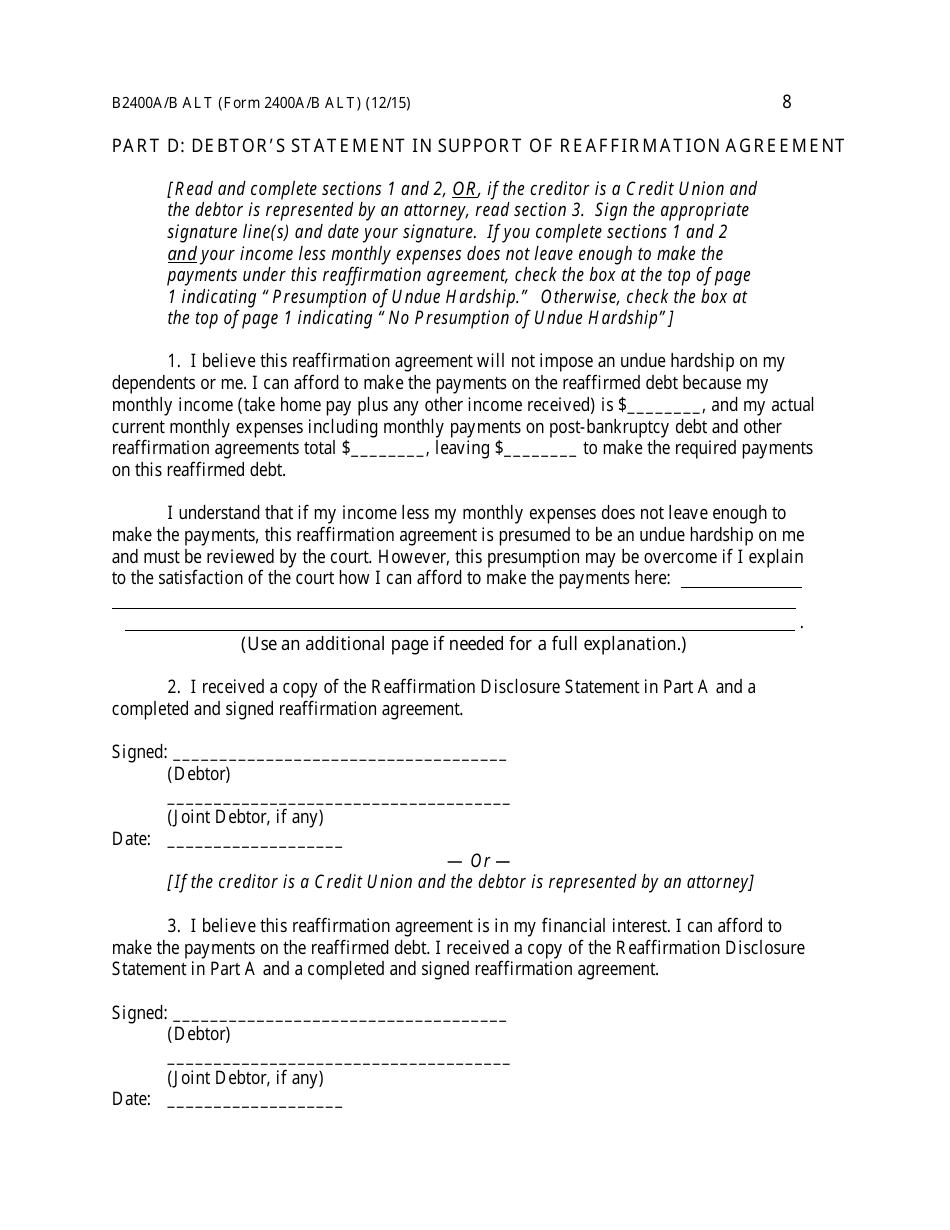

If your income and expenses allow you to make the payments on the reaffirmed debt, consider proposing a Reaffirmation Agreement form to your creditor who might want to secure money instead of the property - this way, you can keep the assets that have significance for your life while also dealing with one of the debts and creditors even in the light of the upcoming insolvency.

