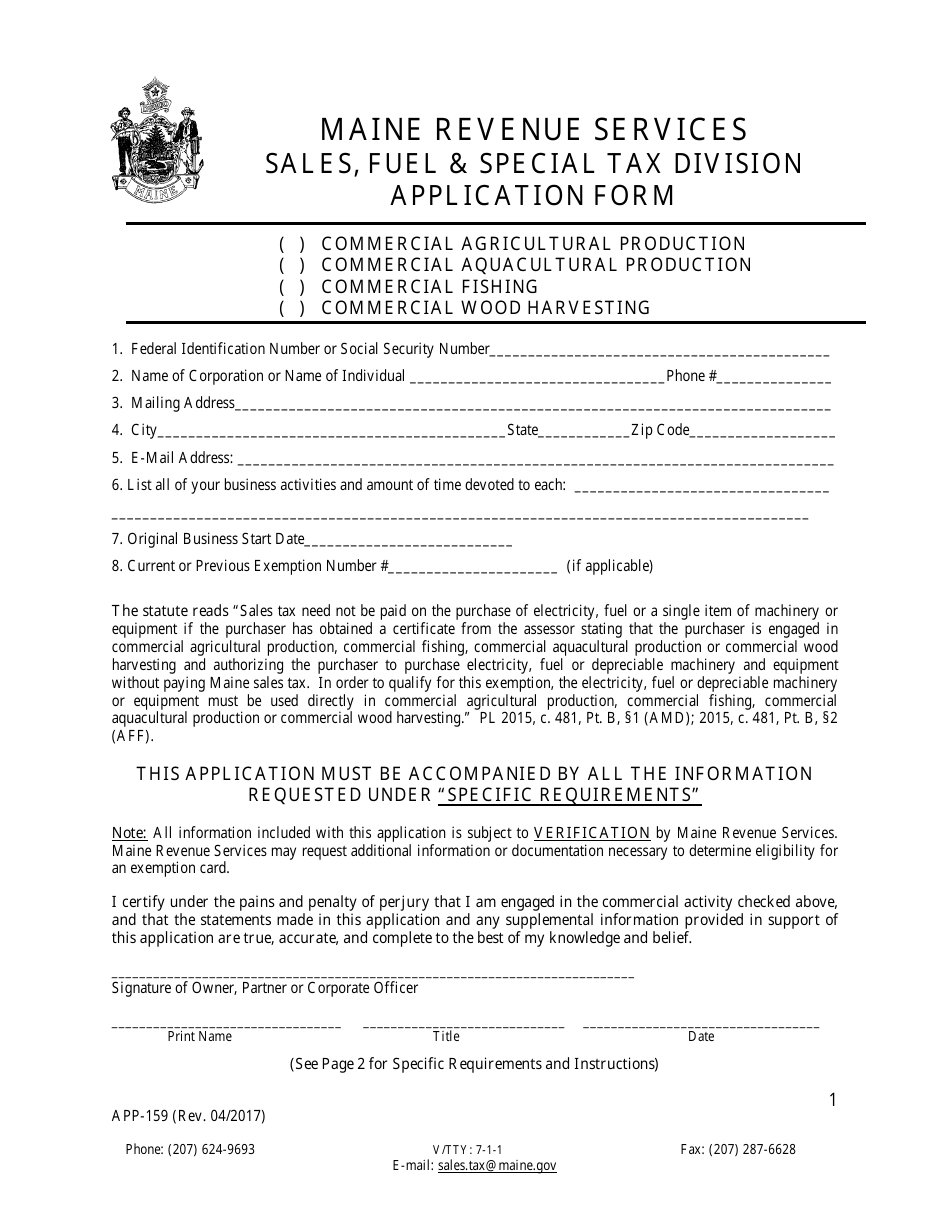

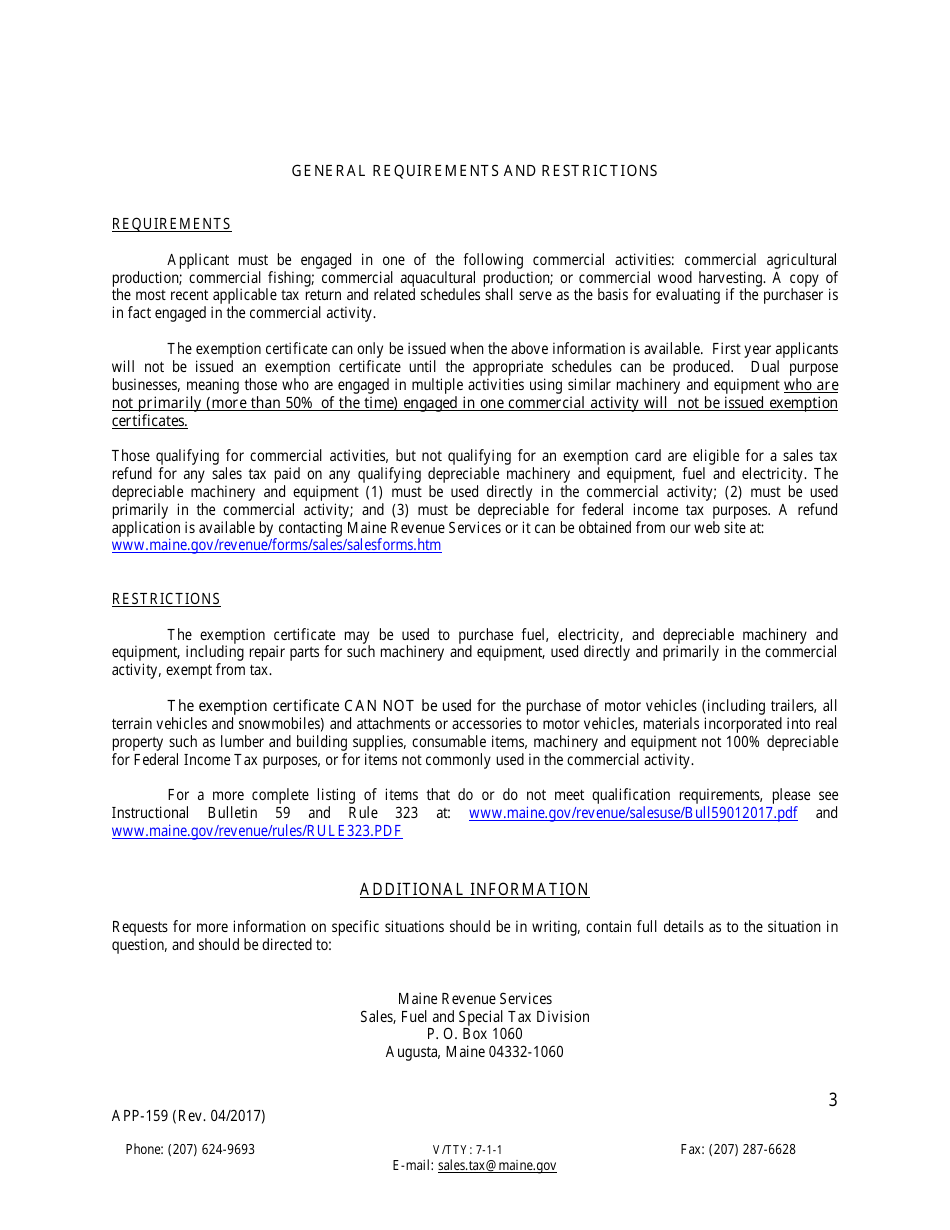

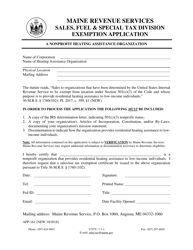

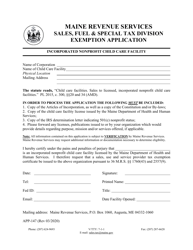

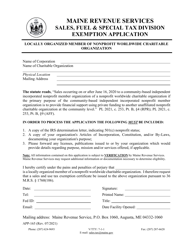

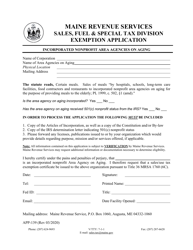

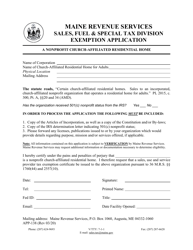

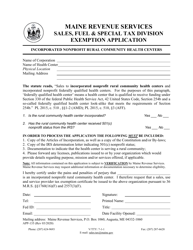

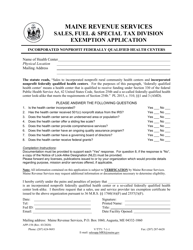

