![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 500C

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 500C

for the current year.

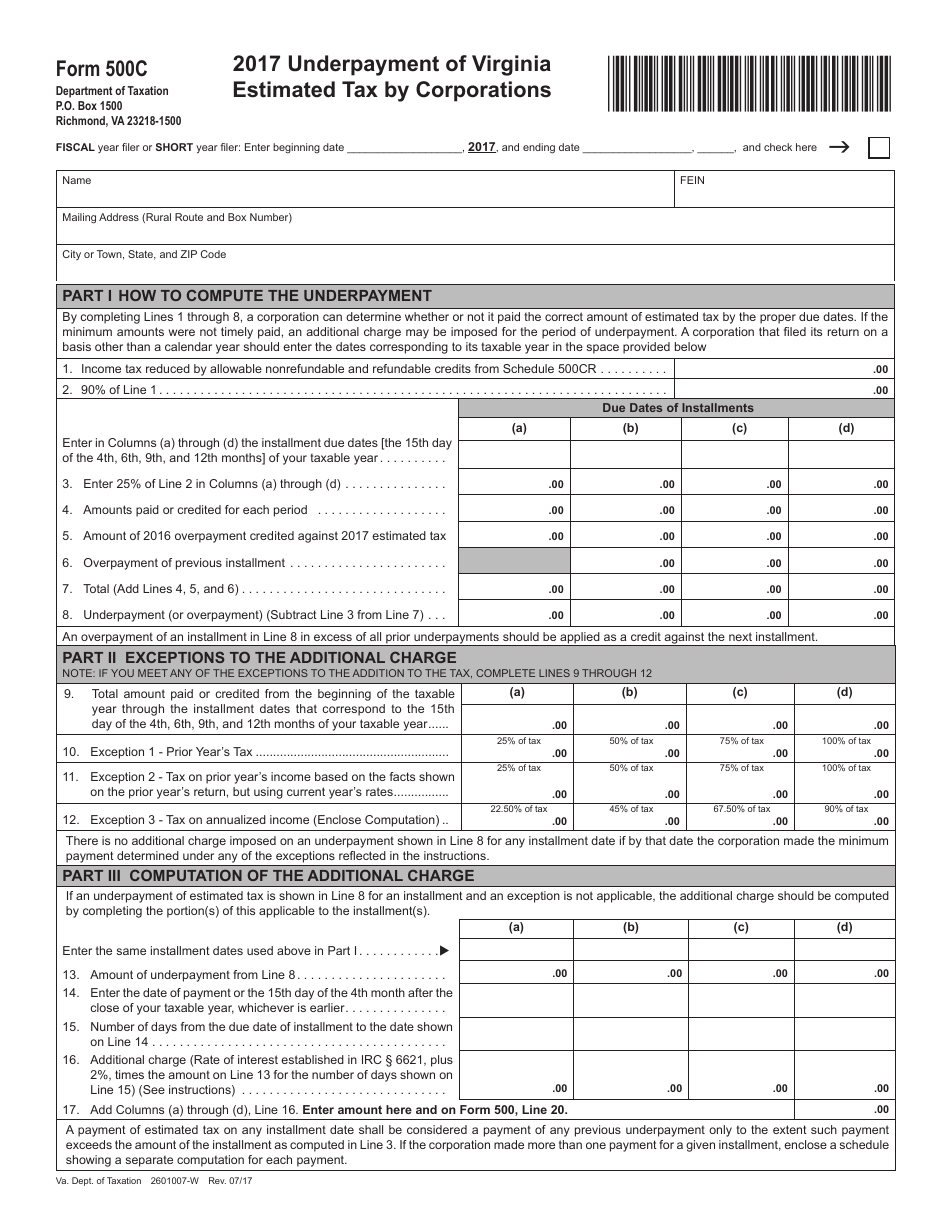

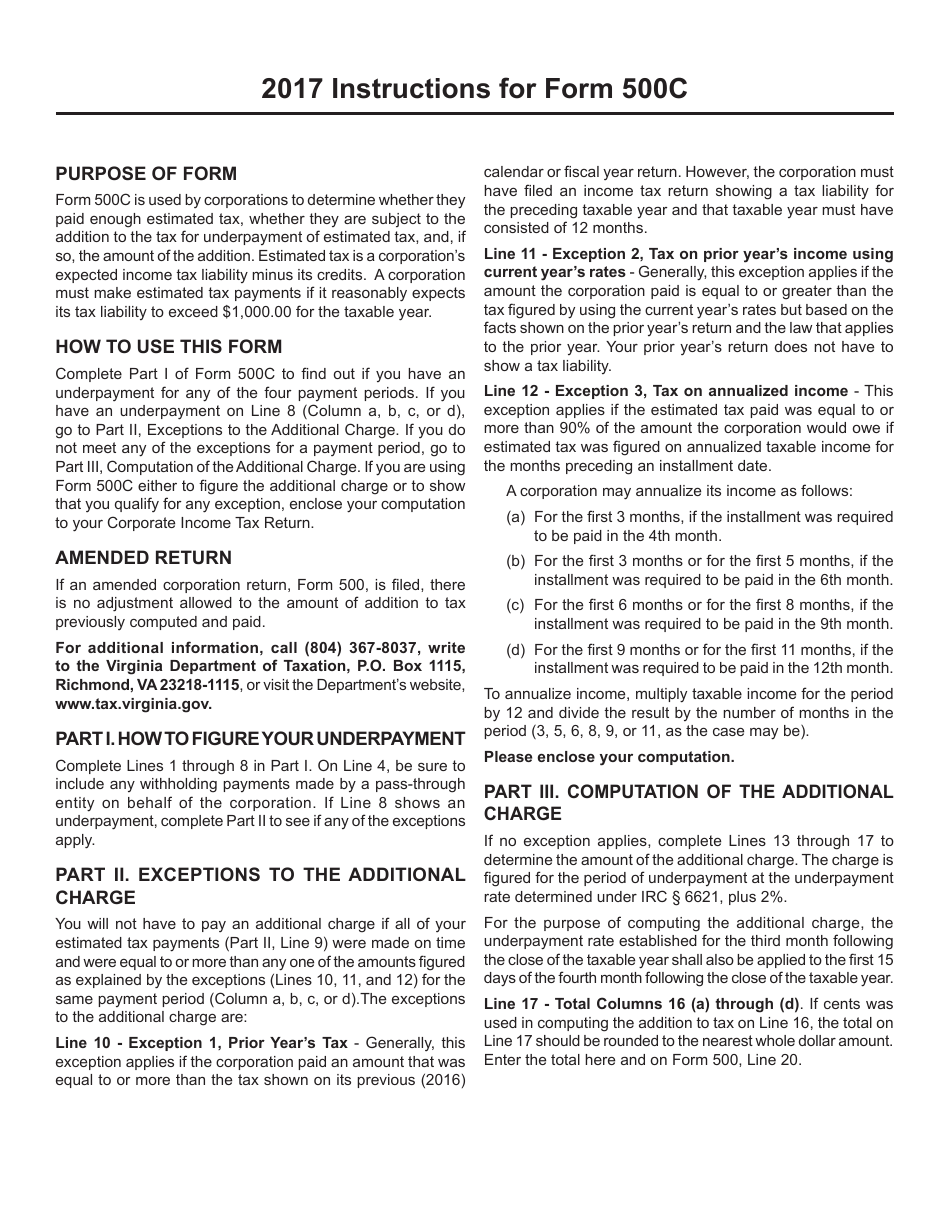

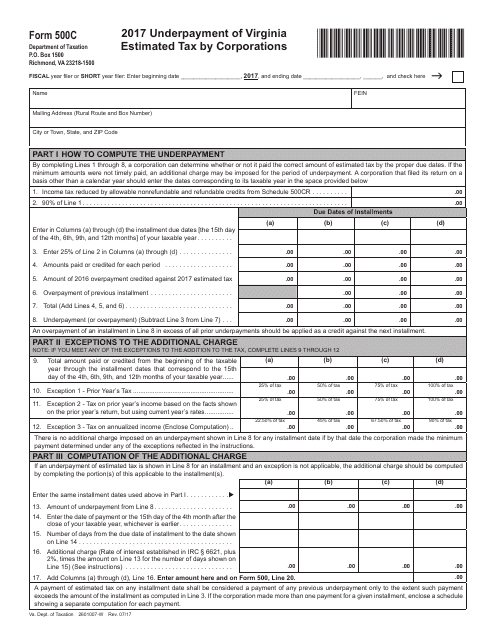

Form 500C Underpayment of Virginia Estimated Tax by Corporations - Virginia

What Is Form 500C?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 500C?

A: Form 500C is a tax form used by corporations in Virginia to report any underpayment of estimated taxes.

Q: What is Virginia estimated tax?

A: Virginia estimated tax is the amount of tax that corporations are required to pay in advance throughout the year based on their estimated income.

Q: Who needs to file Form 500C?

A: Corporations in Virginia that have underpaid their estimated taxes need to file Form 500C.

Q: What happens if a corporation underpays its estimated taxes in Virginia?

A: If a corporation underpays its estimated taxes in Virginia, it may be subject to penalties and interest.

Q: When is the deadline to file Form 500C?

A: The deadline to file Form 500C is generally the same as the deadline to file a corporation's annual tax return, which is the 15th day of the fourth month following the end of the corporation's tax year.

Q: Are there any penalties for not filing Form 500C?

A: Yes, there may be penalties for not filing Form 500C, as it is required for corporations that have underpaid their estimated taxes in Virginia.

Q: Can Form 500C be amended?

A: Yes, if there are errors or changes in the underpayment of estimated taxes, Form 500C can be amended by filing a corrected form.

Q: Is Form 500C required for individuals?

A: No, Form 500C is specifically for corporations in Virginia that have underpaid their estimated taxes. Individuals do not need to file this form.

Form Details:

- Released on July 1, 2017;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 500C by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.

Download Form 500C Underpayment of Virginia Estimated Tax by Corporations - Virginia

1

2