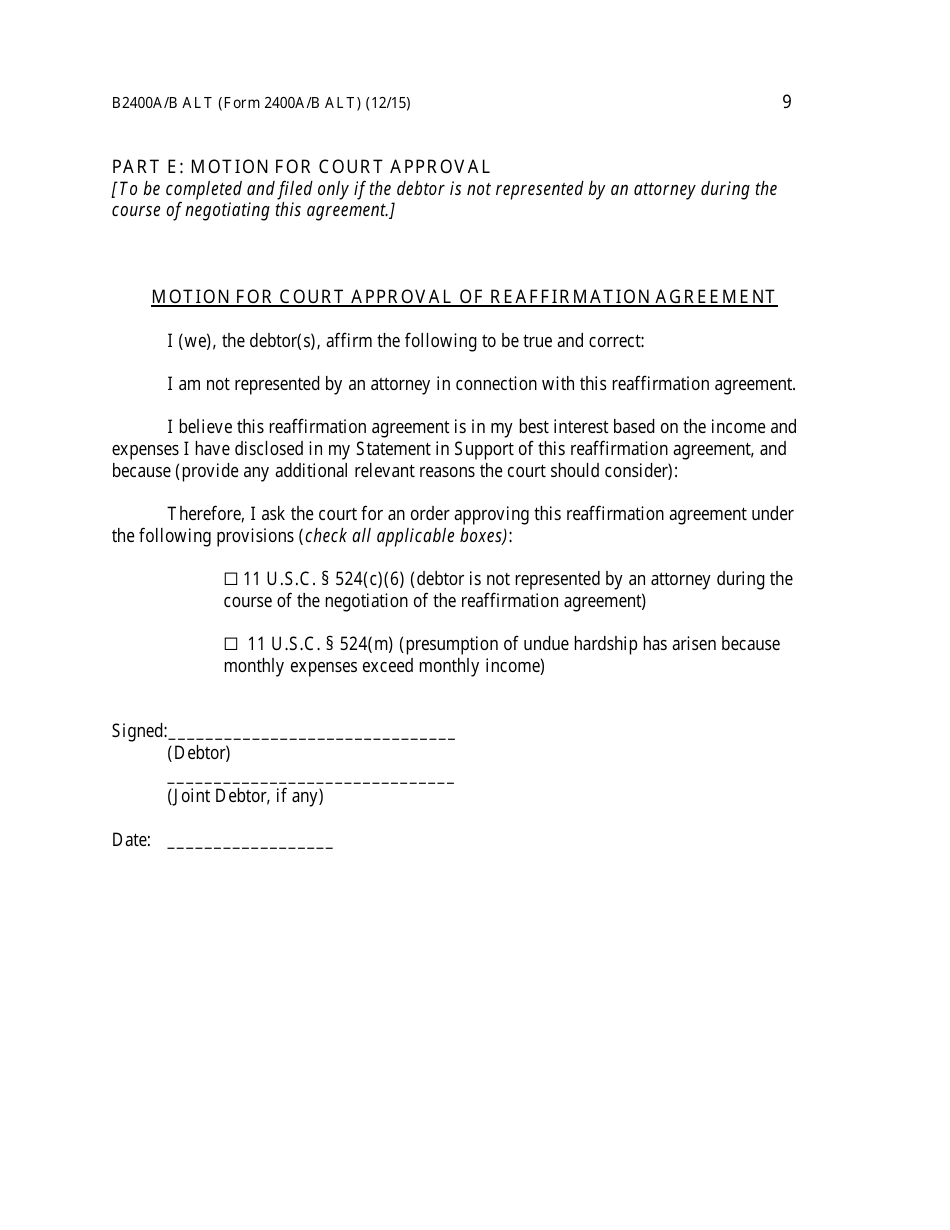

The United States Bankruptcy Court provides a universal form of Reaffirmation Contract: Form B2400A/B ALT, Reaffirmation Agreement , released on December 1, 2015 , that can be accessed through the link below.

