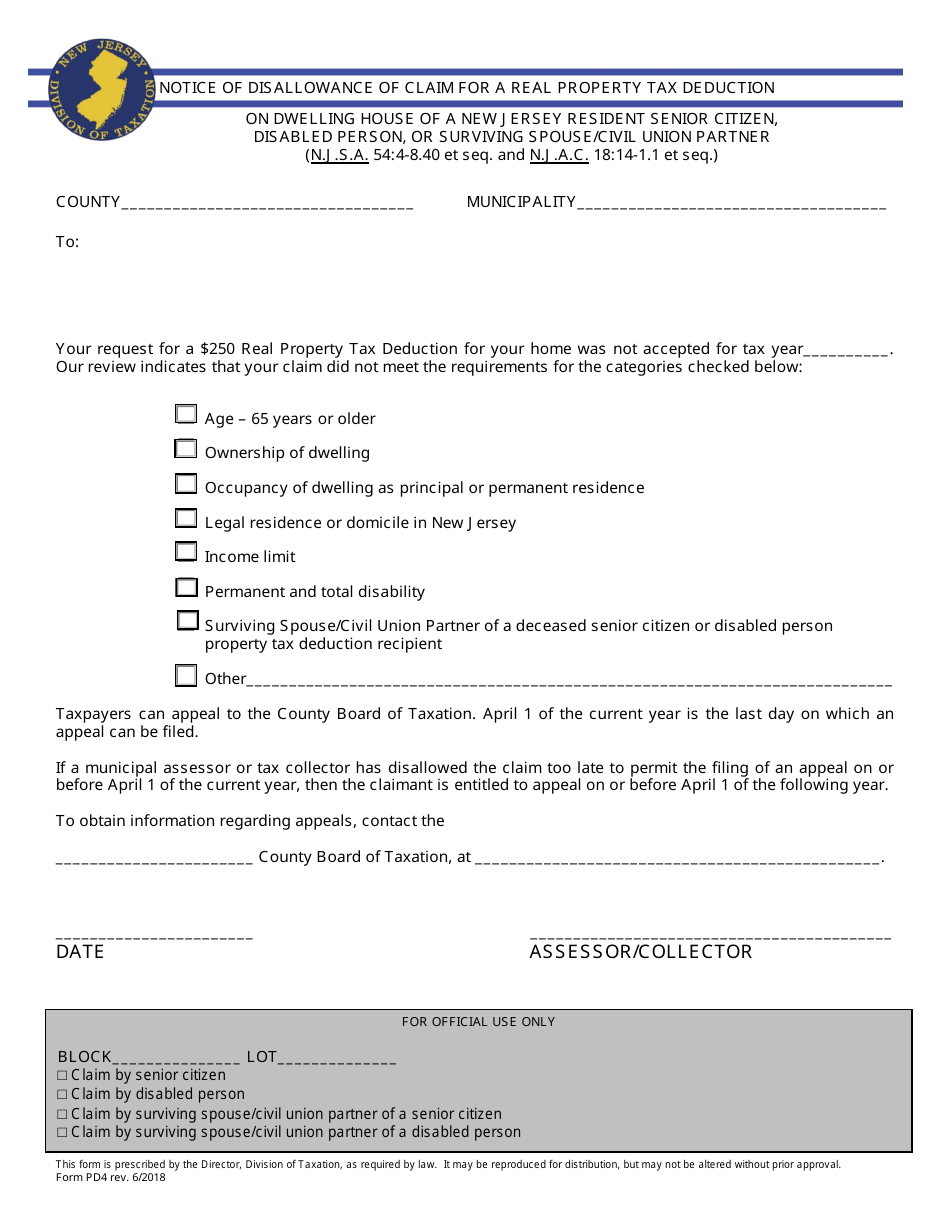

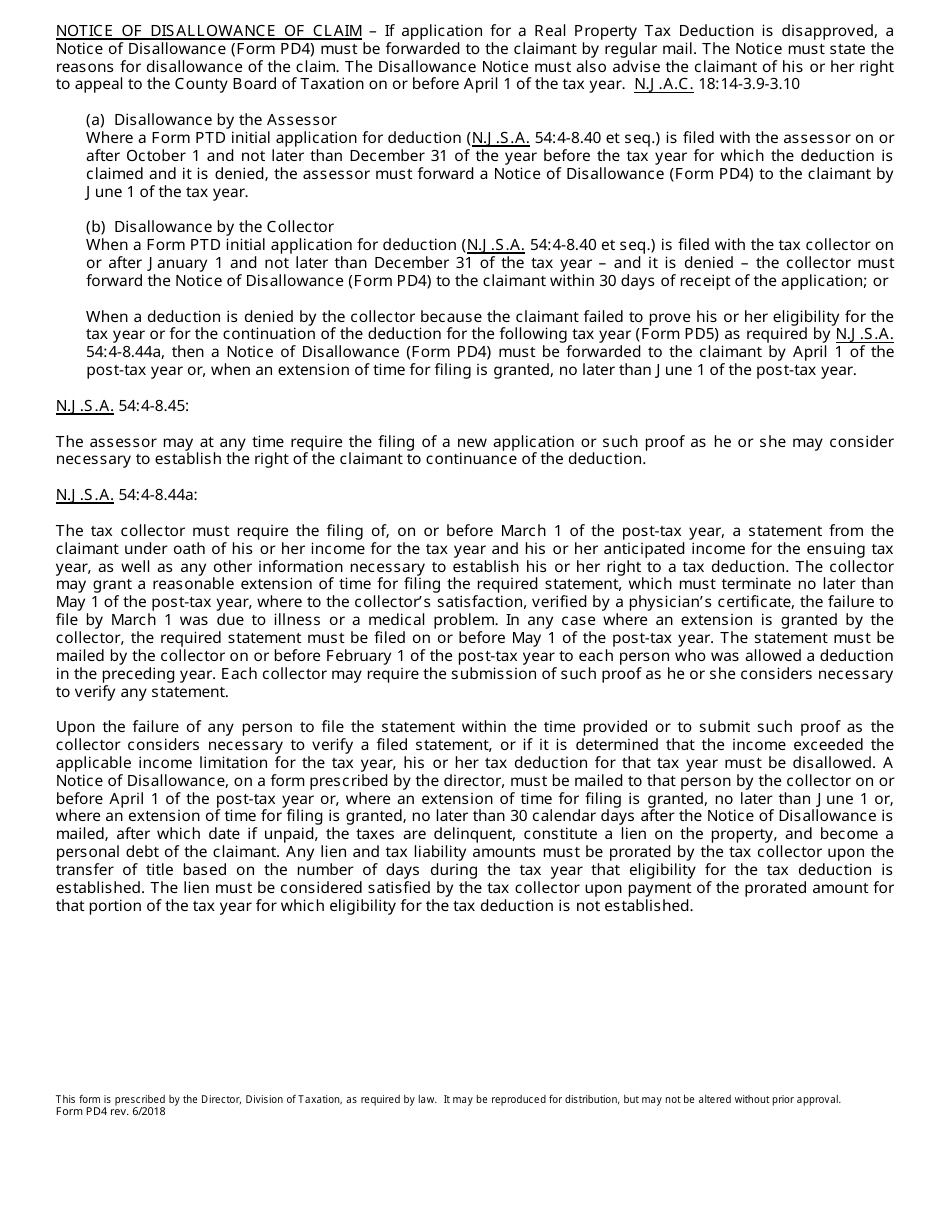

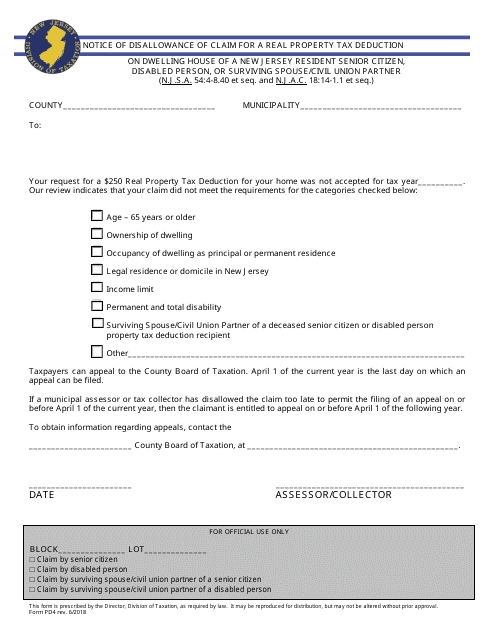

Form PD4 Notice of Disallowance of Claim for a Real Property Tax Deduction - New Jersey

What Is Form PD4?

This is a legal form that was released by the New Jersey Department of the Treasury - a government authority operating within New Jersey. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is a PD4 Notice of Disallowance?

A: A PD4 Notice of Disallowance is a document issued by the state of New Jersey to inform a taxpayer that their claim for a real propertytax deduction has been denied.

Q: What is a real property tax deduction?

A: A real property tax deduction is a benefit that allows homeowners to deduct a portion of their property taxes from their federal income taxes.

Q: Why would a PD4 Notice of Disallowance be issued?

A: A PD4 Notice of Disallowance may be issued if the taxpayer's claim for a real property tax deduction does not meet the eligibility criteria set by the state of New Jersey.

Q: What should I do if I receive a PD4 Notice of Disallowance?

A: If you receive a PD4 Notice of Disallowance, you should review the reasons for the denial and gather any necessary documentation to support your claim. You may also consider contacting the New Jersey Division of Taxation for further assistance.

Q: Can I appeal a PD4 Notice of Disallowance?

A: Yes, you can appeal a PD4 Notice of Disallowance by following the instructions provided on the notice. It is important to act within the specified timeframe to submit your appeal.

Q: Is the PD4 Notice of Disallowance specific to New Jersey?

A: Yes, the PD4 Notice of Disallowance is specific to New Jersey and relates to the state's real property tax deduction program.

Form Details:

- Released on June 1, 2018;

- The latest edition provided by the New Jersey Department of the Treasury;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form PD4 by clicking the link below or browse more documents and templates provided by the New Jersey Department of the Treasury.

Download Form PD4 Notice of Disallowance of Claim for a Real Property Tax Deduction - New Jersey

1

2