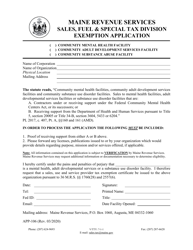

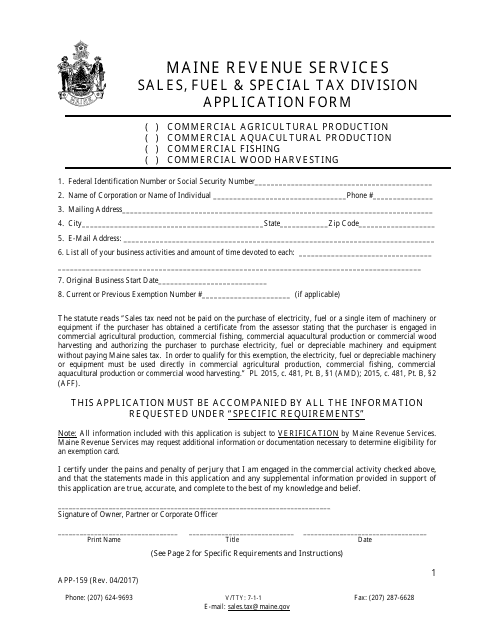

Form APP-159 Combined Commercial Exemption Application - Maine

What Is Form APP-159?

This is a legal form that was released by the Maine Department of Administrative and Financial Services - a government authority operating within Maine. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is APP-159?