How to Write a Reaffirmation Agreement?

Your written Reaffirmation Agreement should contain the following information:

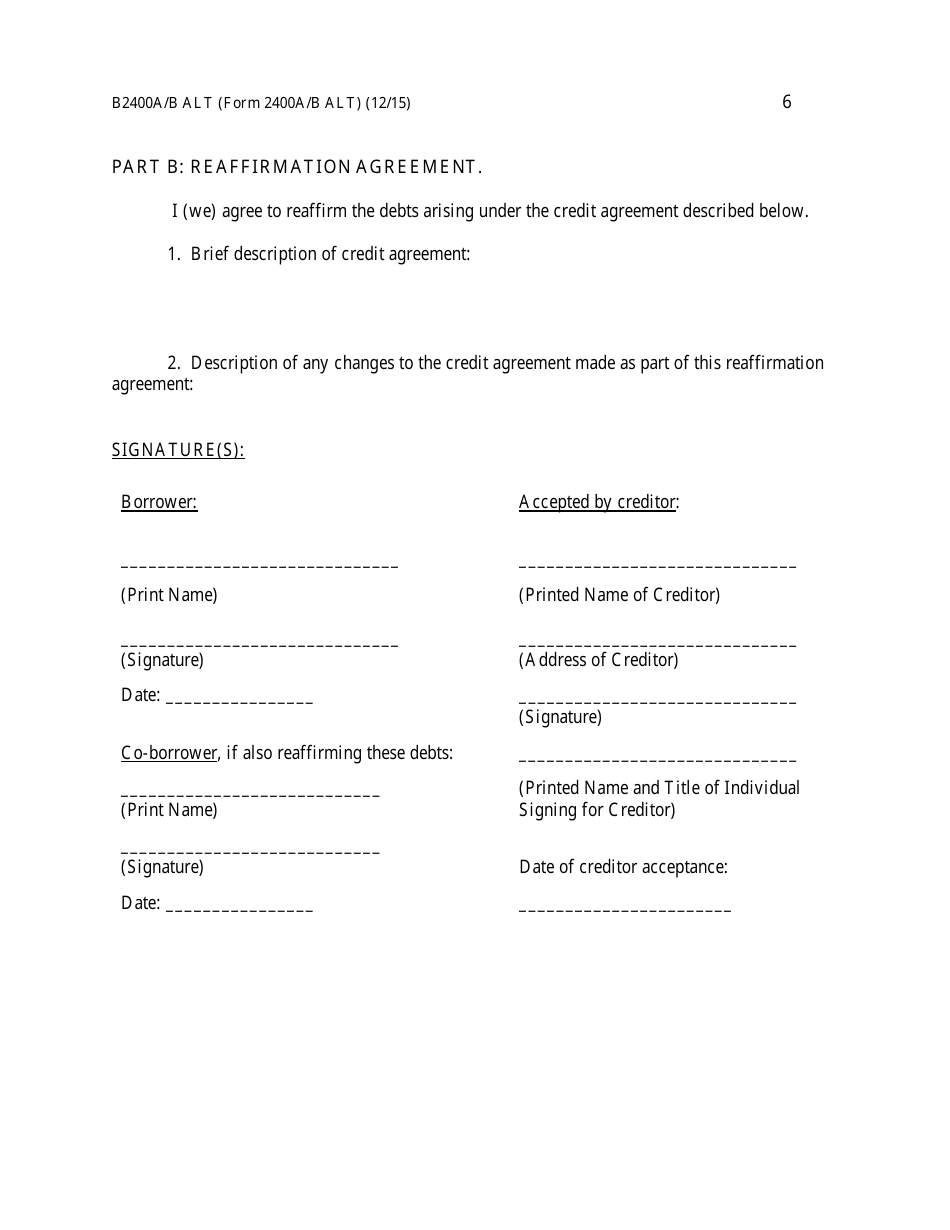

- Proper identification of the parties, their names, addresses, and other contact details.

