![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CG

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CG

for the current year.

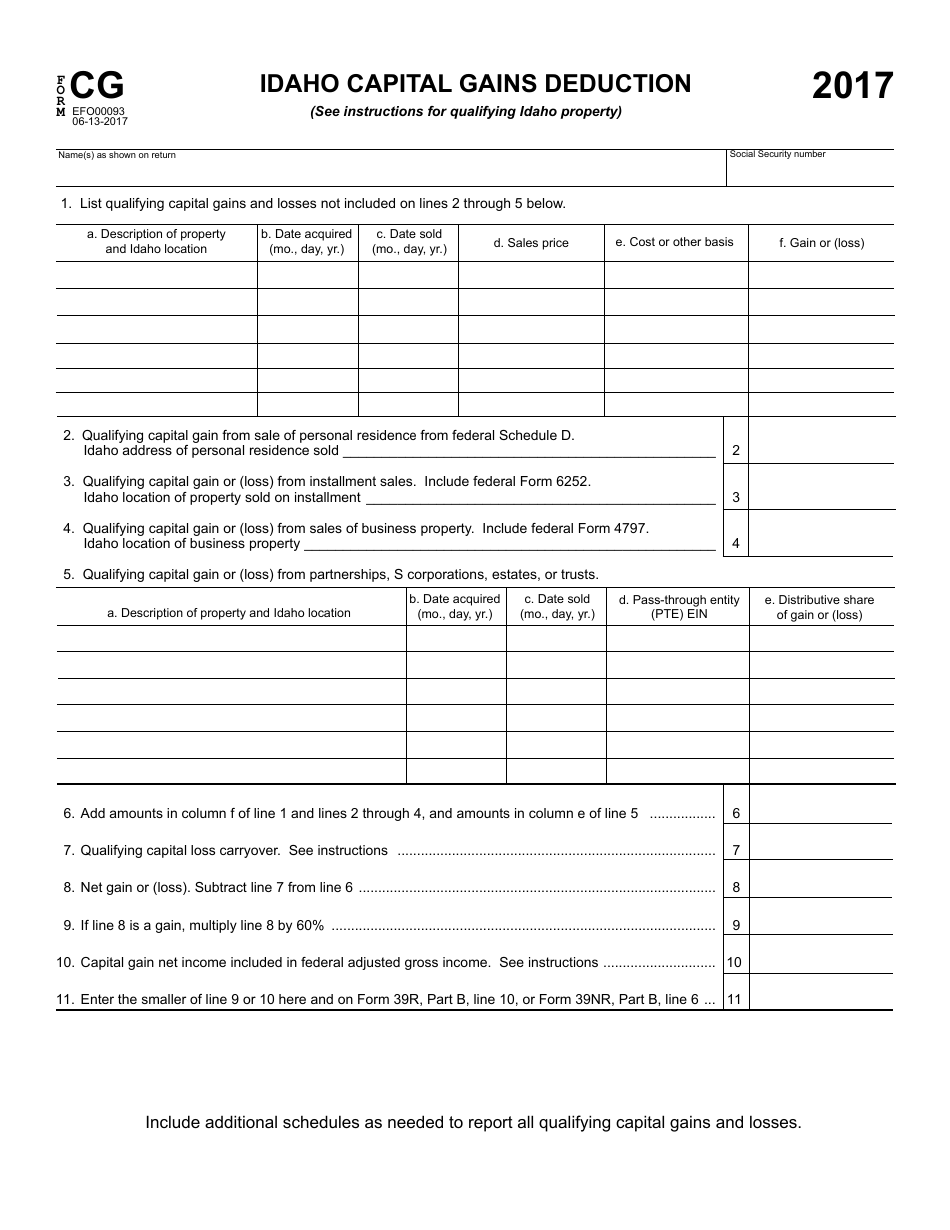

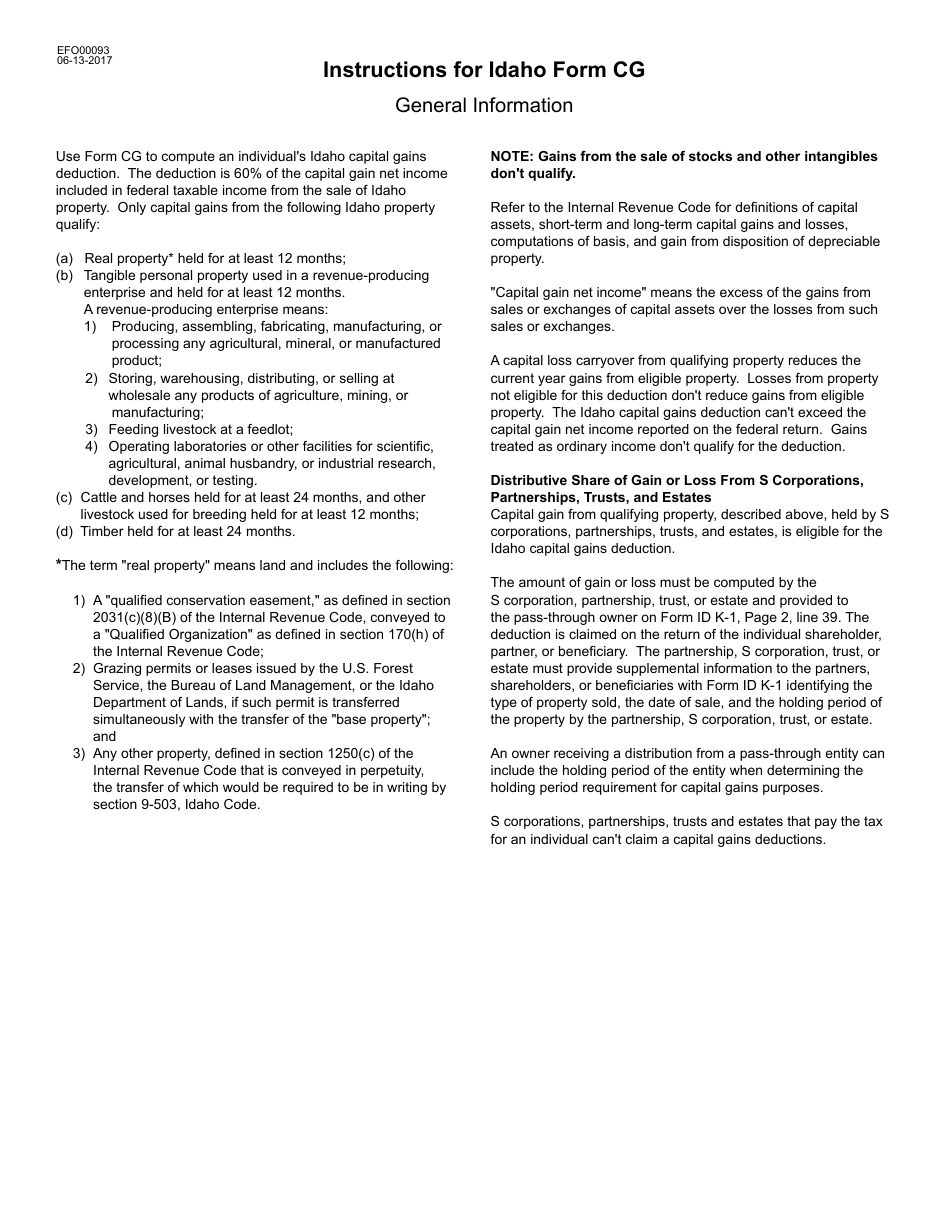

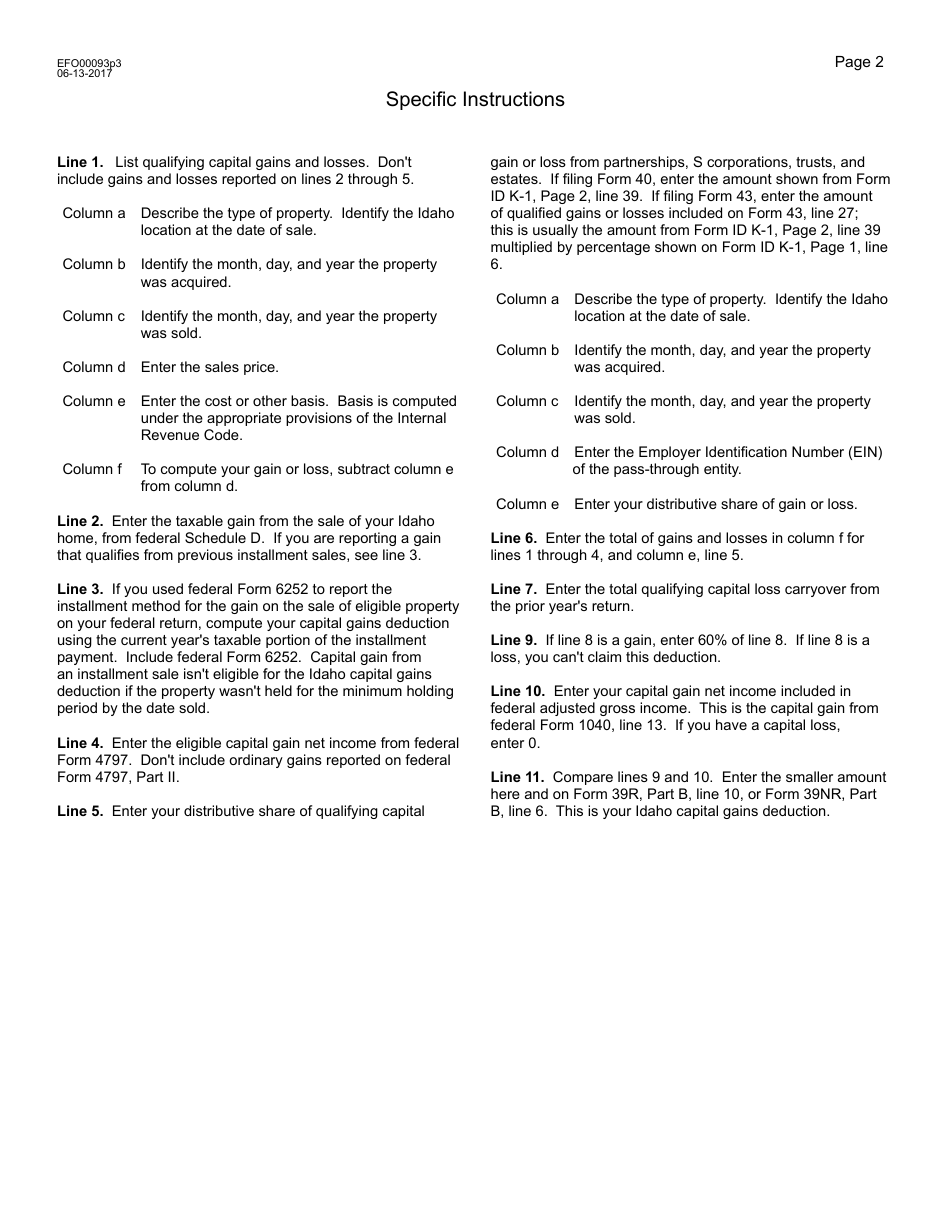

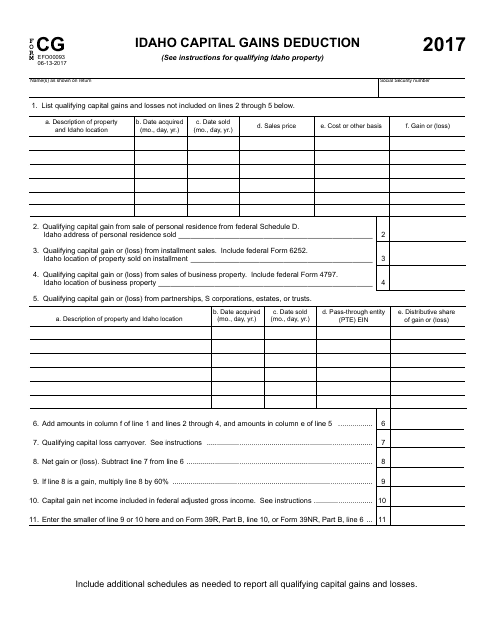

Form CG Idaho Capital Gains Deduction - Idaho

What Is Form CG?

This is a legal form that was released by the Idaho State Tax Commission - a government authority operating within Idaho. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the Form CG Idaho Capital Gains Deduction?

A: The Form CG Idaho Capital Gains Deduction is a tax form used by residents of Idaho to claim a deduction on their state income taxes for capital gains.

Q: Who can use the Form CG Idaho Capital Gains Deduction?

A: Only residents of Idaho who have realized capital gains during the tax year can use the Form CG Idaho Capital Gains Deduction.

Q: What information do I need to complete the Form CG Idaho Capital Gains Deduction?