A: APP-159 is the Combined Commercial Exemption Application form for businesses in Maine.

Q: Who needs to fill out APP-159?

A: Businesses in Maine that want to apply for a commercial exemption need to fill out APP-159 form.

Q: What is a commercial exemption?

A: A commercial exemption is a permit that allows certain businesses in Maine to operate without paying certain taxes or fees.

Q: What are the requirements to qualify for a commercial exemption?

A: The specific requirements for a commercial exemption vary depending on the type of business, but generally include criteria such as size, location, and industry.

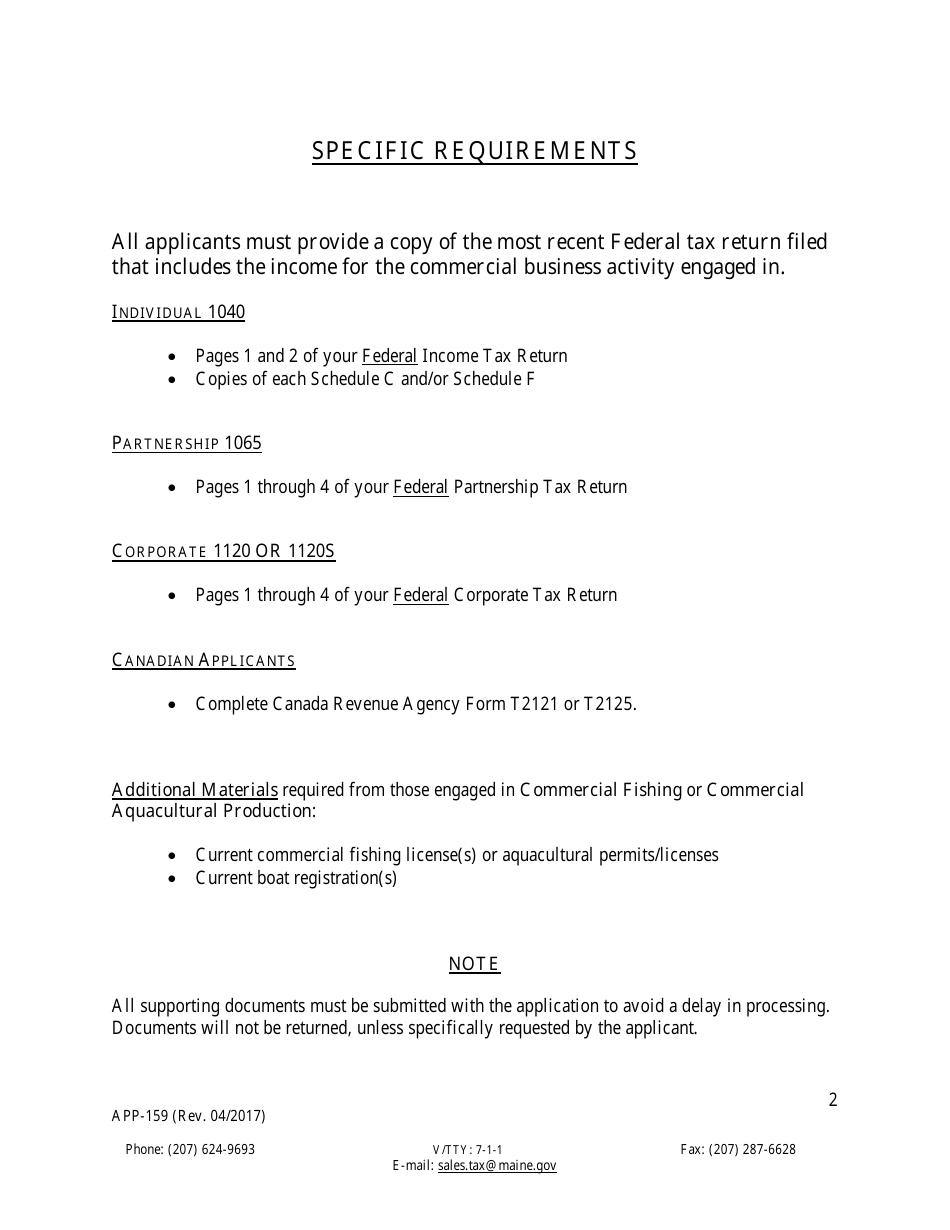

Q: Are there any fees associated with filing APP-159?

A: There may be fees associated with filing APP-159, depending on the type of commercial exemption being applied for. It is recommended to check the instructions on the form or contact the Maine Department of Revenue Services for more information.

Q: What other documents may be required along with APP-159?

A: Additional documents may be required depending on the specific commercial exemption being applied for. It is best to review the instructions on the form or contact the Maine Department of Revenue Services for a complete list of required documents.

Form Details:

- Released on April 1, 2017;

- The latest edition provided by the Maine Department of Administrative and Financial Services;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form APP-159 by clicking the link below or browse more documents and templates provided by the Maine Department of Administrative and Financial Services.

Download Form APP-159 Combined Commercial Exemption Application - Maine

1

2

3