- Description of the debt the borrower has agreed to reaffirm . You need to specify the amount of the debt and possible additional fees and costs.

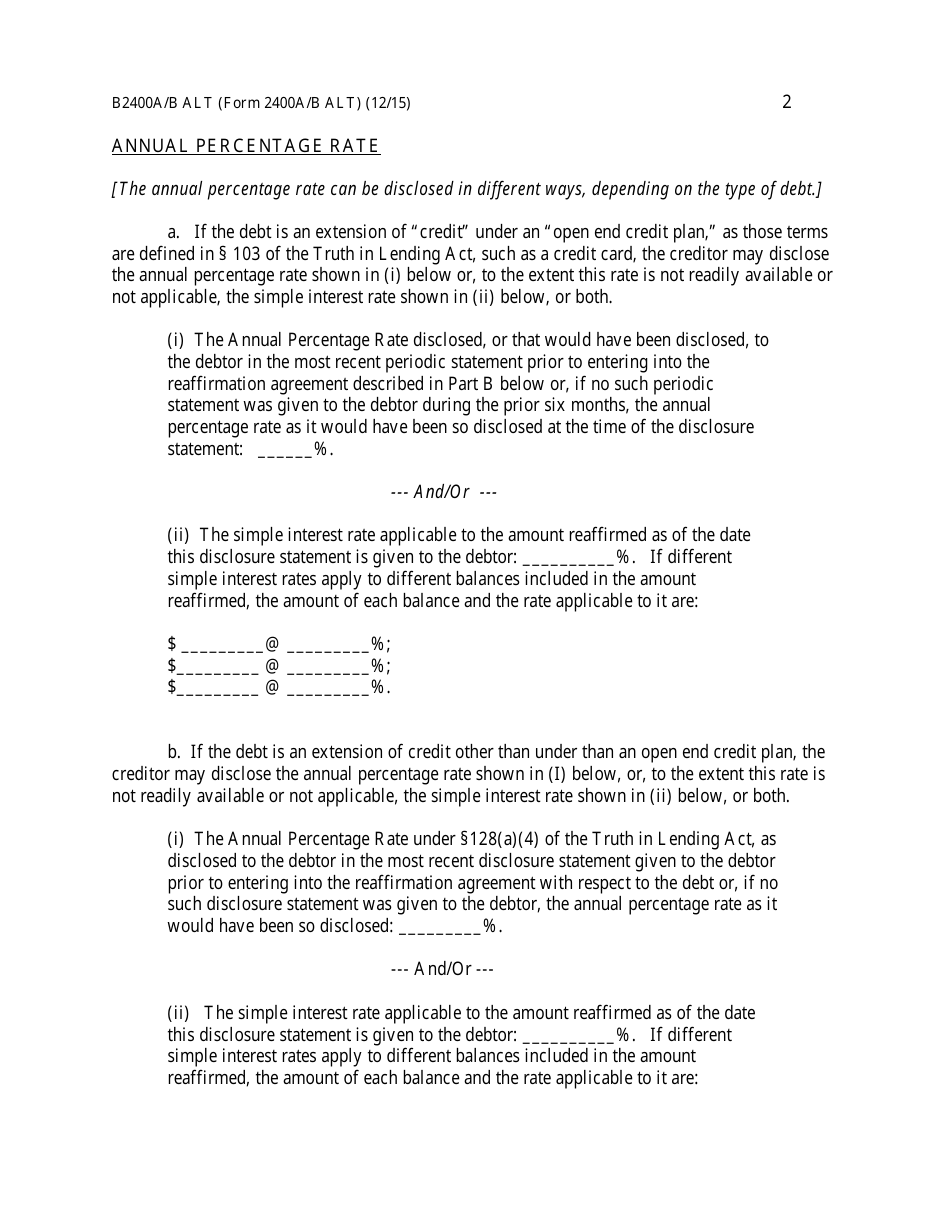

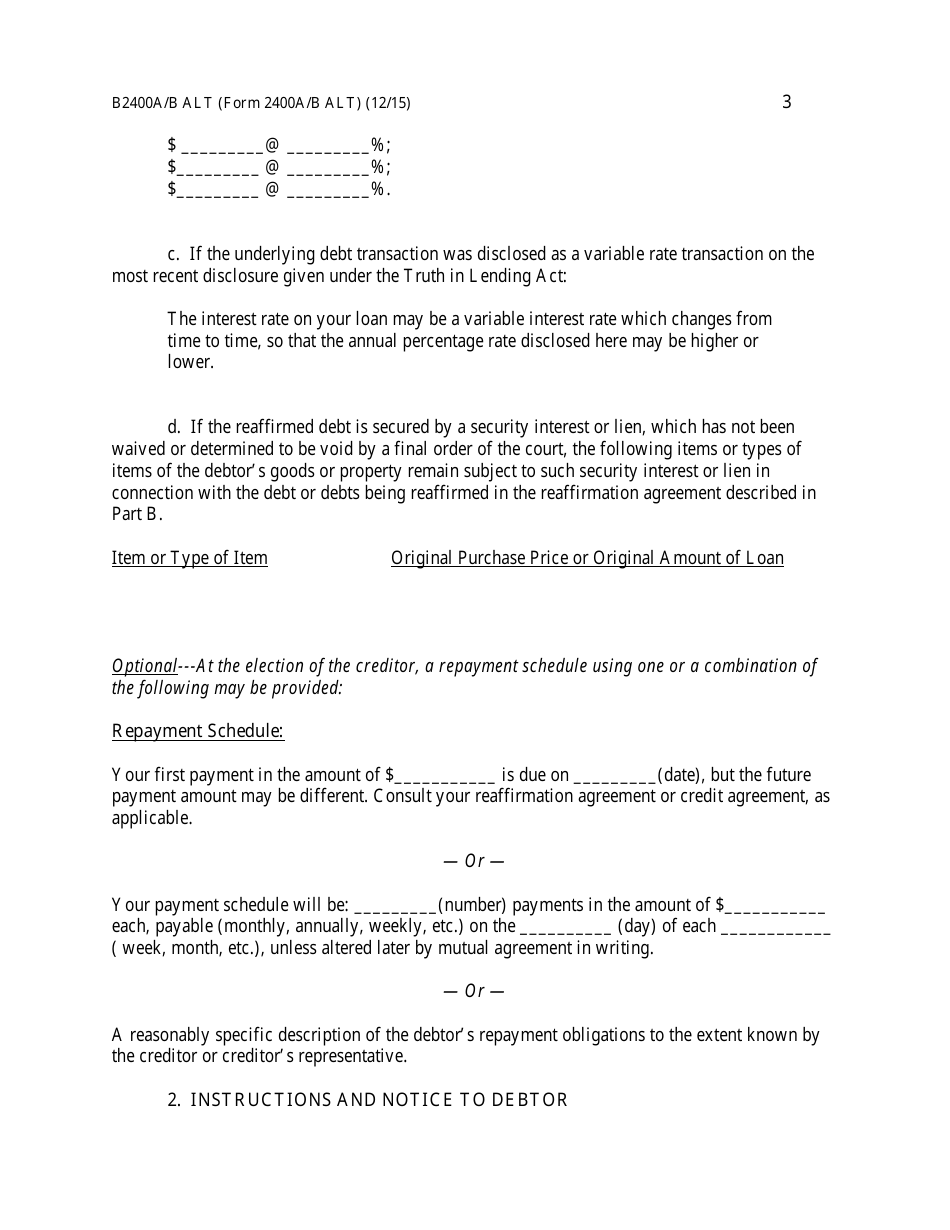

- Annual percentage rate.

- Repayment schedule . State when the debtor must provide their first payment, its exact amount, and the date. Future amounts may be different. Describe the schedule - you may opt for a monthly, biweekly, or weekly payment, typically made on the first day of the month, two week period, or week.