A: You will need information about the capital gains you realized during the tax year, such as the amount of the gain and the type of asset sold.

Q: What is the deadline to file the Form CG Idaho Capital Gains Deduction?

A: The deadline to file the Form CG Idaho Capital Gains Deduction is the same as the deadline for filing your Idaho state income tax return, which is usually April 15th.

Q: Are there any limitations or restrictions to be aware of when using the Form CG Idaho Capital Gains Deduction?

A: Yes, there are limitations and restrictions on the amount of the deduction based on your filing status and income level. It is recommended to consult the instructions and guidelines provided with the form.

Q: Can I e-file the Form CG Idaho Capital Gains Deduction?

A: Yes, you can e-file the Form CG Idaho Capital Gains Deduction if you are electronically filing your Idaho state income tax return.

Q: Is the Form CG Idaho Capital Gains Deduction available for non-residents of Idaho?

A: No, the Form CG Idaho Capital Gains Deduction is only available for residents of Idaho.

Q: Do I need to include any supporting documentation with the Form CG Idaho Capital Gains Deduction?

A: You may be required to include supporting documentation, such as copies of your federal tax return and any applicable schedules or forms related to your capital gains.

Q: What happens if I fail to file the Form CG Idaho Capital Gains Deduction?

A: If you fail to file the Form CG Idaho Capital Gains Deduction and you were eligible for the deduction, you may overpay your state income taxes. It is important to ensure that you claim all eligible deductions to minimize your tax liability.

Form Details:

- Released on June 13, 2017;

- The latest edition provided by the Idaho State Tax Commission;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CG by clicking the link below or browse more documents and templates provided by the Idaho State Tax Commission.

Download Form CG Idaho Capital Gains Deduction - Idaho

1

2

3