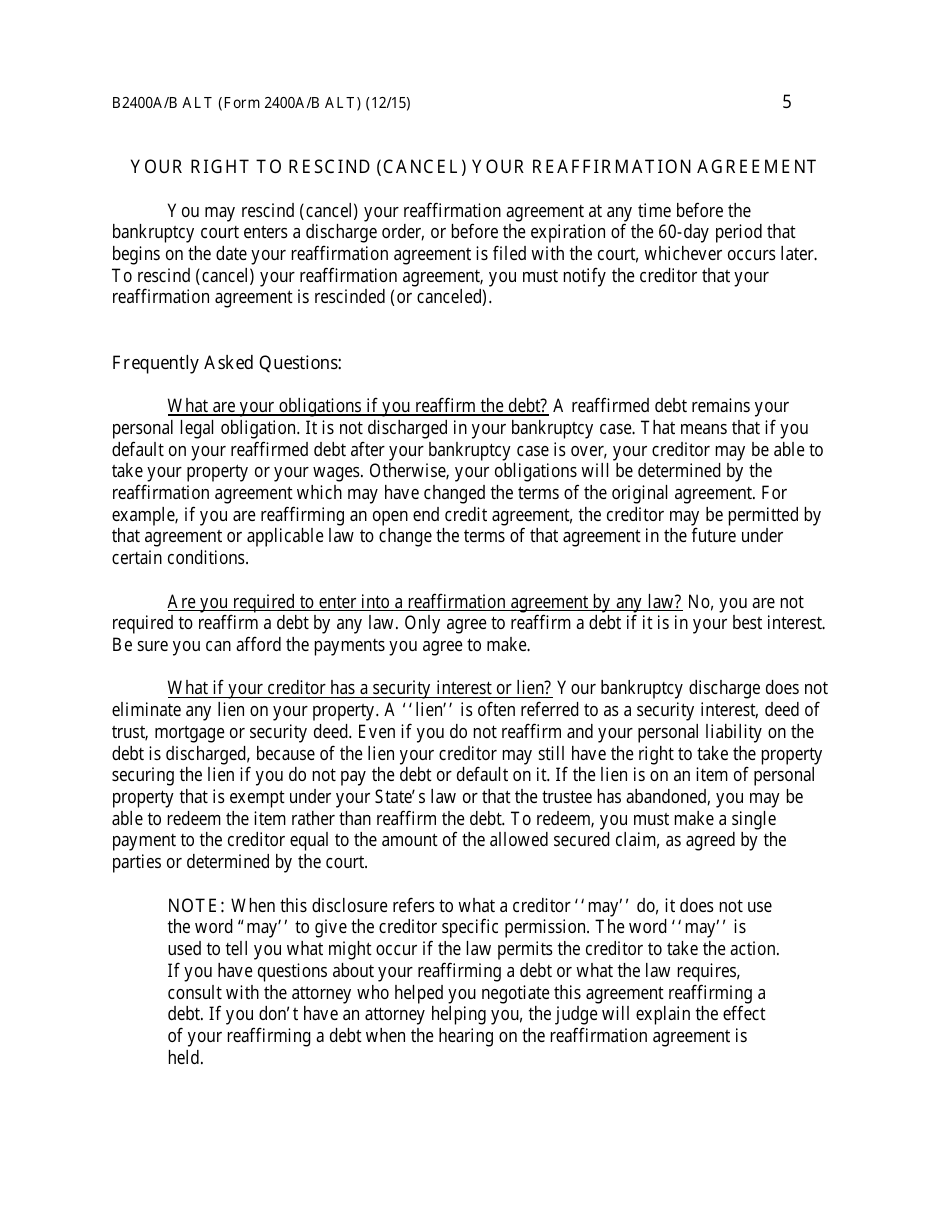

- Cancellation clause . Either party may warn the other about their intention to rescind the agreement - still, the borrower will owe the remaining balance of the debt which remains their personal obligation, even if the creditor takes their property back.

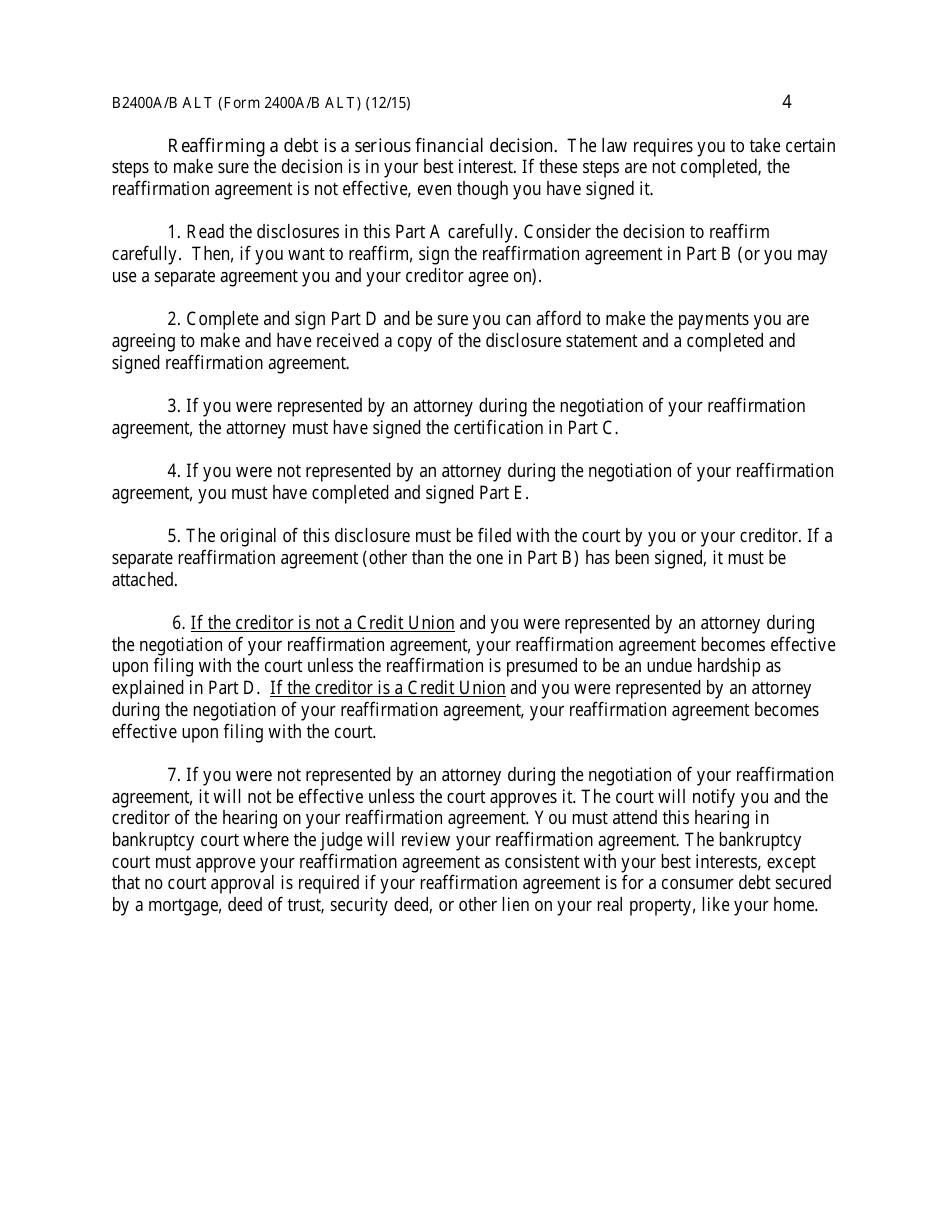

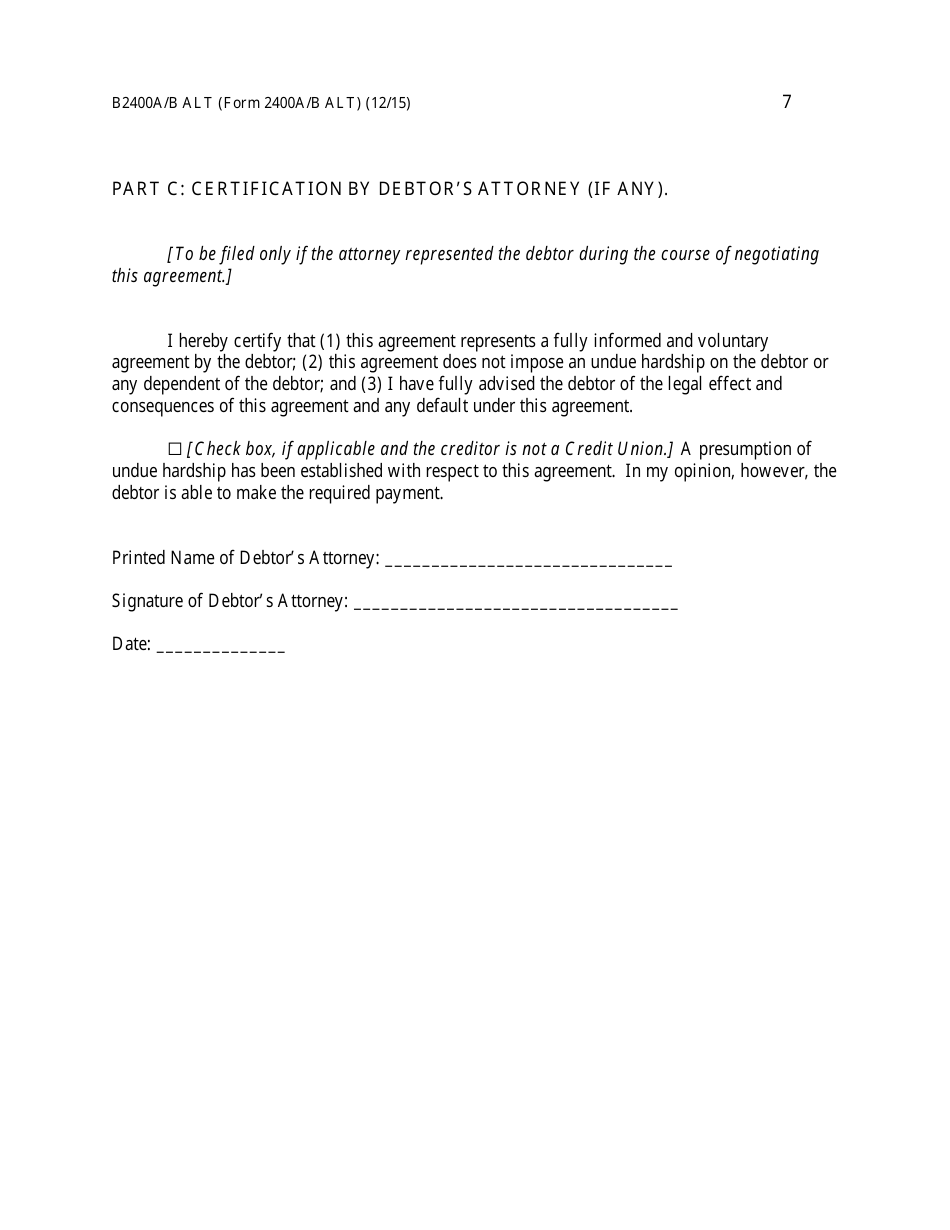

- Confirmation that both parties understood the agreement in its entirety, printed names and signatures of the parties . Do not forget to date the document. Note that you may enter negotiations regarding your debt at any time - if you feel you need to modify the agreement, contact the other party and offer them new terms you deem reasonable.

Related Forms and Topics:

- Bankruptcy forms sorted by type;

- Financial Statement;

- Corporate Guarantee;

- Personal Guarantee.

Download Form B2400A / B ALT Reaffirmation Agreement

1

2

3

4

5

6

7

8

9